Spartacus has had enough. He has been taken advantage of for too many years and he has suffered trade deficits for far too long. Complaints to the regulators have fallen on deaf ears so now time has come to take the necessary action to put this to an end.

For far too long, Spartacus has run a significant trade deficit with Woolworths and Coles; not only for groceries but for petrol also.

Spartacus keeps buying things from Woolworths and Coles but they never buy anything from him. Those bastards even occasionally “dump” products in their stores meaning that Spartacus can buy groceries for less than he would normally. This is completely unsatisfactory.

Effective immediately, pursuant to SEO 1 (Spartacus Executive Order 1), Spartacus has declared a trade war on Woolworths and Coles. Hence forth, rather than buying quality and (relatively) well priced groceries from these trade cheaters, Spartacus will grow his own fruit, vegetables and meat. And rather than buying petrol, Spartacus will walk or otherwise ride his 2 wheeled chariot. Importantly also, when it comes to paper products, particularly of the toilet paper variety, well, the Fairfax papers will be used for their natural purpose.

Yes. Spartacus will have less leisure time, less disposable income and less grocery choice, but he will no longer have a trade deficit with Woolworths and Coles. This is a trade war Spartacus can win.

And if a sore “butt” comes to pass, what would be colonic damage. Sorry. Collateral damage.

“Spartacus”, “Spartacus’ Trade War”, Catallaxy Files, 2018-03-11.

April 3, 2018

QotD: How to win a trade war

March 30, 2018

QotD: “Progressive” eugenicists

Although their ethics were appalling, “Progressive” eugenicists of the late 19th and early 20th centuries at least got their economic analysis correct: they understood that forcibly raising employers’ cost of employing certain kinds of labor would reduce the quantity of that labor that is employed. This correct economic understanding was at the foundation of these “Progressives’” support for minimum wages; these “Progressives” explicitly wanted to keep people that they regarded as ‘undesirable’ from working.

I say (and believe) that these “Progressives’” ethics were appalling. Yet I’m quite sure that they did not see themselves as monsters. They surely believed themselves to be enlightened, humane, and highly ethical. They believed that they worked for a larger cause – “social reform” – and saw eugenics, minimum wages, and other uses of state force as progressive means of improving humankind through social engineering. One lesson here is that people convinced that they have a mission to improve society by helping forcibly to re-arrange that society so that it conforms to some pre-conceived image are dangerous brutes (if ones that wear suits) whose brutality is hidden from them by their consciously held good intentions and masked from their contemporaries, ironically, by the grand scale (‘society’) upon which they propose to implement their schemes. (If Bill pokes a gun at his neighbor Betty and threatens to shoot Betty if she pays any of her workers less than $7.25 per hour, Bill is rightly recognized as a brute who belongs in prison. Yet if Bill persuades a uniformed and well-armed gang to threaten to shoot, not just Betty, but everyone in the state who employs workers at wages lower than $7.25 per hour, Bill is celebrated as a humane social reformer who belongs in public office. It’s damn bizarre.)

Don Boudreaux, “Quotation of the day…”, Café Hayek, 2016-07-16.

March 29, 2018

March 28, 2018

QotD: Rent-seeking through “health concern” trolling

Producers too often shamelessly use whatever excuses are at hand to justify their prodding the state to prevent consumers from patronizing rival producers. Trumped-up health ‘concerns’ are a prominent set of easy excuses when the good in question is food or drink. “Those foods offered by our rivals are likely to kill or injure our beloved consumers!” cry rent-seeking producers, feigning an overriding concern for the health of the public. “For the health of our citizens, our rival producers must be stopped from selling their foul foods in our market!” Conveniently, of course, when such restrictions are implemented the favored producers no longer must compete as vigorously for consumers’ patronage. (Question: What does diminished competition do to producers’ incentives to maintain the safety of the foods they sell to the public?)

Anyway, here’s a history lesson: today’s expressed concerns about the safety of genetically modified foods and the calls for governments to restrict consumers’ freedom to buy these foods are, in their essence, nothing new. In the late-19th century similar ‘concerns’ over the safety of American beef and pork were used by some beef and pork producers to sic state restriction on rival beef and pork producers. European ranchers and farmers, disliking the competition from American ranchers and farmers, played the safety card as means of securing protection from their American rivals. Likewise within the U.S.: local butchers and local slaughterhouses throughout the U.S. played the same safety card as a means of securing protection from the upstart and wildly successful Chicago meatpackers such as Swift and Armour. That this safety card was illegitimate – that is, that charges of unsafe beef and pork were unwarranted – doesn’t matter if enough people believe the charges. The widely believed myth of dangerous foods enables the state to protect powerful producers from competition.

Cronyism and rent-seeking are nothing new. But they are perhaps becoming more widespread as the scope of state involvement in private affairs expands.

Don Boudreaux, “If Only We Could Be Protected From the Disease of Rent-Seeking”, Café Hayek, 2016-07-14.

March 26, 2018

The container revolution in shipping

Is there anything as ubiquitous as the humble shipping container these days? There’re used for all kinds of “second career” purposes, but it’s easy to miss just how important to the growth in international trade … and the rise in global wealth … those containers have been. Marc Scribner gives a quick shout-out to the container:

Deep-sea containers from China at Ely, Cambridgeshire

Via Wikimedia Commons.

One of the most underappreciated drivers of the modern global economy is the humble shipping container. Widely adopted internationally in the second half of the 20th century, intermodal containers largely supplanted break bulk cargo — the bags, barrels, pallets, and crates that must be individually loaded and unloaded onto ships, railcars, and trucks.

Intermodal containers are standardized in size and design, allowing them to be stacked onto large container ships, which can transport thousands of containers. In port, containers can be lifted onto railcars and flatbed trucks, enabling quick access to inland distribution centers and manufacturing facilities.

Containerization dramatically reduced costs all around. Fewer dockworkers were needed to load and unload vessels and larger ships were built thanks to stackable containers. Fewer ports were needed to transport an increasing volume of goods and freight insurance rates fell due to their durability and securability.

These transportation cost declines due to containerization have been estimated to have increased the volume of world trade far more than the proliferation of free trade agreements since the end of World War II. This means, according to recent research published in the Journal of International Economics, that while trade policy was important (and CEI is a strong supporter of trade liberalization), technological change in the shipping industry was responsible for enabling more trade among countries than improvements in government policy. It is important to note that for global commerce going forward, however, government policy is likely to be more important as containers have already been widely adopted, particularly in wealthy industrialized countries.

March 22, 2018

QotD: “Sustainability”

Today on the radio I heard an ad for a DC-area supermarket chain that boasts that it now has on sale – as in, selling for a reduced price – “sustainably farmed fish.”

I really dislike the word “sustainable” (and all of its variations) as used today to signal holier-than-thou environmental ‘awareness.’ As Robert Solow said about this concept,

It is very hard to be against sustainability. In fact, the less you know about it, the better it sounds.

But advertising “sustainably farmed fish” – implying, as it does (rather bizarrely), that unsustainably farmed fish are common – is especially annoying. While the absence of property rights in oceans and other large bodies of water, and in uncaught fish, might well lead to overfishing (that is, to a genuinely unsustainable manner of acquiring fish for human consumption), the very essence of a fish farm implies property rights in the fish stocks. And where there are property rights there is sustainability. A fish farmer is no more likely to allow his stock of fish to be depleted than is the owner of Triple Crown winner American Pharaoh to allow his horse to be slaughtered for sport, or than are you to allow the cost of motor oil to prevent you from ever changing the oil in your car.

[…]

It’s depressing that those people who today are most likely to worry about resources being “unsustainable” – people who are most likely to prattle publicly about “sustainability” – are those people who also are most likely to disparage private property rights and to argue for government policies that weaken and attenuate such rights. Such people are those who are most likely to wish to further collectivize the provision not only of environmental amenities such as park space and animal conservation, but also of health care, of education, of housing, and of a host of other private goods and services. Such people also are those who are most likely to protest prices made higher by market forces, and to applaud rent-control and other government-imposed price ceilings on a variety of consumer goods and services.

In short, the people who today howl most frequently and loudly for “sustainability” are those who most frequently and loudly oppose the legal and economic institutions – private property and market-determined prices – that alone reliably promote genuine sustainability.

Don Boudreaux, “‘Sustainability’ is Fishy”, Café Hayek, 2016-07-26.

March 21, 2018

Millennials and economics

In the Continental Telegraph, Tim Worstall views-with-alarm the economic illiteracy of many Millennials:

A most amusing piece over in Salon about how American millennials are certain that capitalism just ain’t gonna be around in the future therefore they see no point in saving for their retirements. Boy, ain’t they gonna get a surprise! One of the larger ones being that an absence of capitalism is going to, as it was before the emergence of the system, make having some savings for old age rather more important than it is now.

But there’s more there, of course there is, this is Salon we’re talking about:

The idea that we millennials’ only hope for retirement is the end of capitalism or the end of the world is actually quite common sentiment among the millennial left. Jokes about being unable to retire or anticipating utter social change by retirement age were ricocheting around the internet long before CNN’s article was published.

Well, that’s a generation shopping in the cat food aisle for their meat requirements in retirement then. But more:

Many millennials expressed to me their interest in creating self-sustaining communities as their only hope for survival in old age;

Certainly, that’s one way to do it. Move back to that pre-capitalist idea of the self-sustaining community which takes care of its oldsters. Be useful to have a name for those sorts of things but fortunately we’ve got one that already fits – families. Go and have those 6 to 8 kids and hope like hell that one stays home to change diapers. You did it for them after all.

I’m pretty sure that’s not how they’d see it if you presented it to them that way…

Dear Lord, has anyone even taught them some Marxism? For what’s being described there is the True Communism that will arrive once we’ve abolished economic scarcity. The thing which will come through the productive powers of bourgeois capitalism. You know, as Karl The Beard insisted? As, arguably, we have by any reasonable historical standard. A recent potter around Primark – yes, I know, not high up the list of fashionable outlets – showed that you could, or can, purchase an historically adequate set of clothing for a person for £100. Two day’s minimum wage labour. One set of clothes for everyday, one for Sunday Best. Including a warm coat and more changes of underwear than was usual back then.

No, seriously, there’s not been a period of human history when clothing – to give but one example – was as cheap as it is now. Not in relation to the effort needed to acquire it at least.

There’s actually a serious argument to be made that true communism has already arrived. Certainly Karl and Friedrich would be astonished at a society rich enough to be able to afford diversity advisers – if societal productive surplus is great enough to support that idea then surely communism has indeed arrived?

Boy, aren’t these millennials going to have a surprise when they grow up? That the Good Old Days are now?

March 20, 2018

QotD: “Trade-adjustment assistance”

So-called “trade-adjustment assistance” sounds lovely, but this sound is deceptive. Such ‘assistance’ is a policy of socializing losses while keeping gains privatized – which means, therefore, that it is a policy that creates moral-hazard problems. More generally […] the economic and ethical case against trade-adjustment assistance is fraudulent because there is nothing unique about international trade in destroying particular jobs, businesses, and industries. Why should the worker who loses his job in the steel factory to increased imports of steel receive government assistance while the worker who loses her job in the aluminum factory to increased domestic production of carbon-fiber materials be denied such assistance? There is no good reason to treat the two cases differently.

Neither worker is entitled, economically or ethically, to any such ‘assistance.’

Of course, someone might argue that both of these workers should receive government assistance. Apart from such a policy intensifying moral-hazard problems (“Is your firm’s bankruptcy really due to changing patterns of economic activity rather than to your own incompetence as a business owner?”) – and also apart from the need to give such assistance now to the many people who will lose businesses and jobs because of the resulting increase in taxes that must be raised to pay all of this ‘assistance’ (Why should workers and businesses who suffer as a result of changes in government polices be treated differently than those who suffer as a result of changes in private economic activities?) – such a policy of assistance is premised on the false and economically calamitous assumption that the ultimate goal of economic activity is to ensure the well-being of existing producers rather than to satisfy as many consumer desires as possible. The serious pursuit of any such policy would grind the economy to a standstill, and all but the powerful elite into crushing poverty.

Don Boudreaux, “Quotation of the day…”, Café Hayek, 2016-07-14.

March 19, 2018

QotD: Unintended consequences, recycling division

The hallmark of science is a commitment to follow arguments to their logical conclusions; the hallmark of certain kinds of religion is a slick appeal to logic followed by a hasty retreat if it points in an unexpected direction. Environmentalists can quote reams [!] of statistics on the importance of trees and then jump to the conclusion that recycling paper is a good idea. But the opposite conclusion makes equal sense. I am sure that if we found a way to recycle beef, the population of cattle would go down, not up. If you want ranchers to keep a lot of cattle, you should eat a lot of beef. Recycling paper eliminates the incentive for paper companies to plant more trees and can cause forests to shrink.

Steven Landsburg, The Armchair Economist, 1993.

March 17, 2018

Toys ‘R’ Us did for toys what Borders and Barnes & Noble did for books

We have lived through the golden age of the big box store, and the less-fit are now going to the wall. Virginia Postrel looks at the history of Toys’R’ Us and how it changed the toy market:

I wasn’t a Toys ‘R’ Us kid.

By the time the big box wonderland arrived in my hometown, I was a 25-year-old business reporter living 900 miles away. So instead of conjuring up memories of dolls, bikes and video games, the chain’s imminent demise reminds me of what the world was like before it arrived: Most toys were available only around Christmas and even then the choices were limited unless you lived in a big city. We got my doll house in Atlanta.

Toys ‘R’ Us changed that. “They got a million toys at Toys ‘R’ Us that I can play with,” boasted its famous jingle. “The selection — more than 18,000 different toys in every store — is almost inconceivably vast,” wrote David Owen in a 1986 Atlantic article on the toy business. “There’s an enormous opportunity in America if you’re willing to make a commitment to inventory,” founder Charles Lazarus told him.

Indeed there was.

What Toys ‘R’ Us did for toys, Home Depot and Lowe’s did for hardware; Best Buy and Circuit City for electronics and music; Borders and Barnes & Noble for books; Bed, Bath and Beyond and Linens n’ Things for home goods; and Staples, Office Depot and Office Max for office supplies. The rise of category killers in the 1980s accustomed consumers of all ages to unprecedented variety and choice—in any season and just about any locale. In less populated areas, Walmart filled in the gaps.

By internet standards, the selection Owen termed “inconceivably vast” now looks paltry. “I stopped by my local Best Buy to do research, and found they stock something like 30,000 different titles,” I wrote in 1999. Looking at that text today I wondered if the number was a typo. A mere 30,000? Surely there was a missing zero. Or two.

March 16, 2018

Mostly Weekly Series Finale: Creative Destruction

ReasonTV

Published on 14 Mar 2018In the final episode of the webseries, we tackle how markets make and break stuff.

—–

In free and open markets people are able to make new technologies and business models, which displace older, established ones. That process of starting new companies and jobs destroys some professions while creating others.

It’s entirely understandable that people who lose their jobs want to keep them. But industries like manufacturing, coal mining, and mall retailers aren’t dying out because of competition from China, they’re being outmoded by automation, cheaper fuel sources, and online sales.

Despite the uncertainty that markets bring, they also create new jobs and entirely new professions. There aren’t gangs of unemployed lamplighters roaming the land; their descendants became Uber drivers, social media coordinators, and webseries producers.

In the end, it’s better for everyone to look at the world as it is and to move forward than to try and halt progress through the force of law.

Mostly Weekly is hosted by Andrew Heaton with headwriter Sarah Rose Siskind.

Script by Andrew Heaton and Sarah Rose Siskind with writing assistance from Brian Sack.

Edited by Austin Bragg and Sarah Rose Siskind.

Produced by Meredith and Austin Bragg.

Theme Song: Frozen by Surfer Blood.

March 15, 2018

QotD: The self-harming reality of tariffs

Unintended harm to American companies is a recurring problem with tariffs, even those meant to protect American jobs from competition that our government deems unfair. After Bush imposed steel tariffs, steel-consuming industries pointed out that they employed far more Americans than the steel industry itself, and argued that the net effect of the policy on jobs was negative.

Anti-dumping laws, which put tariffs on foreign imports that are supposedly being sold at too low a price, usually target intermediate goods and therefore make the downstream American producers that use them less competitive. Daniel Ikenson, a trade-policy analyst at the Cato Institute, notes that the government, perversely, is forbidden by law from considering the impact of tariffs on these producers before levying the tariffs.

Then there’s the question of costs. Gary Hufbauer and Sean Lowry, a senior fellow and research associate, respectively, at the Peterson Institute for International Economics, calculated [PDF] that Obama’s tariffs on Chinese tires cost American consumers at least $900,000 for every job they saved for one year. That’s before taking account of job losses caused by lower spending by consumers on other products and by retaliatory Chinese tariffs. This very high cost per job, they point out, is consistent with research on other instances of trade protection.

In an interview, Hufbauer notes that our efforts to protect industries from competition have typically not resulted in their revival and impose extremely high costs for any jobs they save. He cites the textile and maritime industries, both of which have been protected for decades, as examples of these disappointing results.

Ramesh Ponnuru, “The High Cost of U.S. Protectionism”, Bloomberg View, 2016-07-01.

March 14, 2018

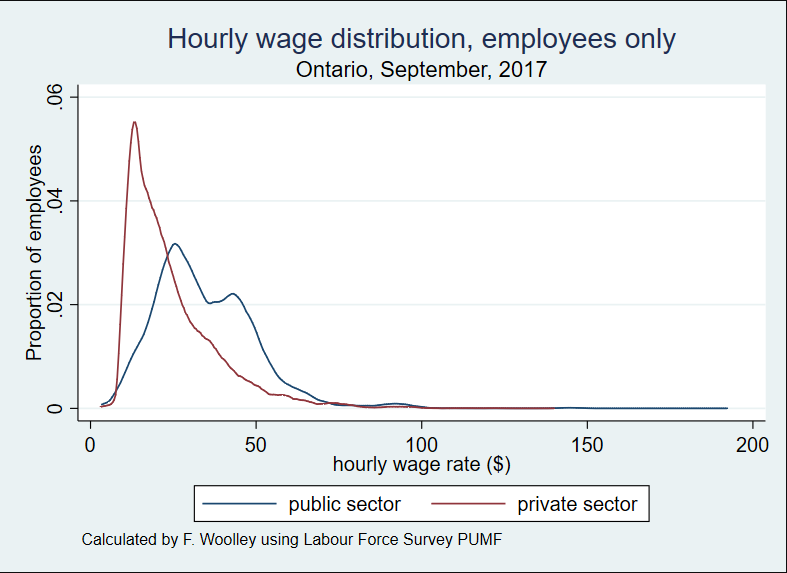

Ontario’s tax dollars at work

At Worthwhile Canadian Initiative, Frances Woolley shows the picture that will define Ontario politics for years to come:

In Ontario, public sector employees earn more than private sector employees. Many workers in the private sector earn the minimum wage, or only slightly above minimum wage. The peak of the public sector earnings distribution is much higher, at twenty-something dollars per hour, and there are a good number of public sector workers earning $40 or $50 an hour.

There are many things missing from this picture. Most importantly, it excludes highly-paid self-employed professionals, such as doctors, lawyers, and accountants, as well as entrepreneurs and business owners. It also excludes self-employed people in the trades, such as plumbers, electricians and contractors. The numbers are non-trivial: 13 percent of Ontario workers are self-employed. A good chunk of the upper part of the private sector earnings distribution is missing from the picture. On the other hand, the hourly wage distribution above excludes non-wage benefits that are more common in the public than the private sector, such as employer contributions to health insurance and pension plans.

Furthermore, the picture does not take into account the differences in the nature of work in the public and private sector. Many public sector jobs, such as nursing, social work, and teaching, require relatively high levels of skill and education. There are private sector jobs that require skill and education as well – but, as noted earlier, many of those jobs are carried out by self-employed professionals, so are not in the graph.

Even noting the exclusions, it’s striking that the old trade-off between public and private sector jobs — that civil servants got lower pay but better benefits and job security — has long since ceased to function. Civil servants, on the whole, now get higher pay than private sector workers, but have retained or even improved the benefits advantage over their private counterparts … and also still retain the job security that private workers can only dream of.

March 13, 2018

The economic argument for carbon taxes

Tim Worstall explains what a carbon tax is supposed to do, as opposed to what many environmental activists want it to do:

The essential economic analysis is that carbon emissions are an “externality.” There are costs to third parties of the freely chosen activities of consenting adults. If there aren’t such third party costs then the adults get to consent – as long as your bedroom contains only those freely consenting adults then what goes on there is up to you. But if there are those third party costs – say, the noise from the enjoyments causes lost sleep among the neighbours – then some societal power to force an adjustment seems reasonable enough.

Again, economics analyses here by suggesting that we’ll get too much, or too many, of those third party costs if people aren’t paying for them. If we’ve not got to pay to soundproof the orgy then we’ll have more orgies than if we do. It’s fair that we insist upon such soundproofing perhaps. But sometimes we cannot insist upon such direct actions – then we’ve got to try and change the price system. Which is what the carbon tax does.

There are benefits to using fossil fuels – transport, heat, cooking and so on. Given current technological levels immediate banning would mean billions die – commonly thought to be a Bad Thing. But there are those costs imposed upon others as well in the climate change the emissions cause. The answer is that we look to that greatest good of the greatest number, the utilitarian answer. Where emissions produce more value than the damage they cause – including over time – then we want them to continue. Where they don’t then we want them to stop. That way we get the maximum possible value being created and thus all humans – over time – are as rich as we can be given current technologies.

Calculating what this number is, this tax rate, is also known as determining the social cost of carbon emissions. The Stern Review may or may not have exactly the right number but it’s a good enough starting point, $80 per tonne CO2. Say 50 cents or so per gallon of gas. Slap that tax on and we’ve corrected the price system. People who use gas are now paying the environmental costs of their use. So, anything they use it for must create greater value than the damage being caused. We’re copacetic at this point, we’ve the optimal level of emissions.

Note that this logic still works whatever you think of the rate. 1 cent or $100 a gallon, the logic is still the same, we’re only arguing over what is that social cost of carbon. Stick a tax on of whatever it is and we’re done.

Even if climate change isn’t a problem, or isn’t happening, we do still need some tax revenues somewhere. It’s also better to tax consumption than incomes or capital, better to tax things inelastic in demand with respect to price than those elastic. Fossil fuel consumption taxation is a consumption tax and the demand for fossil fuels is, in the short to medium term at least, inelastic. We’re fine with fuel taxation therefore.

For a quick backgrounder on the concept of externalities, MR University did a video on this a few years back. For reasons to worry that your government might not be quite as revenue-neutral in imposing a Pigouvian tax, Warren Meyer also has doubts.