Is being pro-business and pro-capitalism the same? Does capitalism generate an unfair distribution of income? Was capitalism responsible for the most recent financial crisis? Dr. Jeffrey Miron at Harvard answers these questions by exposing three common myths of capitalism.

May 19, 2013

Top Three Common Myths of Capitalism

Comments Off on Top Three Common Myths of Capitalism

May 18, 2013

The booming market in pre-owned high fashion clothing

A market I have to admit I was almost completely ignorant about, but it’s poised to become a very busy, competitive market if it can overcome a few hurdles:

There’s been a digital explosion in the market for pre-owned fashion. In the past year, we’ve seen a veritable land grab in the online consignment and resale space with the number of “re-commerce” sites now exceeding 50 — and many more, no doubt, incubating in Silicon Valley, New York, London and beyond. Several market levels are being addressed: mall/high street (Threadflip, Tradesy), thrift (LikeTwice, NiftyThrifty), upmarket (TheRealReal), haute vintage (Byronesque) and boutique (ReFashioner, my own company).

It may seem like these sites are dealing in a mere by-product of the fashion industry. But no, this is the product. Everything that’s bought becomes pre-owned. A tidal wave is building and it has the power to undermine or even destroy. Indeed, the stockpile of merchandise is overwhelmingly vast. I did the math in 2009 for ReFashioner’s beta, a luxury fashion swap site: $880 billion trapped in closets. And that’s just high-end womenswear in the US.

[. . .]

As with flash sales, this inventory is delimited by the retail market. And it’s wayward. The ROI sucks when every SKU is singular and inventory is locked up — literally — in houses. And there’s something of a standoff between buyer and seller: the non-professional seller, accustomed to seeing 100 percent mark-ups in the real world, wants top dollar for her career basics and contemporary designer wear, while the buyer wants Zappos-like service, Etsy pricing and Net-a-Porter merchandising. There are other issues too: resistance to higher ticket items without fittings, sketchy return policies, knock-off trading.

But there’s more. This merchandise is personal. It’s not just a numbers game, it’s about everything fashion means to us. It’s about honouring the past of the clothes and their place in our lives. If this is going to work, we need to add content and context. Idealistic, maybe. But idealism is how things get changed and idealism can work to the advantage of this category.

H/T to Virginia Postrel for the link.

Comments Off on The booming market in pre-owned high fashion clothing

May 16, 2013

The causes of the “Great Recession” by Tyler Cowen

According to Professor Tyler Cowen, the Great Recession was caused by a number of different factors. Cowen outlines 4 distinct and complicated problems which led to the downturn:

• A drop in the aggregate demand (http://en.wikipedia.org/wiki/Aggregat…)

• A “horribly” performing banking sector

• Problems with monetary policy

• An increase in the “risk premium” (http://en.wikipedia.org/wiki/Risk_pre…)Prof. Cowen explains why one economic model isn’t sufficient to explain the economic downturn. He shows how several different economic models can be used to explain both the cause and the effects of the recession.

Comments Off on The causes of the “Great Recession” by Tyler Cowen

May 12, 2013

SF novels for economists

Noah Smith cobbles together a list of science fiction novels that might be of interest to economists:

Diane Coyle has a blog post called “Classics for economists,” and someone on Twitter requested that I do a companion piece called “Science fiction for economists”, so here it is.

Really, most science fiction is about economics. What makes most future visions interesting is not just the technical particulars of the cool new Stuff, but the social ramifications. Here are some of the sci-fi books that I thought dealt with important economic issues in the most insightful and interesting ways. I also chose only books that I think are well-written, with well-conceived characters, engaging plots, and skillful writing.

1. A Deepness in the Sky, by Vernor Vinge

2. Makers, by Cory Doctorow

3. The Dispossessed, by Ursula K. LeGuin

4. Down and Out in the Magic Kingdom, by Cory Doctorow

5. Rainbows End, by Vernor Vinge

6. Accelerando, by Charles Stross

7. Lucifer’s Hammer, by Larry Niven and Jerry Pournelle

8. The Windup Girl, by Paolo Bacigalupi

9. The Moon is a Harsh Mistress, by Robert Heinlein

10. Schismatrix, by Bruce Sterling

11. Permutation City, by Greg Egan

12. Reamde, by Neal Stephenson

13. The Game of Thrones series, by George R.R. Martin

In addition to the ones I’ve marked in boldface (that is, I’ve read them and agree they belong on this list), I suspect Stephenson’s Reamde would be worth reading, although I didn’t like Anathem and Smith lauds that as being Stephenson’s “#1 awesomest book”. The best comment on this post is the first one by Anonymous: “When Hari Seldon predicted his exclusion from this list a single tear rolled down his cheek.”

Comments Off on SF novels for economists

May 9, 2013

Delingpole: Ferguson shouldn’t have apologized

Although James Delingpole concedes that Ferguson pretty much had to apologize for his off-the-cuff remarks on Keynes, he still thinks it was the wrong thing to do:

I don’t think there’s much doubt about Keynes’s latent gayness: not without reason was he known as the ‘Queen of King’s’. And I’m not really sure that the fact that he later married and attempted (unsuccessfully) to have children proves anything very much. Unless, of course, you’re a modern, professional-offence-taking gay activist, in which case it’s the final clincher in your compelling argument that Ferguson is totally evil and really should lose his Lawrence A. Tisch professorship at Harvard right this second for — as one angry commentator put it — taking ‘gay-bashing to new heights’.

New heights? Really? As Jonah Goldberg has noted, it’s not like there’s anything particularly new or controversial in Ferguson’s theory, tossed off lightly in response to a question at an economics conference. ‘He was childless and his philosophy of life was essentially a short-run philosophy,’ wrote Schumpeter in his obituary of Keynes.

[. . .]

Which is why, of course, Niall Ferguson was forced to issue an apology. Not, I suspect — or rather, I hope — because he thought he’d done anything wrong, but because all too easily it could have become the chink in the armour into which his many enemies were able to insert their fatal stilettos. (I know whereof I speak here, you may recall.)

Here’s how it works: lots of liberal-lefties utterly loathe Ferguson for having committed the unforgivable crime of being an articulate and prominent exponent of right-wing views. Unfortunately, we don’t (yet) live in an era where voicing right-wing views is an indictable offence; so the way to get at such dangerously outspoken defenders of free markets, liberty and small government is through the back door, a bit like Al Capone eventually being done for tax evasion. Racism would have been the ideal charge (except Ferguson’s marriage to Ayaan Hirsi Ali scuppered that option); as too would perceived sexism (which did for Harvard president Larry Summers, remember); but the homophobia charge — had not Ferguson nipped it in the bud — would have surely worked its poison just as well in the end.

I perfectly understand why Ferguson apologised but I wish he hadn’t and I’m sure in his heart he knows he shouldn’t have done. As an economic historian, he’ll be familiar with Danegeld: the more you concede to the enemy, the more they’ll demand next time round.

Comments Off on Delingpole: Ferguson shouldn’t have apologized

May 6, 2013

A Canadian criminal innovation – cheese smuggling

The CBC reports on a breathtaking news item … imported mozzarella cheese is being removed from the clutches of the supply management system, which will reduce prices by a significant amount:

Pizza lovers could soon be paying less for their favourite pies.

A ruling made this week by the Canadian Dairy Commission could soon allow Canadian restaurants to buy deeply discounted mozzarella cheese.

The commission changed the rules used to classify mozzarella cheese, putting the milk product in its own class and essentially removing it from supply-management pricing. Before the ruling, the price for mozzarella cheese in Canada was artificially high when compared to the world market.

The new class, to take effect June 1, is expected to result in lower costs for Canadian-made mozzarella for restaurants that prepare and cook pizzas on site.

Bob Abumeeiz, who owns Arcata Pizzeria in Windsor, Ont., said the ruling could drop the price of a large pizza by as much as 10 per cent.

Oh, and the cheese smuggling?

High prices are part of the reason some pizzeria owners were turning to contraband cheese, smuggled into Canada from the U.S.

Last fall CBC News learned three men, including one current and one former police officer from the Niagara Falls area, were charged in connection with an international cheese-smuggling network.

The men are accused of smuggling caseloads of cheap cheese from the U.S. to sell to Canadian pizzerias and restaurants.

May 5, 2013

Niall Ferguson apologizes for inappropriate comments about Keynes

Historian and Harvard professor Niall Ferguson has issued an apology for some remarks he made about John Maynard Keynes at a conference in California:

I had been asked to comment on Keynes’s famous observation “In the long run we are all dead.” The point I had made in my presentation was that in the long run our children, grandchildren and great-grandchildren are alive, and will have to deal with the consequences of our economic actions.

But I should not have suggested — in an off-the-cuff response that was not part of my presentation — that Keynes was indifferent to the long run because he had no children, nor that he had no children because he was gay. This was doubly stupid. First, it is obvious that people who do not have children also care about future generations. Second, I had forgotten that Keynes’s wife Lydia miscarried.

My disagreements with Keynes’s economic philosophy have never had anything to do with his sexual orientation. It is simply false to suggest, as I did, that his approach to economic policy was inspired by any aspect of his personal life. As those who know me and my work are well aware, I detest all prejudice, sexual or otherwise.

Comments Off on Niall Ferguson apologizes for inappropriate comments about Keynes

May 4, 2013

Ron Paul on the so-called “Marketplace Fairness Act”

As you probably guessed, he’s against it:

David French, Senior Vice President of the National Retail Federation, the major industry group lobbying for the so-called “Marketplace Fairness Act,” (more aptly named the “National Internet Tax Mandate”) recently commented that “…the law [governing Internet sales] today is a 20th-century interpretation of an 18th-century document…” Mr. French’s comments are typical of those wishing to expand government power beyond the limits established by the United States Constitution.

[. . .]

The National Internet Tax Mandate overturns the Supreme Court’s 1992 Quill v. North Dakota decision that states can only force businesses to collect sales tax if the business has a “physical presence” in the state. Quill represented a rare instance where the Supreme Court properly interpreted the Commerce Clause. Thanks to the Quill decision, the Internet has remained a tax-free zone, though some states require consumers to later pay taxes on products they purchased online. This freedom has helped turn the Internet into a thriving and dynamic sector of the economy, to the benefit of entrepreneurs and consumers.

Now that status is threatened by an alliance of big business and tax-hungry state governments seeking new powers to force out-of-state business to collect state sales taxes. Far from updating the Constitution to fit the needs of the 21st century, the National Internet Tax Mandate is a throwback to 18th century mercantilism.

The National Internet Tax Mandate will raise the costs of doing business over the Internet. Large, established Internet companies, such as Amazon, can absorb these costs, whereas their smaller competitors cannot. More importantly, the Mandate’s increased costs and regulations could prevent the creation and growth of the next Amazon.

Comments Off on Ron Paul on the so-called “Marketplace Fairness Act”

This is why cash-rich Apple is borrowing money on the bond market

In one word, taxes:

What a crazy world. Apple, a company with $145 billion of cash, is issuing some $17 billion of debt to buy back its own shares. Why doesn’t it just use its cash to do the same thing? First, because a lot of that cash is overseas, and bringing it back to America would incur a tax charge. Second, because interest rates are low and debt interest is tax-deductible, making this look a great arbitrage.

But think of it from the point of view of the hard-working American taxpayer. Apple’s money will still sit overseas and not be invested at home to create jobs. Apple’s tax bill will fall, as it offsets the interest payments against its profits. The buy-back will probably push up the share price in the short term, boosting the value of executive options; profits from those options will probably be taxed at the long-term capital gains tax rate of 15%, lower than the rate many workers pay. Organising a bond issue, rather than using a company’s own cash, incurs costs in the form of fees to bankers on Wall Street; the same bankers taxpayers helped support five years ago.

Comments Off on This is why cash-rich Apple is borrowing money on the bond market

May 2, 2013

Canada’s Arctic patrol ship design program just a job creation scheme that doesn’t actually create jobs in Canada

The CBC’s Terry Milewski on the Harper government’s much-heralded shipbuilding program which is far more expensive than it needs to be — because of the demand that the work be done in Canada — and yet somehow doesn’t even manage to create Canadian jobs:

Public Works Minister Rona Ambrose and Defence Minister Peter MacKay announced March 7 in Halifax that Ottawa will pay Irving Shipbuilding $288 million just to design — not build — a fleet of new Arctic offshore patrol ships.

Irving will then build the ships under a separate contract.

However, a survey of similar patrol ships bought by other countries shows they paid a fraction of that $288 million to actually build the ships — and paid less than a tenth as much for the design.

In addition, the design of Canada’s new ships is based upon a Norwegian vessel whose design Ottawa has already bought for just $5 million.

The Norwegian ship, the Svalbard, was designed and built for less than $100 million in 2002.

Experts say the design price is normally 10-20 per cent of the total cost of the ships.

But don’t worry … jobs are being created or saved by this major Canadian government project … in Denmark and in the United States:

Another criticism of the project is that much of the design work — in a project meant to create Canadian jobs — is actually going overseas.

Although Irving will manage the design project in Nova Scotia, it has subcontracted the actual production of final blueprints to a Danish firm, OMT. Seventy Danish ship architects will work on those.

The job of designing the systems integration is going to Lockheed Martin and the propulsion system will be designed by General Electric, both U.S. companies.

This is only to be expected, say supporters of the project.

“We’ve been dormant here for better than two decades now. We don’t have the skill sets inside the industry,” said Ken Hansen, editor of the Canadian Naval Review in Dartmouth, N.S.

Comments Off on Canada’s Arctic patrol ship design program just a job creation scheme that doesn’t actually create jobs in Canada

April 28, 2013

Reason.tv: Why the GOP Should Embrace Science

“What has always alleviated our scarcity? What has always alleviated our environmental problems? Technology. What breeds technological dynamism? Economic success,” explains Joshua Jacobs, co-founder of the Conservative Future Project, a new pro-science, pro-technology organization that’s trying to get the Republican Party to embrace an open-ended future filled with driverless cars, stem-cell research, and private space exploration.

If that sounds like a tall order for a party whose leading presidential candidates in 2012 waffled on whether they believed in evolution, you’re right. But Jacobs argues forcefully that the GOP is no less anti-science than the Democrats and actually has a long history of pushing scientific and technological innovation.

Nick Gillespie sat down with Jacobs in Reason‘s D.C. studio to talk about how conservatives might stop standing athwart history yelling stop and march boldly into the future.

Comments Off on Reason.tv: Why the GOP Should Embrace Science

April 27, 2013

The misplaced outrage over Amazon’s tiny tax bill in the UK

Tim Worstall explains that the current efforts by various campaigners including Stephen Fry are not only a waste of time and effort, but betray a fundamental misunderstanding of how the EU is set up:

There are several points that could be made. One being that selling to Brits from Luxembourg is not tax dodging, it’s exactly what the EU intends the Single Market should be. A, umm, single market across 27 countries. A second might be that even if we start to whine about UK warehouses, tax is still not due here. Our double taxation treaty with Luxembourg means that such warehouses do not lead to tax being due. And that’s from 1968 or so when Wilson ruled: it’s also a standard part of all double taxation treaties and for good reason.

(For example, the metals trade uses warehouses in Rotterdam as the point at which a contract is concluded. The cut flowers business warehouses in a small village near Schipol. Should Holland get all the tax from the world’s metals and flower businesses? Or should everyone be taxed where they really are, not the warehouses?)

But there’s much worse than this. We’ve had the Margaret Hodges screeching that we’re talking about immoral, not illegal. The TJN and other fools similarly scream about how awful it is that people can do business without paying tax. And it is precisely all of this activism that leads these gentle booksellers to spend their year collecting signatures. To absolutely no avail whatsoever.

For in the year they are complaining about, last year, 2012, Amazon did not make a profit. A $39 million loss in fact according to their accounts. It’s simply not true that “tax dodging” by Amazon is leading to the crucifixtion of the independent book shop. That’s a lie that’s been foisted upon people by the obfuscations of the campaigners.

Comments Off on The misplaced outrage over Amazon’s tiny tax bill in the UK

April 25, 2013

Populist talk on taxes may please the voters (sometimes), but it won’t help the economy

In Maclean’s, Stephen Gordon explains why the only kind of tax hikes that seem in any way “popular” are particularly bad if implemented:

Magical thinking might be smart politics, but it’s not very good economics. Here are the two most popular themes:

- Higher corporate income taxes. From a political marketing point of view, the appeal of increasing corporate income tax (CIT) rates is obvious: “Hey, I’m not a corporation, so it’s no skin off my nose.” But the economics of CIT rates are very dodgy indeed: higher CIT rates are the most costly way of generating revenue and are most harmful to economic growth. It also turns out that workers and consumers are the ones who ultimately bear the burden of higher CIT rates. (If you start taxing corporate profits, shareholders will eventually move their money to jurisdictions with more competitive rates, reducing the availability of investment capital. In the long-run, that results in lower output and weaker labour demand. More on that here.) But even if you were willing to pay these costs, higher CIT rates don’t generate much in the way of new revenues.

- Increased taxes on high earners. While there may be good reasons for wanting to use the personal income tax system to counter recent trends in the concentration of income, policymakers should be under no illusions about how much new revenue taxing the rich will bring in. There simply aren’t that many high earners to tax, and they have access to expert tax planning advice: there is overwhelming evidence showing that those with high incomes can and will respond to higher tax rates by reporting lower taxable income.

Comments Off on Populist talk on taxes may please the voters (sometimes), but it won’t help the economy

April 24, 2013

Copyright terms are almost certainly too long already

At Techdirt, Mike Masnick makes the case for reducing the swollen length of time current copyrights are protected:

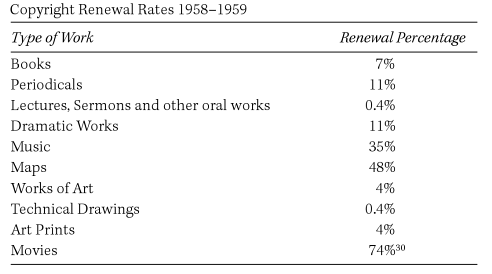

We’ve pointed a few times in the past to a chart from William Patry’s book, looking at how frequently copyright was renewed at the 28 year mark back when copyright (a) required registration and (b) required a “renewal” at 28 years to keep it another 28 years. The data is somewhat amazing:

As you can see, very few works are renewed after 28 years. Only movies, at 74% are over the 50% mark. Only 35% of music and only 7% of books tells quite a story. It makes it quite clear that even the copyright holders see almost no value in their copyrights after a short period of time. It appears that the Bureau of Economic Analysis is coming to the same conclusion from a different angle. As Matthew Yglesias notes, as part of its effort to recalibrate how it calculates GDP, the BEA is considering money spent on the creation of content an “investment” in a capital good, which needs to be depreciated over the time period in which it is valuable. Frankly, I’m not convinced this is the smartest way to account for money spent on the creation of content, but either way, the BEA’s analysis provides some insight into the standard “economic life” of various pieces of content, which match up with the chart above in many ways.

Comments Off on Copyright terms are almost certainly too long already