Video game communities, social economies, give us something that we never had as economists before. That’s something of an opportunity, a chance to experiment with a macroeconomy. We can experiment in economics with individuals. We can put someone behind a screen and experiment on the subject, and ask him or her to make choices and see how they behave.

That has nothing to do with macroeconomics. Macroeconomics requires a different scenario. You conduct controlled experiments with a large economy. We are not allowed to do this in the real world. But in the video game world, we economists have a smidgen of an opportunity to conduct controlled experiments on a real, functioning macroeconomy. And that may be a scientific window into economic reality that we’ve never had access to before.

Yanis Varoufakis, talking to Peter Suderman, “A Multiplayer Game Environment Is Actually a Dream Come True for an Economist”, Reason, 2014-05-30.

March 4, 2015

QotD: The macroeconomic insights of MMO gaming

February 26, 2015

Free trade is for consumers, not producers

Matt Ridley gives a potted history of the rise of free trade in the nineteenth century, bringing great benefit to workers and consumers:

… the point about free trade is and always should be that it is good for consumers. “Consumption is the sole end and purpose of all production”, said Adam Smith. The genius of the Corn Law radicals was to turn the debate upside down and give the consumers a voice. Between 1660 and 1846, the British government passed 127 Corn Laws, imposing tariffs as well as rules about the storage, sale, import, export and quality of grain and bread. The justification was much like today’s opposition to TTIP: maintaining our supposedly high standards against foreign, cheapskate corner-cutters.

In 1815, Parliament banned the import of all grain if the price fell below 80 shillings a quarter — to protect landowners. Rioters vandalised the house of Lord Castlereagh and other supporters. David Ricardo wrote a pamphlet against the laws, but in vain. It was not until the 1840s that the railways and the penny post enabled Richard Cobden and John Bright to stir up a successful mass campaign against the laws on behalf of the working class’s right to buy cheap bread from abroad if they wished.

Cobden did not stop there. Elected to parliament but refusing office and honours, this pacifist radical was as responsible as anybody for accelerating global economic growth. He persuaded Gladstone to abolish many tariffs unilaterally, and personally negotiated the first international free trade treaty in 1860, the so-called Cobden-Chevalier treaty with France, which established the unconditional “most-favoured nation” principle, leading to the dismantling of tariffs all over Europe. “Peace will come to earth when the people have more to do with each other and governments less,” he said.

Only when Bismarck began rebuilding tariffs in 1879 did the tide begin to turn, and competitive protectionism slowly throttled free trade, eventually contributing to half a century of war. Britain held out longest, enacting a general tariff only in 1932 under Neville Chamberlain as chancellor. Trade barriers undoubtedly helped precipitate war: they shut the Japanese out of resource markets that they then decided to seize by force instead, while Germany’s Lebensraum argument would have carried less force in a free-trading world.

The argument for free trade is paradoxical and much misunderstood. Free trade benefits consumers because it is the scourge of expensive or monopolistic national suppliers. It benefits both sides: yet it works unilaterally. Your citizens benefit if you let them buy cheap goods from abroad, while foreigners are punished if their government does not reciprocate. This creates more demand for local services and hence more growth and jobs in the importing country.

February 22, 2015

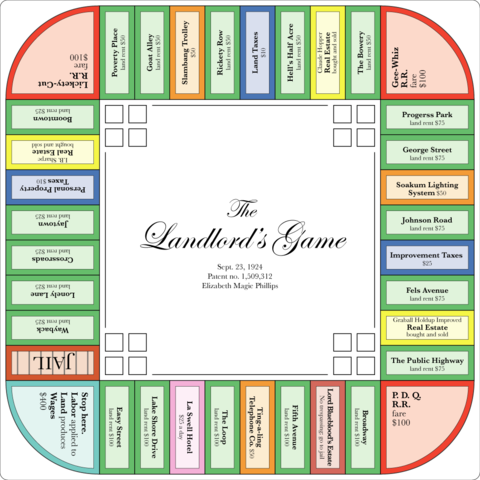

The forgotten history of the game of Monopoly

At Open Culture, Dan Colman looks at how Monopoly evolved and changed before it became a fixture in children’s games, despite the intent of the original designer:

The great capitalist game of Monopoly was first marketed by Parker Brothers back in February 1935, right in the middle of the Great Depression. Even during hard times, Americans could still imagine amassing a fortune and securing a monopoly on the real estate market. When it comes to making money, Americans never run out of optimism and hope.

Monopoly didn’t really begin, however, in 1935. And if you trace back the origins of the game, you’ll encounter an ironic, curious tale. The story goes like this: Elizabeth (Lizzie) J. Magie Phillips (1866–1948), a disciple of the progressive era economist Henry George, created the prototype for Monopoly in 1903. And she did so with the goal of illustrating the problems associated with concentrating land in private monopolies. As Mary Pilon, the author of the new book The Monopolists: Obsession, Fury, and the Scandal Behind the World’s Favorite Board Game, recently explained in The New York Times, the original game — The Landlord’s Game — came with two sets of rules: “an anti-monopolist set in which all were rewarded when wealth was created, and a monopolist set in which the goal was to create monopolies and crush opponents.” Phillips’ approach, Pilon adds, “was a teaching tool meant to demonstrate that the first set of rules was morally superior.” In other words, the original game of Monopoly was created as a critique of monopolies — something the trust- and monopoly-busting president, Theodore Roosevelt, could relate to.

For more on the modern game, here’s the Wikipedia page.

Obamacare’s externalities

Megan McArdle on just what externalities are and why we pay attention to them:

For those who might not know the term, “externality” is economist-speak, and it means about what it sounds like: an effect that your action has on others. An externality can be positive or negative, and obviously, we as a society would like to have as many as possible of the former and as few as possible of the latter. In other words, “Your right to swing your fist stops at the end of my nose.”

I’m a libertarian, and libertarians love talking about externalities. They give us a (relatively) clear way to define what are and are not legitimate scopes of public action. Whatever you’re doing in the privacy of your own bedroom with another consenting adult is really none of my business, even if I think you oughtn’t to be doing it. On the other hand, if you’re breeding rats and cockroaches in there, and they’re coming through the shared wall of our respective row houses, then I have the right to get the law involved.

Framing things as “externalities” is therefore a good way to get a libertarian, or someone who leans that way, on your side. And such frames have come up over and over in the debate over Obamacare, which has been variously justified by the cost to the state of emergency room care; the cost to society of free-riding young folks who don’t buy insurance until they get sick; the public health cost of people who don’t go to the doctor and get really, expensively sick; an unhealthy workforce that is less productive; and the cost to friends and relatives who have to chip in to cover uninsured medical expenses.

I didn’t find any of those arguments particularly convincing. The third can just be dispensed with on the grounds of accuracy: In general, preventive medicine does not save money. Oh, it may save money in the particular case of someone whose diabetes or cancer went long undiagnosed. The problem is, you can’t just look at the cost of sick folks who would have been a lot cheaper to treat if their conditions had been caught earlier. You also have to include the cost of all the healthy people you had to screen in order to catch that one case of disease. And with limited exceptions, the cost of screening the healthy generally outweighs the cost of treating the chronically ill. Now, you can certainly argue for preventive care on other grounds — for example, that it makes people healthier (though even then you have to add the cost of unnecessary medical procedures, such as biopsies following a false positive on a blood test, which is why we do not, say, give annual mammograms to every American woman). But it’s not generally a money saver, so this particular externality doesn’t exist.

The rest of the arguments have some weight, but in the end, I don’t think they’re weighty enough. Let me explain.

February 17, 2015

The bet between Julian Simon and Paul R. Erlich

Aaron Tao remembers one of the more amusing stories from the career of economist Julian Simon:

February 12 marks the birthday of the late economist Julian Simon (1932–1998). On this special occasion, I wish to bring attention to this thinker whose work I feel has not been fully appreciated. The implications of his controversial but time-tested ideas certainly deserve greater attention in academia and society at large.

Simon is perhaps best known for his famous wager against ecologist Paul R. Ehrlich, author of the notorious best-seller The Population Bomb.

In line with classical Malthusian theory, Ehrlich predicted that human population growth would result in overconsumption, resource shortages, and global famine — in short, an apocalyptic scenario for humanity. Simon optimistically countered Ehrlich’s claim and argued that the human condition and our overall welfare would flourish thanks to efficient markets, technological innovation, and people’s collective ingenuity. Both men agreed to put their money where their mouth is.

They agreed that rising prices of raw materials would indicate that these commodities were becoming more scarce, and this became the premise of The Bet. The metals chromium, copper, nickel, tin, and tungsten were chosen as measures of resource scarcity by Ehrlich’s team. Ehrlich and his Malthusian colleagues invested a total of $1,000 (in 1980 prices) on the five metals ($200 each). The terms of the wager were simple: If by the end of the period from September 29, 1980, to September 29, 1990, the inflation-adjusted prices of the metals rose, then Simon would pay Ehrlich the combined difference, and vice versa if the prices fell.

Here’s the final outcome as summarized by Wired:

Between 1980 and 1990, the world’s population grew by more than 800 million, the largest increase in one decade in all of history. But by September 1990, without a single exception, the price of each of Ehrlich’s selected metals had fallen, and in some cases had dropped through the floor. Chrome, which had sold for $3.90 a pound in 1980, was down to $3.70 in 1990. Tin, which was $8.72 a pound in 1980, was down to $3.88 a decade later.

Which is how it came to pass that in October 1990, Paul Ehrlich mailed Julian Simon a check for $576.07.

A more perfect resolution of the Ehrlich-Simon debate could not be imagined.

Looking back on this high-profile debate, it is important to realize that Simon did not win because he was a savvier investor or had special knowledge about economic trends. Rather, Simon’s ideas were shown to be more empirically, intellectually, and morally sound. A distinguishing hallmark of Simon’s work was that he held a sincere conviction that human imagination was the ultimate renewable resource that can create a better world

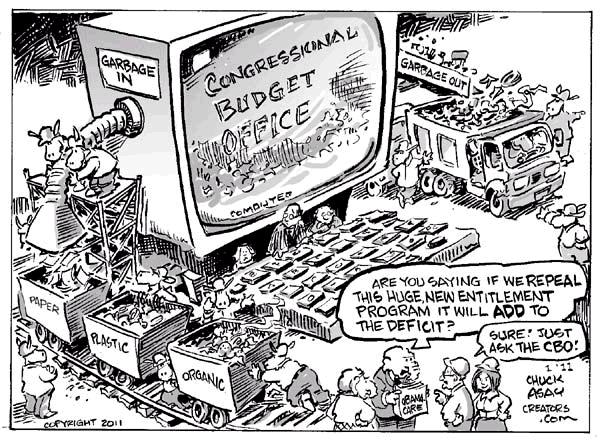

In praise of “dynamic scoring”

Dan Mitchell explains why there’s a need to change the way the Congressional Budget Office (CBO) and Joint Committee on Taxation (JCT) “keep score” on how proposed legislative changes will impact the US economy:

The CBO, for instance, puts together economic analysis and baseline forecasts of revenue and spending, while also estimating what will happen if there are changes to spending programs. Seems like a straightforward task, but what if the bureaucrats assume that government spending “stimulates” the economy and they fail to measure the harmful impact of diverting resources from the productive sector of the economy to Washington?

The JCT, by contrast, prepares estimates of what will happen to revenue if politicians make various changes in tax policy. Sounds like a simple task, but what if the bureaucrats make the ridiculous assumption that tax policy has no measurable impact on jobs, growth, or competitiveness, which leads to the preposterous conclusion that you maximize revenue with 100 percent tax rates?

Writing for Investor’s Business Daily, former Treasury Department officials Ernie Christian and Gary Robbins explain why the controversy over these topics – sometimes referred to as “static scoring” vs “dynamic scoring” – is so important.

It is Economics 101 that many federal taxes, regulations and spending programs create powerful incentives for people not to work, save, invest or otherwise efficiently perform the functions essential to their own well-being. These government-induced changes in behavior set off a chain reaction of macroeconomic effects that impair GDP growth, kill jobs, lower incomes and restrict upward mobility, especially among lower- and middle-income families. …Such measurements are de rigueur among credible academic and private-sector researchers who seek to determine the true size of the tax and regulatory burden on the economy and the true value of government spending, taking into account the economic damage it often causes.

But not all supposed experts look at these second-order or indirect effects of government policy.

And what’s amazing is that the official scorekeepers in Washington are the ones who refuse to recognize the real-world impact of changes in government policy.

These indirect costs of government, in particular or in total, have not been calculated and disclosed in the Budget of the United States or in analyses by the Congressional Budget Office. The result of this deliberate omission by Washington has been to understate many costs of government, often by more than 100%, and grossly overstate its benefits. …It is on this foundation of disinformation that the highly disrespected, overly expensive and too often destructive federal government in Washington has been built.

February 14, 2015

“I, Rose” and “A Price is Signal Wrapped Up in an Incentive”

Published on 8 Feb 2015

How is it that people in snowy, chilly cities have access to beautiful, fresh roses every February on Valentine’s Day? The answer lies in how the invisible hand helps coordinate economic activity, Using the example of the rose market, this video explains how dispersed knowledge and self-interested actors lead to a global market for affordable roses.

Published on 8 Feb 2015

Join Professor Tabarrok in exploring the mystery and marvel of prices. We take a look at how oil prices signal the scarcity of oil and the value of its alternative uses. Following up on our previous video, “I, Rose,” we show how the price system allows for people with dispersed knowledge and information about rose production to coordinate global economic activity. This global production of roses reveals how the price system is emergent, and not the product of human design.

February 12, 2015

EU governments and GM crops

Last month, Matt Ridley ran down the benefits to farmers, consumers, ecologists and the environment itself that the European Union has been resisting mightily all these years:

Scientifically, the argument over GM crops is as good as over. With nearly half a billion acres growing GM crops worldwide, the facts are in. Biotech crops are on average safer, cheaper and better for the environment than conventional crops. Their benefits accrue disproportionately to farmers in poor countries. The best evidence comes in the form of a “meta-analysis” — a study of studies — carried out by two scientists at Göttingen University, in Germany.

The strength of such an analysis is that it avoids cherry-picking and anecdotal evidence. It found that GM crops have reduced the quantity of pesticide used by farmers by an average of 37 per cent and increased crop yields by 22 per cent. The greatest gains in yield and profit were in the developing world.

If Europe had adopted these crops 15 years ago: rape farmers would be spraying far less pyrethroid or neo-nicotinoid insecticides to control flea beetles, so there would be far less risk to bees; potato farmers would not need to be spraying fungicides up to 15 times a year to control blight; and wheat farmers would not be facing stagnant yields and increasing pesticide resistance among aphids, meaning farmland bird numbers would be up.

Oh, and all that nonsense about GM crops giving control of seeds to big American companies? The patent on the first GM crops has just expired, so you can grow them from your own seed if you prefer and, anyway, conventionally bred varieties are also controlled for a period by those who produce them.

African farmers have been mostly denied genetically modified crops by the machinations of the churches and the greens, aided by the European Union’s demand that imports not be transgenically improved. Otherwise, African farmers would now be better able to combat drought, pests, vitamin deficiency and toxic contamination, while not having to buy so many sprays and risk their lives applying them.

I made this point recently to a charity that works with farmers in Africa and does not oppose GM crops but has so far not dared say so. Put your head above the parapet, I urged. We cannot do that, they replied, because we have to work with other, bigger green charities and they would punish us mercilessly if we broke ranks. Is the bullying really that bad? Yes, they replied.

Yet the Green Blob realises that it has made a mistake here. Not a financial mistake — it made a fortune out of donations during the heyday of stoking alarm about GM crops in the late 1990s — but the realisation that all it has achieved is to prolong the use of sprays and delay the retreat of hunger.

QotD: Poverty-stricken Little House on the Prairie

Consider the Little House on the Prairie books, which I’d bet almost every woman in my readership, and many of the men, recalls from their childhoods. I loved those books when I was a kid, which seemed to describe an enchanted world — horses! sleighs! a fire merrily crackling in the fireplace, and children frolicking in the snow all winter, then running barefoot across the prairies! Then I reread them as an adult, as a prelude to my research, and what really strikes you is how incredibly poor these people were. The Ingalls family were in many ways bourgeoisie: educated by the standards of the day, active in community leadership, landowners. And they had nothing.

There’s a scene in one of the books where Laura is excited to get her own tin cup for Christmas, because she previously had to share with her sister. Think about that. No, go into your kitchen and look at your dishes. Then imagine if you had three kids, four plates and three cups, because buying another cup was simply beyond your household budget — because a single cup for your kid to drink out of represented not a few hours of work, but a substantial fraction of your annual earnings, the kind of money you really had to think hard before spending. Then imagine how your five-year-old would feel if they got an orange and a Corelle place setting for Christmas.

There’s a reason old-fashioned kitchens didn’t have cabinets: They didn’t need them. There wasn’t anything to put there.

Imagine if your kids had to spend six months out of the year barefoot because you couldn’t afford for them to wear their shoes year-round. Now, I love being barefoot, and I longed to spend more time that way as a child. But it’s a little different when it’s an option. I walked a mile barefoot on a cold fall day — once. It’s fine for the first few minutes, and then it hurts like hell. Sure, your feet toughen up. But when it’s cold and wet, your feet crack and bleed. As they do if the icy rain soaks through your shoes, and your feet have to stay that way all day because you don’t own anything else to change into. I’m not talking about making sure your kids have a decent pair of shoes to wear to school; I’m talking about not being able to afford to put anything at all on their feet.

Or take the matter of food. There is nothing so romanticized as old-fashioned cookery, lovingly hand-prepared with fresh, 100 percent organic ingredients. If you were a reader of the Little House books, or any number of other series about 19th-century children, then you probably remember the descriptions of luscious meals. When you reread these books, you realize that they were so lovingly described because they were so vanishingly rare. Most of the time, people were eating the same spare food three meals a day: beans, bread or some sort of grain porridge, and a little bit of meat for flavor, heavily preserved in salt. This doesn’t sound romantic and old-fashioned; it sounds tedious and unappetizing. But it was all they could afford, and much of the time, there wasn’t quite enough of that.

These were not the nation’s dispossessed; they were the folks who had capital for seed and farm equipment. There were lots of people in America much poorer than the Ingalls were. Your average middle-class person was, by the standards of today, dead broke and living in abject misery. And don’t tell me that things used to be cheaper back then, because I’m not talking about their cash income or how much money they had stuffed under the mattress. I’m talking about how much they could consume. And the answer is “a lot less of everything”: food, clothes, entertainment. That’s even before we talk about the things that hadn’t yet been invented, such as antibiotics and central heating.

Megan McArdle, “When Bread Bags Weren’t Funny”, Bloomberg View, 2015-01-29.

February 11, 2015

Light rail – cool but ultra-expensive. Buses – cheap and flexible but lack glamour

At Mother Jones, Kevin Drum looks at the image problem of buses compared to the seemingly irresistable pull of light rail (at least to municipal politicians looking to overspend and under-deliver):

Josh Barro thinks our cities are building too much light rail. It’s expensive, often slow, and offers virtually no advantage over simply opening up a bus line. The problem, according to a 2009 report from the Federal Transit Administration, is that “Bus-based public transit in the United States suffers from an image problem.” But what if transit agencies tackled that image problem head on?

[…]

So perhaps we need a two-pronged marketing campaign if we want to attract more suburbanites onto buses. They need to be convinced that new bus lines are both bourgeois1 and safe. I might add that although Barro doesn’t highlight this particular feature, the Orange Line mentioned in the report also has “high frequencies.” That’s a key feature too, and it costs money. But it still costs less to run a high-frequency bus than an above-ground light rail system.

Maybe we need more celebrities to ride the bus. I’ll bet if George Clooney took the bus to work, it would suddenly become a lot more popular. You’d probably need to increase service to accommodate all the paparazzi, but surely that’s a small price to pay?

1I confess to some curiosity here. Did focus group participants really refer to the Orange Line as a “bourgeois bus”? That seems a bit unlikely to me.

February 8, 2015

Misallocating infrastructure spending

Randal O’Toole on the problems with directing your infrastructure spending on the basis of ideology rather than economic efficiency:

For the past two decades or so, however, much of our transportation spending has focused on infrastructure that is slower, more expensive, less convenient, and often more dangerous than before. Too many cities have given up on trying to relieve congestion. Instead, they have allowed it to grow while they spend transportation dollars (nearly all paid by auto users) on other forms of travel such as rail transit. Such transportation is:

- Slower: Where highway speeds even in congested cities average 35 miles per hour or more, the rail transit lines built with federal dollars mostly average 15 to 20 mph.

- More expensive: In 2013, Americans auto users spent less than 45 cents per vehicle mile (which means, at average occupanies of 1.67 people per car, about 26 cents per passenger mile), and subsidies to roads average under a penny per passenger mile. By comparison, transit fares are also about 26 cents per passenger mile, but subsidies are 75 cents per passenger mile.

- Less convenient: Autos can go door to door, while transit requires people to walk or use other forms of travel, often at both ends of the transit trip.

- Less safe: For every billion passenger miles carried, urban auto accidents kill about 5 people, while light rail kills about 12 people and commuter trains kill 9. Only subways and elevateds are marginally safer than auto travel, at 4.5, but we haven’t built many of those lately.

Not surprisingly, most transit projects lead to almost no new travel. Yet their backers claim this is a virtue. They have demonized the new travel generated by the interstates by calling it “induced demand.” They have celebrated transportation projects that generate no new travel but merely get people to shift from one mode to another, usually more expensive, mode as “sustainable.”

Even when cities spend money on roads, they often spent it making travel slower, less convenient, and more dangerous. Many cities are doing various forms of what planners euphemistically called “traffic calming,” meaning narrowing streets, putting barriers in roads, and turning one-way streets into two-way streets. The overt goal is to slow down traffic, and it often has the side effect of making it more dangerous for both auto users and pedestrians.

A very simple test can determine whether any particular transportation project will be faster, cheaper, more convenient, and/or safer than before: Will the users themselves pay for it? Users will pay for real improvements in transportation; they won’t pay for slower, more expensive, less convenient, and more dangerous transportation.

February 1, 2015

The diminishing applicability of Marx’s view of the class system

Rick McGinnis on the steadily reducing relationship between the class system as described by Karl Marx and the modern world:

I blame Karl Marx for a lot of things, but after inspiring some of the most destructive and blood-thirsty governments in modern history, his most abidingly destructive legacy is hobbling our understanding of the word “class.” For as long as I’ve been alive, when almost anyone talks about the class system they end up invoking images frozen somewhere in the middle of the European 19th century.

Arrogant entitled aristocrats and heartless mill owners; upright bourgeois, dispirited workers and peasants. It’s a world of frock coats and cloth caps and sunless terraced slums under smoke-filled skies, and while it’s a useful image if you want to start a discussion about the Industrial Revolution, it doesn’t do much to help describe the fluid, amorphous, endlessly adaptable way that class works in the modern world – and probably always has, even if one writer managed to fix the word to a tether at a spot roughly between Jane Austen and Charles Dickens.

Which is why I don’t have much hope that Joel Kotkin’s The New Class Conflict (Telos Press, 220 pages) will do much to budge our discussion of class to a point somewhere closer to the world of suburbs, computers, megamalls, and package vacations. It’s not that Kotkin’s book doesn’t struggle – mostly successfully – to make a discussion about class relevant, but that decades of framing class in antique trappings has made the word and everything it invokes seem anachronistic, or even irrelevant, to modern people and especially Americans.

[…]

Whether intended or not, Kotkin points out that encouraging people to live in crowded cities not only stifles the ownership of private property that’s been a mark of increasing mass material prosperity for two centuries, but it re-creates a renting class at the mercy of moneyed landowners that he describes as a “new feudalism.”

H/T to Kathy Shaidle for the link.

January 31, 2015

QotD: MMO economies

A multiplayer game environment is a dream come true for an economist. Because here you have an economy where you don’t need statistics. And elaborate statistics is what you use when you don’t know everything, you’re not omniscient, and you need to use something in order to gain feeling as to what is happening to prices, what is happening to quantities, what’s happening to investments, and so on and so forth. But in a video game world, all the data are there. It’s like being God, who has access to everything and to what every member of the social economy is doing.

Yanis Varoufakis, talking to Peter Suderman, “A Multiplayer Game Environment Is Actually a Dream Come True for an Economist”, Reason, 2014-05-30.

January 30, 2015

What can Plato’s Cave tell us about basic economics?

Over at Ace of Spades H.Q., Monty takes us back to Philosophy 101 to show the economic version of Plato’s famous story:

If you had occasion to take a Philosophy 101 course in college, you may remember the allegory of Plato’s cave. Plato meant it as a discussion of what “reality” is — whether it is an absolute thing, and whether humans can experience “reality” in its totality or if we are limited only to what we can experience and measure. The idea is that what we can sense and measure is only a subset of a larger reality that we cannot perceive directly.

I’ve long thought that this allegory works quite well for economics in many ways, especially as it pertains to concepts of money and wealth.

Take a dollar out out of your pocket and look at it. What is it? It’s many things, actually: it is money, so it must be a store of wealth, a unit of account, and a medium of exchange; it is a manufactured good, intended by its manufacturer to be used as currency; it is a work of engravers’ art; it is a complex piece of technology (especially modern bills with the various anti-counterfeiting countermeasures); it is a carrier for the oils, dirt, and germs of the people who have handled it; and so on.

You can think of money as a special kind of battery, only instead of storing electricity, it stores up economic value which can be expended at a later time. And just as a battery can store energy but not create it, money can store value but not create it.

It turns out that this dollar bill is a pretty complex object, all things considered. And yet it isn’t a “real” thing in the sense Plato was speaking of. Whatever else it may be, a dollar is not in itself valuable; it is rather a signifier of a real thing we cannot see directly. A unit of money — whether a dollar, a franc, a pound, or a quatloo — is only “real” insofar as it signifies some existing value in the economy. (We can think of some value as being latent as opposed to realized, as it often is with investments. We invest in expectation of value being created and providing some kind of return on the investment. No value appears spontaneously out of the void. The invested capital is based on already-existing assets; a return is only realized if the endeavor creates additional value. Interest income or dividends don’t just magically materialize — interest income is your share of the value added and payment for the time-value of the money you invested. Nothing comes from nothing, as Parmenides reminds us.)

That dollar you hold in your hand is the shadow cast by something of value in the world of real things.*

[…]

* One way in which the Plato’s Cave allegory doesn’t work well in the monetary sense is when considering an essential property of money: fungibility. For money to be money, it must be fungible — that is, a dollar bill is exactly like any other dollar bill in terms of how it behaves in a monetary sense. I can buy a candy bar with any dollar, not just one specific dollar. The Plato’s Cave allegory draws a 1-to-1 linkage between the “real” object we cannot perceive and the shadow we can perceive, but with money it is more like a probabilistic wavefront that only collapses when you spend the dollar.

This means that, in the economic sense, our “shadow” of a real world good or service is not a particular dollar but any dollar.

January 28, 2015

Employment skills at the very basic level

Warren Meyer says what the US needs to do is to make changes to the structure of the working world to allow companies to profitably hire low-skilled workers:

A lot of head scratching goes on as to why, when the income premium is so high for gaining skills, there are not more people seeking to gain them. School systems are often blamed, which is fair in part (if I were to be given a second magic wand to wave, it would be to break up the senescent government school monopoly with some kind of school choice system). But a large portion of the population apparently does not take advantage of the educational opportunities that do exist. Why is that?

When one says “job skills,” people often think of things like programming machine tools or writing Java code. But for new or unskilled workers — the very workers we worry are trapped in poverty in our cities — even basic things we take for granted like showing up on-time reliably and working as a team with others represent skills that have to be learned. Amazon.com CEO Jeff Bezos, despite his Princeton education, still learned many of his first real-world job skills working at McDonald’s. In fact, back in the 1970’s, a survey found that 10% of Fortune 500 CEO’s had their first work experience at McDonald’s.

Part of what we call “the cycle of poverty” is due not just to a lack of skills, but to a lack of understanding of or appreciation for such skills that can cross generations. Children of parents with few skills or little education can go on to achieve great things — that is the American dream after all. But in most of these cases, kids who are successful have parents who were, if not educated, at least knowledgeable about the importance of education, reliability, and teamwork — understanding they often gained via what we call unskilled work. The experience gained from unskilled work is a bridge to future success, both in this generation and the next.

But this road to success breaks down without that initial unskilled job. Without a first, relatively simple job it is almost impossible to gain more sophisticated and lucrative work. And kids with parents who have little or no experience working are more likely to inherit their parent’s cynicism about the lack of opportunity than they are to get any push to do well in school, to work hard, or to learn to cooperate with others.

Unfortunately, there seem to be fewer and fewer opportunities for unskilled workers to find a job. As I mentioned earlier, economists scratch their heads and wonder why there are not more skilled workers despite high rewards for gaining such skills. I am not an economist, I am a business school grad. We don’t worry about explaining structural imbalances so much as look for the profitable opportunities they might present. So a question we business folks might ask instead is: If there are so many under-employed unskilled workers rattling around in the economy, why aren’t entrepreneurs crafting business models to exploit this fact?