BobbyBroccoli

Published Nov 4, 2023For a brief moment, Nortel Networks was on top of the world. Let’s enjoy that moment while we can. Part 1 of 2.

00:00 This is John Roth

02:04 The Elephant and the Mouse

12:47 Pa without Ma

26:27 Made in Amerada

42:15 Right Turns are Hard

57:43 Silicon Valley North

1:07:37 The Toronto Stock Explosion

(more…)

February 27, 2024

The Company that Broke Canada

Comments Off on The Company that Broke Canada

February 2, 2024

QotD: Financial bubbles

That financial markets sometimes go off on one has been noted for centuries now. Dutch Tulips, the South Sea Bubble, Dotcom and more recently Bitcoin have all shown that the lust for easy speculation profits can lead to, well, to financial excess at minimum. Those with an orderly cast of mind like to point out that all of this is waste. If instead the truly wise and clever people – after we’ve installed them in government or at least the bureaucracy – could apportion society’s assets very much better. You know, truly invest in the diversity advisers civilisation so badly needs.

The thing is, economists often disagree at this point. Sure, financial bubbles, they occur. Sure, there’s waste in them. But perhaps the very bubble itself is an either useful or necessary part of the process.

Necessary in that perhaps it needs a mania to get some new technology over the finish line. I tend to think it’s not going to happen with Tesla but it did with Railway Mania. Without speculators searching for easy money the network never would have been built out. Without Dotcom Amazon probably wouldn’t have got funded through the decade it was scratching a living.

It’s also possible that it’s just useful. For the overbuilding in the mania might then leave assets that are repurposed to get other technologies over that finish line into general use. Global Crossing lost a fortune – no, really billions – on building out fibre optic cabling to girdle the world. Which was, after the bankruptcy, bought up by the Googles and the like to carry all this web and video stuff. It’s arguably true that without the previous overinvestment we’d simply never have developed – or perhaps not for decades – such resource and bandwidth-hungry hogs.

Tim Worstall, “Cloud Rendering – The Latest Proof That Investment Bubbles Actually Work”, Continental Telegraph, 2019-03-17.

Comments Off on QotD: Financial bubbles

January 23, 2024

QotD: Shakespeare was apparently a terrible writer, according to Bayesian analysis

First there is the dull, seemingly steady, respectable type, instantiated by Bernie Madoff, who had just the kind of personal gravitas that inspired confidence in the cautious. “Yes,” the cautious type thought as he gazed into Madoff’s calm and wise face, “he is just the type to whom I can safely entrust my money. He knows, if anyone knows, how to make money fruitful and multiply.”‘ His very dullness obscured from the cautious man the fact that he, the cautious man, was as motivated by greed and lust for painless enrichment as the most reckless gambler; and no man wants to think that he is motivated by greed. That is a vice that motivates others, not oneself.

Second there is the flamboyant genius type. For more adventurous investors in search of quick returns, a man like SBF is just the one to follow. His refusal to comply with elementary social conventions, even his wild hair, stood guarantor of his genius. Those who followed SBF as the children followed the pied piper deluded themselves by the following false syllogism:

Geniuses are unconventional.

SBF is unconventional.

Therefore, SBF is a genius.(Actually, even his unconventionality was conventional. Convention is that from which no man can ever fully escape.)

The nature of SBF’s “genius” has come to light in his thoughts of Shakespeare, against whose genius he applies statistical reasoning:

I could go on and on about the failings of Shakespeare … but really I shouldn’t need to: the Bayesian priors are pretty damning. About half the people born since 1600 have been born in the past 100 years, but it gets much worse than that. When Shakespeare wrote, almost all Europeans were busy farming and very few people attended university; few people were even literate — probably as low as ten million people. By contrast there are now upwards of a billion literate people in the Western sphere. What are the odds that the greatest writer would have been born in 1564? The Bayesian priors aren’t very favourable.

One could have a great deal of fun with this argument, for example by proving statistically that Isaac Newton was not one of the greatest physicists who ever lived, and indeed could never really even have existed, because the number of people in his time who could do simple arithmetic was so exiguous. How could he, then, together with Leibniz (another impossibility), have invented the calculus?

By contrast, we could also prove that we are living through a golden age of literature (as of every art) because there are now so many people who know how to write. Of course, our painting must be best because, comparatively speaking, our materials are so cheap and within the range of most people, all of whom have the time to take up painting. Think of how poor Spain was when Velasquez was painting! In Vermeer’s day they didn’t even have flush toilets! How, then, could his paintings be beautiful? Basquiat’s paintings must be much better because now we have electric light.

How could Dickens have been so funny when the infant mortality rate was so high and the life expectancy so low? Therefore, he was not funny. As for Mozart, he didn’t even have an electronic amplifier to his name, so how could his music have been any good? He hadn’t even heard of rap.

One swallow doesn’t make a summer, of course, or one vulture a flock, but one cannot help but remark that SBF was not some poor child who managed, by hook or by crook, to crawl out of a noisome slum, but the child of two professors at Stanford University (admittedly of law) who was himself expensively educated and who was, by the standards of 99.999 percent of all previously existing humanity (to use an SBFian type of statistic), extremely privileged. He was of the elite. His immortal thoughts on Shakespeare would not have been possible without his education, for they certainly would not have occurred to — shall we say — an illiterate illegal immigrant from El Salvador or Honduras.

No, it requires many years of training to come up with arguments such as his. And this in turn raises the question of what is going on in schools and universities (if, that is, SBF is not completely sui generis) that their alumni end up by saying things that make the pronouncements of Azande witch doctors look like those of the latest science. Perhaps — and let us hope that — SBF is not typical of his breed.

Theodore Dalrymple, “The Literary Financier”, New English Review, 2023-10-21.

Comments Off on QotD: Shakespeare was apparently a terrible writer, according to Bayesian analysis

January 13, 2024

The ongoing encrapification of the internet – “When I hear the phrase ‘web platform’ I reach for my gun”

Ted Gioia used to be a techno-optimist, eagerly looking forward to ever-improving online experiences. He, like so many of us, has reluctantly come to the conclusion that those hopes are fading out of sight:

I once loved new technology. I lived in the heart of Silicon Valley for 25 years, and was bursting with enthusiasm for its free-wheeling mission to transform the world — and have some fun along the way.

When the Worldwide Web made its debut, I thought I’d found Nirvana. It was like tech was turning everything into a game.

But look at me now. When I hear the phrase “web platform” I reach for my gun.

Where did it go wrong? Did I just get old and embittered? Or did something change in the tech world?

Let me share a story that might help us decide.

What kind of business spends hundreds of billions over 10 years — just to get worse?

This is a story about the birth of the search engine.

There were no commercial search engines back in 1993. But a Stanford student named David Filo compiled a list of his 200 favorite websites.

His buddy Jerry Yang helped turn this into an online list. They called it “Jerry’s Guide to the Worldwide Web”. Filo and Yang added new websites every day to their list — and classified them according to categories.

This turned into Yahoo.

Here’s my favorite part of the story: These two students didn’t even know they were running a business.

They did it for fun. They did it out of love. They did it because it was cool. “We wanted to avoid doing our dissertations”, Yang later explained.

But a venture capitalist named Mike Moritz heard about Filo and Yang, and tracked them down. The founders of Yahoo were living in total squalor in a trailer littered with stale food and pizza boxes, strewed alongside sleeping bags and overheating computers. A phone rang constantly — but nobody bothered to pick it up.

Moritz was dismayed by this dorm-room-gone-wild ambiance, but he was impressed with the students’ web searching technology. So he asked them the obvious question: How much did they plan to charge users?

Filo and Yang had no answer for this. They wanted to give their tech away for free.

Yahoo wasn’t even selling ads back then. It wasn’t tracking users and selling their private information. It didn’t even have a bank account.

But it was a community and had millions of users.

That was a word you heard frequently in Silicon Valley in the early days. People didn’t build web platforms — they formed online communities.

It was a FUN community. People enjoyed being a member. Even the absurd name Yahoo was part of the game — although early investors hated it.

Yang’s job title was “Chief Yahoo”. Filo’s position was “Cheap Yahoo”.

Investors always hate those kinds of things.

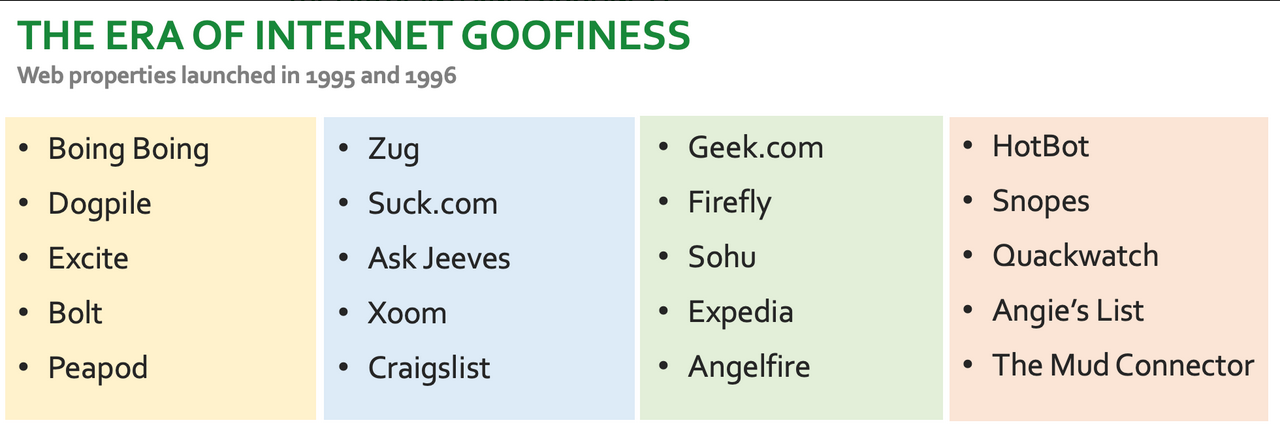

But a new web business, back then, was expected to have a silly name. Here are some of the websites launched in the mid-1990s.

Moritz wanted to turn Yahoo into a business. And the founders realized that their fun community was growing faster than they could handle in their down-and-out trailer. So they sold out 25% of Yahoo for $1 million.

Comments Off on The ongoing encrapification of the internet – “When I hear the phrase ‘web platform’ I reach for my gun”

November 20, 2023

The latest scam – Natural Asset Companies (NACs)

Elizabeth Nickson on the US Securities and Exchange Commission’s plan to magic up some new ways to “financialize” national parks and other federally regulated places for the benefit of the hyper-wealthy and well-connected:

Soon to be a financially performing asset of BlackRock?

Grand Canyon of the Yellowstone, 21 June 2021. Photo by Grastel via Wikimedia Commons.

Delayed but not stopped, the U.S. government is planning a rule that allows for America’s protected lands, including parks and wildlife refuges, to be listed on the N.Y. Stock Exchange. Natural Asset Companies (NACs) will be owned, managed, and traded by companies like BlackRock, Vanguard, and even China.

The deadline was Friday, but earlier this week, the deadline was postponed until January. This is the usual criminal feint from the environmental movement and the administrative state. People are complaining? Let’s put it off till they go back to sleep. Then we will steal their birthright late at night, in precisely the manner we have stolen everything else.

[…]

The entire universe envies the lush interior of the U.S. Increasingly empty, it is filled with a cornucopia of minerals, fiber, food, waters, extraordinarily fertile soil as well as well-ordered, educated, mostly docile people. Worth in the quadrillions, if one could monetize and trade it, financialize it, the way the market has financialized the future labor of Americans, well, it would be like golden coins raining from the sky.

On October 4th, the Securities and Exchange Commission filed a proposed rule to create Natural Asset Companies (NACs). A twenty-one day comment period was allowed, which is half the minimum number of days generally required and when they postponed passing the rule, they did not extend the comment period. “Nope, shut up,” they said.

NACs will allow BlackRock, Bill Gates, and possibly even China to hold the ecosystem rights to the land, water, air, and natural processes of the properties enrolled in NACs. Each NAC will hold “management authority” over the land. When we are issued carbon allowances, owners of said lands will be able to claim tax deductions and will be able to sell carbon allowances to businesses, families and townships. In the simplest of terms, that’s where the money will be made. WE peons will be renting air from the richest people on earth.

The following are eligible for NACs: National Parks, National Wildlife Refuges, Wilderness Areas, Areas of Critical Environmental Concern, Conservation Areas on Private and Federal Lands, Endangered Species Critical Habitat, and the Conservation Reserve Program. Lest you think that any conserved land is conserved in your name, the largest Conservation organization in the U.S., is called The Nature Conservancy, or TNC, which, while being a 501(c)3, also holds six billion dollars of land on its books. Those lands have been taken using your money via donations and government grants, and transferred to the Nature Conservancy, which can do with those lands what it wills.

If this rule passes, America’s conserved lands and parks will move onto the balance sheets of the richest people in the world. Management of those lands will be decided by them and their operations, to say the least, will be opaque.

μολὼν λαβέ, buddy.

Comments Off on The latest scam – Natural Asset Companies (NACs)

November 10, 2023

QotD: Economic distortions of slavery in the Antebellum South

At the end of the day, economies grow and become wealthier as labor and capital are employed more productively. Slavery does exactly the opposite.

Slaves are far less productive than free laborers. They have no incentive to do any more work than the absolute minimum to avoid punishment, and have zero incentive (and a number of disincentives) to use their brain to perform tasks more intelligently. So every slave is a potentially productive worker converted into an unproductive one. Thus, every dollar of capital invested in a slave was a dollar invested in reducing worker productivity.

As a bit of background, the US in the early 19th century had a resource profile opposite from the old country. In Europe, labor was over-abundant and land and resources like timber were scarce. In the US, land and resources were plentiful but labor was scarce. For landowners, it was really hard to get farm labor because everyone who came over here would quickly quit their job and headed out to the edge of settlement and grabbed some land to cultivate for themselves.

In this environment the market was sending pretty clear pricing signals — that it was simply not a good use of scarce labor resources to grow low margin crops on huge plantations requiring scores or hundreds of laborers. Slave-owners circumvented this pricing signal by finding workers they could force to work for free. Force was used to apply high-value labor to lower-value tasks. This does not create prosperity, it destroys it.

As a result, whereas $1000 invested in the North likely improved worker productivity, $1000 invested in the South destroyed it. The North poured capital into future prosperity. The South poured it into supporting a dead-end feudal plantation economy. As a result the south was impoverished for a century, really until northern companies began investing in the South after WWII. If slavery really made for so much of an abundance of opportunities, then why did very few immigrants in the 19th century go to the South? They went to the industrial northeast or (as did my grandparents) to the midwest. The US in the 19th century was prosperous despite slavery in the south, not because of it.

Warren Meyer, “Slavery Made the US Less Prosperous, Not More So”, Coyote Blog, 2019-07-12.

Comments Off on QotD: Economic distortions of slavery in the Antebellum South

October 30, 2023

The rapidly fading market for “song investing”

Ted Gioia called it over two years ago, and now it’s coming true:

The collapse finally came.

When I analyzed the song buyout mania, led by the Hipgnosis fund, back in June 2021, I predicted that this ultra-hot investment trend would “come to an unhappy end”. And now the collapse has arrived.

We’ve reached the endgame. The song fund’s share price has dropped 50% since I made that assessment — and now shareholders have voted to dissolve or reorganize the investment trust.

But where do we go from here? What are old songs really worth? And who will end up owning all these old rock and pop tunes?

Below I offer 12 predictions.

Much of what I have to say is harsh. That’s unfortunate — if I were a real judge, I’d err on the side of leniency. It’s never fun issuing such hardass verdicts. But if I claim to be the Honest Broker, I really have to stick with truths, even when (as in this case) they’re painful truths.

(1) Many musicians still want to sell their songs, but it will be hard to find generous buyers.

Bob Dylan got out at the top, but the times are now a-changin’. Musicians won’t get the big payouts available back in 2021. A telltale sign will be more deals with “undisclosed terms” — because nobody will want to brag about these lowball transactions.(2) Professional financiers have finally learned their lesson.

The two big finance outfits promoting song investing, Hipgnosis and Round Hill, have faltered and will now sell the songs they bought. Sophisticated investors no longer believe the hype. So don’t expect to see the launch of new song investment funds any time soon. The remaining buyers will be bottom fishers and the terminally naive (described in more detail below).[…]

(5) Look out for these vultures in all sectors of the music business.

When private equity firms knock on your door, it’s a sign that you’re already half dead. These folks actually enjoy picking on carcasses — which is easier work than hunting for live prey. I tend to avoid name-calling, but there’s a reason why some folks refer to them as vulture capitalists. That’s their specialty and their economic model is built on bottom-feeding. This is why private equity firms bought up lots of failing local newspaper, struggling local radio stations, etc. Guess what’s next on their list? Expect to see these tough hombres play a bigger role in all aspects of the music business over the next decade.[…]

(7) This whole situation is a case study in misallocated investment capital.

There’s a general lesson here too. I realized, early on in my consulting work, that the single biggest mistake large corporations make is investing too much to keep their old business units alive — when they would be wiser putting that cash to work in new opportunities. The major record labels in the current moment are poster children for exactly this mistaken sense of priorities. They will support the “old songs” business model at all costs — it’s a core part of their self image — but return on investment will be dismal.

Comments Off on The rapidly fading market for “song investing”

September 18, 2023

It turns out that buying up the rights to old rock songs wasn’t a good investment after all

Ted Gioia enjoys a little bit of schadenfreude here because he was highly skeptical of the investments in the first place, although the geriatric rockers who “sold out” seem to have generally made out like bandits this time around:

Back in 2021, investors spent more than $5 billion buying the rights to old songs. Never before in history had musicians over the age of 75 received such big paydays.

I watched in amazement as artists who would never sell out actually sold out. And they made this the sale of a lifetime, like a WalMart in El Paso on Black Friday.

Bob Dylan sold out his entire song catalog ($400 million — ka-ching!). Paul Simon sold out ($250 million). Neil Young sold out ($150 million). Stevie Nicks sold out ($100 million). Dozens of others sold out.

As a result, rock songs have now entered their Madison Avenue stage of life.

Twisted Sister once sang “We’re Not Gonna Take It”. But even they took it — a very large payout, to be specific. A few months ago, the song showed up in a commercial for Discover Card.

Bob Dylan’s song “Shelter from the Storm” got turned into a theme for Airbnb. Neil Young’s “Old Man” was rejuvenated as a marketing jingle for the NFL (touting old man quarterback Tom Brady).

Fans mocked this move. Even Neil Young, now officially a grumpy old man himself, expressed irritation at the move. After all, the head of the Hipgnosis, the leading song investment fund, had promised that the rock star’s “Heart of Gold” would never get turned into “Burger of Gold”.

That hasn’t happened (yet). But where do you draw the line?

I was skeptical of these song buyouts from the start — but not just as a curmudgeonly purist. My view was much simpler. I didn’t think old songs were a good investment. […] But even I didn’t anticipate how badly these deals would turn out.

The more songs Hipgnosis bought, the more its share price dropped. The stock is currently down almost 40% from where it was at the start of 2021.

Things have gotten so bad, that the company is now selling songs.

On Thursday, Hipgnosis announced a plan to sell almost a half billion dollars of its song portfolio. They need to do this to pay down debt. That’s an ominous sign, because the songs Hipgnosis bought were supposed to generate lots of cash. Why can’t they handle their debt load with that cash flow?

But there was even worse news. Hipgnosis admitted that they sold these songs at 17.5% below their estimated “fair market value”. This added to the already widespread suspicion that current claims of song value are inflated.

Comments Off on It turns out that buying up the rights to old rock songs wasn’t a good investment after all

August 11, 2023

The Weirdest Boats on the Great Lakes

Railroad Street

Published 5 May 2023Whalebacks were a type of ship indigenous to the Great Lakes during the late 1890s and mid 1900s. They were invented by Captain Alexander McDougall, and revolutionized the way boats on the Great Lakes handled bulk commodities. Unfortunately, their unique design was one of the many factors which led to their discontinuation.

(more…)

Comments Off on The Weirdest Boats on the Great Lakes

July 28, 2023

QotD: “Stakeholder” Capitalism

Of course, nobody participating in the push to replace shareholder capitalism with stakeholder capitalism would describe it this way. But then, euphemism and branding are each crucial tools in the Marxist’s verbal toolbox. So when you ask a stakeholder capitalist to describe stakeholder capitalism, what you ordinarily hear is that, as a business ethic, it combines the “sustainability” shareholder capitalism supposedly lacks with the “inclusivity” we’re not supposed to recognize is merely stultifying, policed conformity, the yield being a Woke capitalism that replaces production and consumption with “sharing and caring,” taking it out of the realm of the invisible and mechanical, as Adam Smith would have it, and placing it into the realm of values, where it can be used to shape the Greater Good the Marxist pretends he cares about. It’s fascism with a smiley face.

In the stakeholder capitalist system, investors aren’t — or at least, they shouldn’t be — solely interested in profits driven by production and consumption. And this is because to the stakeholder capitalist, itself a euphemism for collectivist corporatist, “it is well proven that our current form of Capitalism is inherently unsustainable because it requires endless growth on a planet with finite resources.”

Of course, none of this is “well proven” — the history of shareholder capitalism suggests the opposite, in fact, as innovation has led to the production of more and more out of less and less — but whether this is or isn’t the material case is incidental to those who are working on this inorganic worldwide paradigm shift commonly known as The Great Reset.

Because the move toward a “caring and sharing” worldwide economy, especially one that we’re told will be both sustainable and inclusive, requires those who care, those who share, and — most importantly, and at the very heart of the turn — those who get to determine what is cared about, who must do the sharing, and how most effectively to police the excesses that the ruling elite determine aren’t sustainable, while slowly dissolving the idea of the individual and his will to make way for an inclusive collective required to run the machinery of the self-installed Elect. It’s a global system of neo-Feudalism dressed in the finery of familiar values that have been deconstructed and re-signified, often without their consumers even aware that the values they reference — which were once commonly understood and largely shared by the civil society — are now their precise inverse: “tolerance”, thus, becomes the violent rejection of intolerance, as they define it; free speech is separated from “hate speech”, as they adjudicate it; individualism is but a controlling fiction maintained by the white male power structure that must be replaced by an ordered and value-determined collection of identity markers that construct you, while simultaneously acknowledging that there is no “you” beyond this assembly of discourses that assign your being its social situatedness, then places you within a collective of those with similar — though never identical — constructions. Once here, you are graded on the intersectional scale. Your relative worth and power come down to not to the content of your character, but rather to the collection and arrangement of your victimization tokens.

Jeff Goldstein, “Maybe I’ll be there to shake your hand, maybe I’ll be there to stakeholder capitalist the land”, protein wisdom reborn!, 2023-04-26.

Comments Off on QotD: “Stakeholder” Capitalism

June 12, 2023

“The more recent four or five years at Indigo have been a disastrophe”

In the latest SHuSH newsletter, Ken Whyte outlines the rise and fall of Canada’s biggest bookstore chain that stopped trying to be a bookstore chain and now appears to be looking for a new identity to assume in the wake of several board resignations and the announced resignation of Heather Reisman, the founder and public face of the chain:

“Indigo Books and Music” by Open Grid Scheduler / Grid Engine is licensed under CC0 1.0![]()

![]()

Indigo opened its first bookstore in Burlington in 1997 and quickly expanded across the country in competition with the Chapters chain, which it bought in 2001. Heather’s husband, Gerry Schwartz, provided much of the financing in these years. Gerry is the controlling shareholder of Onex, a private equity firm that now has about $50 billion in assets under management.

Influential in Ottawa, the Schwartz-Reismans managed to convince the federal government to approve Indigo’s purchase of Chapters and also keep the US book chain Borders from moving north into Canada — a double play that cleared the field of meaningful competition and wouldn’t have happened in a country with serious antitrust enforcement.

Heather, as Indigo CEO, cast herself as the queen of Canadian literature, making personal selections of books to her customers, hosting book launches, interviewing celebrity authors, etc.

From a financial perspective, Indigo took about five years to get rolling after the Chapters acquisition. It looked steady through the late aughts and into the teens when Amazon showed up in force. Indigo’s share price caved. Unable to convince Ottawa to push Amazon back across the border, Heather adopted a new strategy, backing out of books and recasting Indigo as a general merchandiser selling cheeseboards, candles, blankets, and a lot of other crap to thirtyish women. “We built a wonderful connection with our customers in the book business,” she famously said. “Then, organically, certain products became less relevant and others were opportunities.” This charmed investors, if not the book community, and Indigo’s share price hit a high of $20 a share in 2018. By then, books, as a share of revenue, had fallen from 80 percent of revenue to below 60 percent (they are now 46 percent).

The more recent four or five years at Indigo have been a disastrophe. With its eighty-eight superstores and eighty-five small-format stores, the company lost $37 million in 2019, $185 million in 2020, and $57 million in 2021. Things looked somewhat better in 2022 with a $3 million profit, but its first three quarters of 2023 (Indigo has a March 28 year-end) resulted in an $8 million loss and its fourth quarter featured one of the most spectacular cyberhacks in Canadian commercial history. The company’s website was breached and its employment records held for ransom, resulting in a ten-day blackout for all of the company’s payment systems and a month-long outage in online sales. The share price is now $2.00 or one tenth the 2018 high.

ANALYSIS AND IRRESPONSIBLE SPECULATION

Given everything Indigo has been through over the last several years, and especially the last several months, it’s not surprising that Heather wants to pack it in. She’s seventy-four and super wealthy. There’s nothing but a desperately hard slog ahead for her money-losing company. Why stay?

Still, this has the feel of something that blew up at a board meeting, or in advance of a board meeting. It’s highly irregular for a company to lose almost half its directors in a single day. If these changes had been approached in conventional fashion, there would have been more in the way of messaging and positioning, especially regarding Heather. For all intents and purposes, she is Indigo. It wouldn’t exist without her. They ought to be throwing her a retirement parade and presenting her with a golden cheeseboard. Instead, all she’s getting, for now, are a few cliches in a terse press release.

It’s also weird that this all happened days before we get the company’s year-end results (they were out by this time last year). My guess is that the board got a preview, that the picture is ugly, that there are big changes afoot, and that the directors were nudged out as the start of a major retrenchment or given the option of sticking around for a bloodbath and chose instead to exit.

Comments Off on “The more recent four or five years at Indigo have been a disastrophe”

June 9, 2023

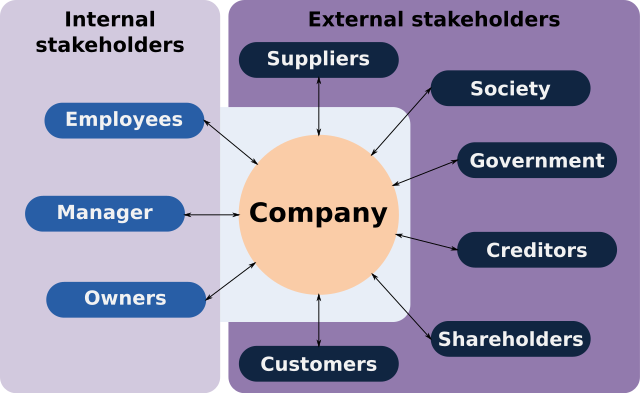

Putting an end to “stakeholder” capitalism

The Streetwise Professor explains what “stakeholder capitalism” is and why it needs to be staked through the heart to save western economies:

A graphic from Wikipedia showing typical internal and external stakeholders.

At its root, stakeholder capitalism represents a rejection – and usually an explicit one – of shareholder wealth maximization as the sole objective and duty of a corporation’s management. Instead, managers are empowered and encouraged to pursue a variety of agendas that do not promote and are usually inimical to maximizing value to shareholders. These agendas are usually broadly social in nature intended to benefit various non-shareholder groups, some of which may be very narrow (transsexuals) or others which may be all encompassing (all inhabitants of planet earth, human and non-human).

This system, such as it is, founders on two very fundamental problems: the Knowledge Problem and Agency problems.

The Knowledge Problem is that no single agent possesses the information required to achieve any goal – even if universally accepted. For example, even if reducing the risk of global temperature increases was broadly agreed upon as a goal, the information required to determine how to do so efficiently is vast as to be unknowable. What are the benefits of a reduction in global temperature by X degrees? The whole panic about global warming stems from its alleged impact on every aspect of life on earth – who can possibly understand anything so complex? And there are trade-offs: reducing temperature involves cost. The cost varies by the mix of measures adopted – the number of components of the mix is also vast, and evaluating costs is again beyond the capabilities of any human, no matter how smart, how informed, and how lavishly equipped with computational power. (Daron Acemoğlu, take heed).

[…]

Agency problems exist when due to information asymmetries or other considerations, agents may act in their own interests and to the detriment of the interests of their principals. In a simple example, the owner of a QuickieMart may not be able to monitor whether his late-shift employee is sufficiently diligent in preventing shoplifting, or exerts appropriate effort in cleaning the restrooms and so on. In the corporate world, the agency problem is one of incentives. The executives of a corporation with myriad shareholders may have considerable freedom to pursue their own interests using the shareholders’ money because any individual shareholder has little incentive to monitor and police the manager: other shareholders benefit from, and thus can free ride on, any individual’s efforts. So managers can, and often do, get away with extravagant waste of the resources owned by others placed in their control.

This agency problem is one of the costs of public corporations with diffuse ownership: this form of organization survives because the benefits of diversification (i.e., better allocation of risk) outweigh these costs. But agency costs exist, and increasing the scope of managerial discretion to, say, saving the world or achieving social justice inevitably increases these costs: with such increased scope, executives have more ways to waste shareholder wealth – and may even get rewarded for it through, say, glowing publicity and other non-pecuniary rewards (like ego gratification – “Look! I’m saving the world! Aren’t I wonderful?”)

H/T to Tim Worstall for the link.

Comments Off on Putting an end to “stakeholder” capitalism

March 18, 2023

Tales of the Metaverse

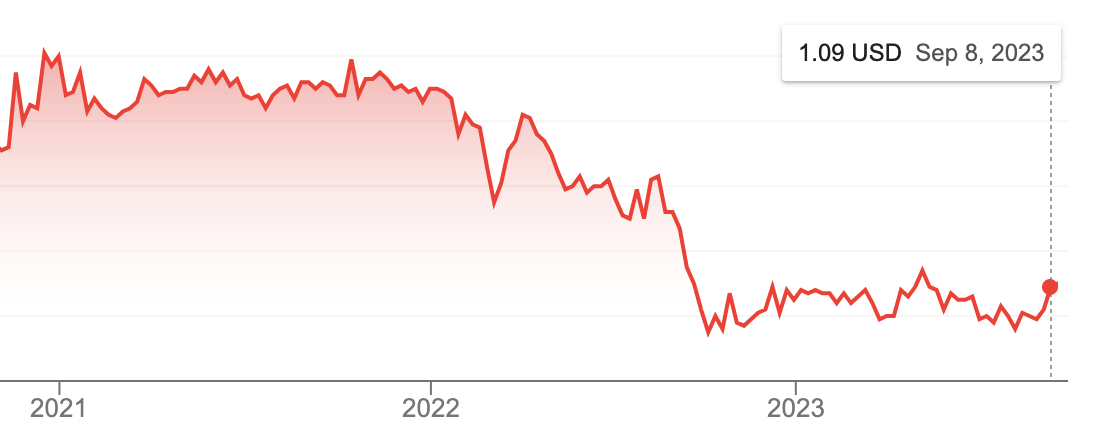

Ted Gioia wonders if Metaverse is doing badly enough to seriously harm Facebook itself:

![]()

When Facebook changed it’s name to Meta back in 2021, I made a gloomy prediction:

“Meta is for losers,” I announced. “Mark Zuckerberg is betting his company on a new idea — but this is a wager he will almost certainly regret.”

I revisited the situation in December, and pointed out all the ways Meta wasn’t just dying in the metaverse. It was also ruining its base business, the Facebook platform.

The company kept making the same mistake as so many other aging websites — instead of serving users they want to control them. The end result is a seeming paradox: the more money the company spends, the worse the user experience becomes.

In the article, I gave a dozen examples — and after it was published many readers shared their own horror stories.

Here’s just one anecdote, out of many:

Try to sign up for Facebook Dating and then try to leave. They won’t let you. A friend of mine recently used it, and now is unable to remove herself totally from the feature. She was allowed to remove all of her pictures, however, she was not permitted to remove her dating profile and picture, which really distressed her. She didn’t want any record of it.

What a great concept. You can meet somebody special, fall in love, get married, and raise a family — but years later you’re still on the Facebook dating app.

It seems ridiculous. But Meta really, really doesn’t like you to opt out of features. Their dream is to operate a virtual Hotel California, where — as the lyrics warn, “you can check out any time you want, but you can never leave”.

Hey, maybe that’s why Mark Zuckerberg won’t let you have legs in his metaverse.

Why isn’t this bold new strategy working? It certainly isn’t for lack of investment. Meta is reportedly spending one billion dollars per month on the project.

But sometimes you can fail even with the right concept — simply because the technology just isn’t ready for the mass market.

[…]

A year-and-a-half after his corporate makeover, the situation at Meta is more dire than ever. Back in October 2021, Facebook shares were trading above $340, but now they are below $200 — that’s a loss of around $300 billion in market value.

But here again, the real problem is the user experience.

“On my initial visits, the metaverse seems sort of desolate, like an abandoned mall,” writes Paul Murray in New York magazine.

[…]

Mark Zuckerberg seems hellbent on pursuing an even more embarrassing fate. His bet on the metaverse may turn into the biggest cash sinkhole in the history of capitalism. Already the Edsel and New Coke look like tiny peccadilloes by comparison.

Even if he keeps his job, he may want to go hide. Fortunately, he has a huge metaverse at his disposal where that has become surprising easy to do.

Comments Off on Tales of the Metaverse

February 7, 2023

Disney – An Empire In Collapse

The Critical Drinker

Published 6 Feb 2023Disney isn’t looking too healthy these days, with massive financial losses, collapsing stock prices and internal power struggles threatening to tear the House of Mouse apart at the seams. How did this happen? Let’s find out.

(more…)

Comments Off on Disney – An Empire In Collapse

November 13, 2022

Corruption in US politics? Where’s the fainting couch?

Elizabeth Nickson looks at several recent books covering political corruption in US politics:

Whitney Webb’s One Nation under Blackmail published late last month, explains in exhaustive detail how the American government was taken over by well-dressed thieves. Webb writes from the left, but she is dispassionate. In 1,000 pages, she explains the history of the turning of democracy, starting post WW2 with the heinous Dulles brothers, moving through Reagan with country club thugs calling themselves The Enterprise, to Jeffrey Epstein’s seduction of Bill and Hillary Clinton. Promising riches beyond their imaginings, the seduction led the couple, by increments, to sell out the country to China and Wall Street.

Webb explains how Epstein set up the Clinton and Gates Foundations promising a new iteration in “charity”, one that made profits, and pushed forward the founders as Saviours. Clinton in her years as Sec State, flew around the world eating brownies and demanding tithes for herself, in return for every beneficence she gave courtesy of the American taxpayer. The ’08 crisis was brought to us by the same crooks, and the same methods, chipping away at regulation. The head Fannie and Freddie Mae bureaucrat, James A Johnson walked away with $100 million leaving the world in crisis. Tens of millions lost everything.

Add this to [Profiles in Corruption] Peter Schweizer’s extraordinary detailing of how Pelosi etc. made their hundreds of millions using taxpayer money, pinpointed deregulation and insider trading.

Schweizer describes how the mega-criminal dealing of the Bidens with China and the Ukraine has walked us into a potential nuclear conflict with both Russia and China. The Lords of Easy Money shows how Wall Street and all the pension funds, all the index funds, have been rolling over corporate debt and taking profits, then borrowing more, selling, borrowing more, selling, and repeat. Which means that every American enterprise that is traded and somehow functional, is laden with corporate debt it cannot possibly pay the interest on, as interest rates rise. Jay Powell made his $50 million that way.

Webb shows how Epstein coached Gates through invading and then purchasing public health both at home and through the UN. Add in the Covid mess, and another bunch of corporate and government thieves walked away with $3 Trillion, in the US alone.

Do you really think they’d allow the endless prosecutions they deserve? Do you really think they want to give back the money they stole?

Comments Off on Corruption in US politics? Where’s the fainting couch?