In the Times Literary Supplement, David Wootton reviews Enlightenment Now: A manifesto for science, reason, humanism and progress by Steven Pinker:

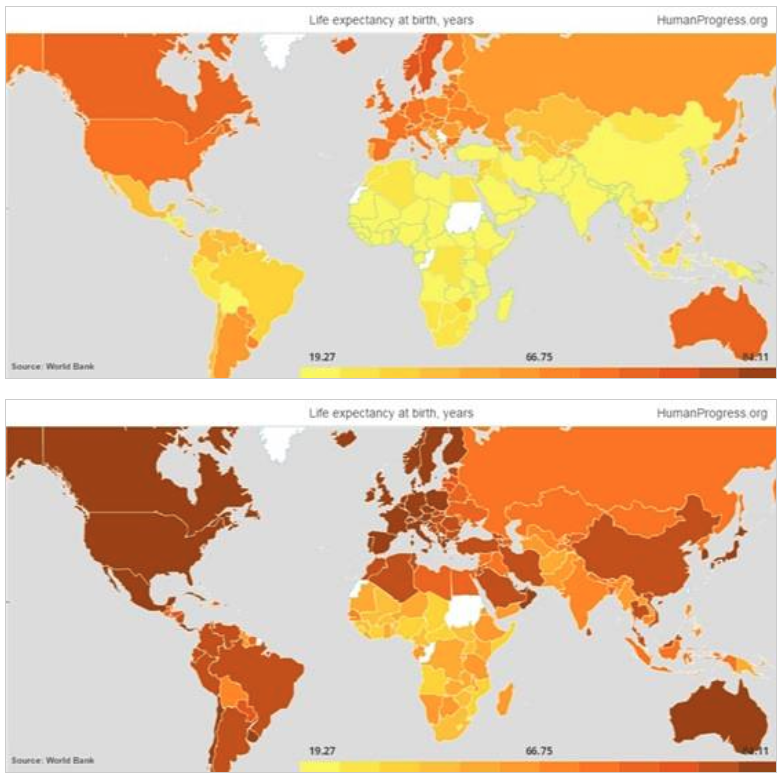

This book consists essentially of seventy-two graphs – and, despite that, it is gripping, provocative and (many will find) infuriating. The graphs all have time on the horizontal axis, and on the vertical axis something important that can be measured against it – life expectancy, for example, or suicide rates, or income. In some graphs the line, or lines (often the graphs compare trends in several countries) fall as they go from left to right; in others they rise. In every single one, the overall picture (with the inevitable blips and bounces) is of life getting better and better. Suicide rates fall, homicides fall, incomes rise, life expectancies rise, literacy rates rise and so on and on through seventy-two variations. Most of these graphs are not new: some simply update graphs which appeared in Pinker’s earlier The Better Angels of Our Nature (2011); others come from recognized purveyors of statistical information. The graphs that weren’t in Better Angels extend the argument of that book, that war and homicide are on the decline across the globe, to assert that life has been getting better and better in all sorts of other respects. The claim isn’t new: a shorter version is to be found in Johan Norberg’s Progress (2017). But the range and scope of the evidence adduced is new. The only major claim not supported by a graph (or indeed much evidence of any kind) is the assertion that all this progress has something to do with the Enlightenment.

Since the argument of the book is almost entirely contained in the graphs, those who want to attack the argument are going to attack the figures on which the graphs are based. Good luck to them: arguments based on statistics, like all interesting arguments, should be tested and tested again. Better Angels caused a vitriolic dispute between Pinker and Nassim Nicholas Taleb as to whether major wars are becoming less frequent. In Taleb’s view the question is a bit like asking whether major earthquakes are getting less frequent or not: they happen so rarely, and so randomly, that you would need records going back over a vast stretch of time to reach any meaningful conclusion; a graph showing falling death rates in wars over the past seventy years won’t do the job. But it certainly will tell you that lots of generalizations about modern war are wrong. Much, indeed most, of Pinker’s argument survived Taleb’s attack, which in any case was directed at only one graph among many.

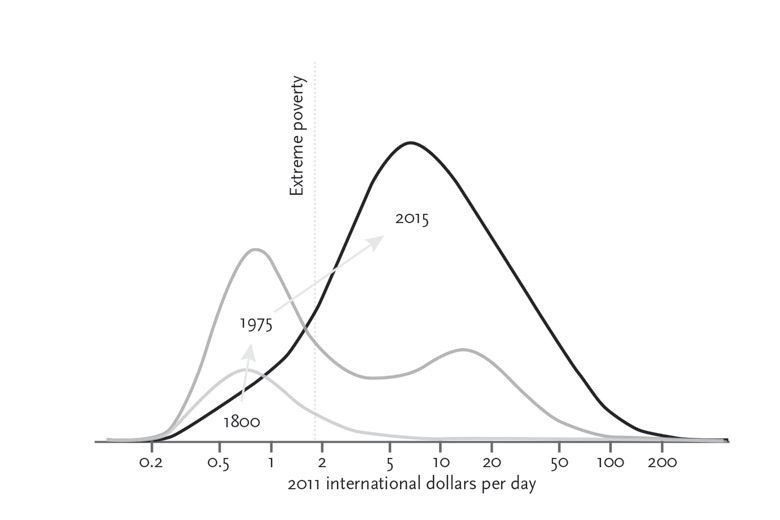

A more radical line of criticism of Better Angels came from John Gray. How can one find a common standard of measurement for the suffering of a concentration camp victim, of a soldier who died in the trenches, and of someone killed in the firebombing of Dresden? To turn to economics, how can one find a common standard of measurement for books and washing machines, oranges and steak pies? Money, you might think, provides that standard, but what happens if many of the goods being measured – electric lighting, cars, televisions, computers – get cheaper and cheaper as time goes on, so that a rising standard of living is concealed by falling prices? For Gray, to place one’s faith in statistics, which claim to be measuring the unmeasurable, is no different from believing in conversations with angels or in the efficacy of Buddhist prayer wheels. Quantification is our religion.