This notion that slavery somehow benefited the entire economy is a surprisingly common one and I want to briefly refute it. This is related to the ridiculously bad academic study (discussed here) that slave-harvested cotton accounted for nearly half of the US’s economic activity, when in fact the number was well under 10%. I assume that activists in support of reparations are using this argument to make the case that all Americans, not just slaveholders, benefited from slavery. But this simply is not the case.

At the end of the day, economies grow and become wealthier as labor and capital are employed more productively. Slavery does exactly the opposite.

Slaves are far less productive than free laborers. They have no incentive to do any more work than the absolute minimum to avoid punishment, and have zero incentive (and a number of disincentives) to use their brain to perform tasks more intelligently. So every slave is a potentially productive worker converted into an unproductive one. Thus, every dollar of capital invested in a slave was a dollar invested in reducing worker productivity.

As a bit of background, the US in the early 19th century had a resource profile opposite from the old country. In Europe, labor was over-abundant and land and resources like timber were scarce. In the US, land and resources were plentiful but labor was scarce. For landowners, it was really hard to get farm labor because everyone who came over here would quickly quit their job and headed out to the edge of settlement and grabbed some land to cultivate for themselves.

In this environment the market was sending pretty clear pricing signals — that it was simply not a good use of scarce labor resources to grow low margin crops on huge plantations requiring scores or hundreds of laborers. Slave-owners circumvented this pricing signal by finding workers they could force to work for free. Force was used to apply high-value labor to lower-value tasks. This does not create prosperity, it destroys it.

As a result, whereas $1000 invested in the North likely improved worker productivity, $1000 invested in the South destroyed it. The North poured capital into future prosperity. The South poured it into supporting a dead-end feudal plantation economy. As a result the south was impoverished for a century, really until northern companies began investing in the South after WWII. If slavery really made for so much of an abundance of opportunities, then why did very few immigrants in the 19th century go to the South? They went to the industrial northeast or (as did my grandparents) to the midwest. The US in the 19th century was prosperous despite slavery in the south, not because of it.

Warren Meyer, “Slavery Made the US Less Prosperous, Not More So”, Coyote Blog, 2019-07-12.

November 10, 2023

QotD: Economic distortions of slavery in the Antebellum South

October 30, 2023

The rapidly fading market for “song investing”

Ted Gioia called it over two years ago, and now it’s coming true:

The collapse finally came.

When I analyzed the song buyout mania, led by the Hipgnosis fund, back in June 2021, I predicted that this ultra-hot investment trend would “come to an unhappy end”. And now the collapse has arrived.

We’ve reached the endgame. The song fund’s share price has dropped 50% since I made that assessment — and now shareholders have voted to dissolve or reorganize the investment trust.

But where do we go from here? What are old songs really worth? And who will end up owning all these old rock and pop tunes?

Below I offer 12 predictions.

Much of what I have to say is harsh. That’s unfortunate — if I were a real judge, I’d err on the side of leniency. It’s never fun issuing such hardass verdicts. But if I claim to be the Honest Broker, I really have to stick with truths, even when (as in this case) they’re painful truths.

(1) Many musicians still want to sell their songs, but it will be hard to find generous buyers.

Bob Dylan got out at the top, but the times are now a-changin’. Musicians won’t get the big payouts available back in 2021. A telltale sign will be more deals with “undisclosed terms” — because nobody will want to brag about these lowball transactions.(2) Professional financiers have finally learned their lesson.

The two big finance outfits promoting song investing, Hipgnosis and Round Hill, have faltered and will now sell the songs they bought. Sophisticated investors no longer believe the hype. So don’t expect to see the launch of new song investment funds any time soon. The remaining buyers will be bottom fishers and the terminally naive (described in more detail below).[…]

(5) Look out for these vultures in all sectors of the music business.

When private equity firms knock on your door, it’s a sign that you’re already half dead. These folks actually enjoy picking on carcasses — which is easier work than hunting for live prey. I tend to avoid name-calling, but there’s a reason why some folks refer to them as vulture capitalists. That’s their specialty and their economic model is built on bottom-feeding. This is why private equity firms bought up lots of failing local newspaper, struggling local radio stations, etc. Guess what’s next on their list? Expect to see these tough hombres play a bigger role in all aspects of the music business over the next decade.[…]

(7) This whole situation is a case study in misallocated investment capital.

There’s a general lesson here too. I realized, early on in my consulting work, that the single biggest mistake large corporations make is investing too much to keep their old business units alive — when they would be wiser putting that cash to work in new opportunities. The major record labels in the current moment are poster children for exactly this mistaken sense of priorities. They will support the “old songs” business model at all costs — it’s a core part of their self image — but return on investment will be dismal.

September 18, 2023

It turns out that buying up the rights to old rock songs wasn’t a good investment after all

Ted Gioia enjoys a little bit of schadenfreude here because he was highly skeptical of the investments in the first place, although the geriatric rockers who “sold out” seem to have generally made out like bandits this time around:

Back in 2021, investors spent more than $5 billion buying the rights to old songs. Never before in history had musicians over the age of 75 received such big paydays.

I watched in amazement as artists who would never sell out actually sold out. And they made this the sale of a lifetime, like a WalMart in El Paso on Black Friday.

Bob Dylan sold out his entire song catalog ($400 million — ka-ching!). Paul Simon sold out ($250 million). Neil Young sold out ($150 million). Stevie Nicks sold out ($100 million). Dozens of others sold out.

As a result, rock songs have now entered their Madison Avenue stage of life.

Twisted Sister once sang “We’re Not Gonna Take It”. But even they took it — a very large payout, to be specific. A few months ago, the song showed up in a commercial for Discover Card.

Bob Dylan’s song “Shelter from the Storm” got turned into a theme for Airbnb. Neil Young’s “Old Man” was rejuvenated as a marketing jingle for the NFL (touting old man quarterback Tom Brady).

Fans mocked this move. Even Neil Young, now officially a grumpy old man himself, expressed irritation at the move. After all, the head of the Hipgnosis, the leading song investment fund, had promised that the rock star’s “Heart of Gold” would never get turned into “Burger of Gold”.

That hasn’t happened (yet). But where do you draw the line?

I was skeptical of these song buyouts from the start — but not just as a curmudgeonly purist. My view was much simpler. I didn’t think old songs were a good investment. […] But even I didn’t anticipate how badly these deals would turn out.

The more songs Hipgnosis bought, the more its share price dropped. The stock is currently down almost 40% from where it was at the start of 2021.

Things have gotten so bad, that the company is now selling songs.

On Thursday, Hipgnosis announced a plan to sell almost a half billion dollars of its song portfolio. They need to do this to pay down debt. That’s an ominous sign, because the songs Hipgnosis bought were supposed to generate lots of cash. Why can’t they handle their debt load with that cash flow?

But there was even worse news. Hipgnosis admitted that they sold these songs at 17.5% below their estimated “fair market value”. This added to the already widespread suspicion that current claims of song value are inflated.

August 11, 2023

The Weirdest Boats on the Great Lakes

Railroad Street

Published 5 May 2023Whalebacks were a type of ship indigenous to the Great Lakes during the late 1890s and mid 1900s. They were invented by Captain Alexander McDougall, and revolutionized the way boats on the Great Lakes handled bulk commodities. Unfortunately, their unique design was one of the many factors which led to their discontinuation.

(more…)

July 28, 2023

QotD: “Stakeholder” Capitalism

Of course, nobody participating in the push to replace shareholder capitalism with stakeholder capitalism would describe it this way. But then, euphemism and branding are each crucial tools in the Marxist’s verbal toolbox. So when you ask a stakeholder capitalist to describe stakeholder capitalism, what you ordinarily hear is that, as a business ethic, it combines the “sustainability” shareholder capitalism supposedly lacks with the “inclusivity” we’re not supposed to recognize is merely stultifying, policed conformity, the yield being a Woke capitalism that replaces production and consumption with “sharing and caring,” taking it out of the realm of the invisible and mechanical, as Adam Smith would have it, and placing it into the realm of values, where it can be used to shape the Greater Good the Marxist pretends he cares about. It’s fascism with a smiley face.

In the stakeholder capitalist system, investors aren’t — or at least, they shouldn’t be — solely interested in profits driven by production and consumption. And this is because to the stakeholder capitalist, itself a euphemism for collectivist corporatist, “it is well proven that our current form of Capitalism is inherently unsustainable because it requires endless growth on a planet with finite resources.”

Of course, none of this is “well proven” — the history of shareholder capitalism suggests the opposite, in fact, as innovation has led to the production of more and more out of less and less — but whether this is or isn’t the material case is incidental to those who are working on this inorganic worldwide paradigm shift commonly known as The Great Reset.

Because the move toward a “caring and sharing” worldwide economy, especially one that we’re told will be both sustainable and inclusive, requires those who care, those who share, and — most importantly, and at the very heart of the turn — those who get to determine what is cared about, who must do the sharing, and how most effectively to police the excesses that the ruling elite determine aren’t sustainable, while slowly dissolving the idea of the individual and his will to make way for an inclusive collective required to run the machinery of the self-installed Elect. It’s a global system of neo-Feudalism dressed in the finery of familiar values that have been deconstructed and re-signified, often without their consumers even aware that the values they reference — which were once commonly understood and largely shared by the civil society — are now their precise inverse: “tolerance”, thus, becomes the violent rejection of intolerance, as they define it; free speech is separated from “hate speech”, as they adjudicate it; individualism is but a controlling fiction maintained by the white male power structure that must be replaced by an ordered and value-determined collection of identity markers that construct you, while simultaneously acknowledging that there is no “you” beyond this assembly of discourses that assign your being its social situatedness, then places you within a collective of those with similar — though never identical — constructions. Once here, you are graded on the intersectional scale. Your relative worth and power come down to not to the content of your character, but rather to the collection and arrangement of your victimization tokens.

Jeff Goldstein, “Maybe I’ll be there to shake your hand, maybe I’ll be there to stakeholder capitalist the land”, protein wisdom reborn!, 2023-04-26.

June 12, 2023

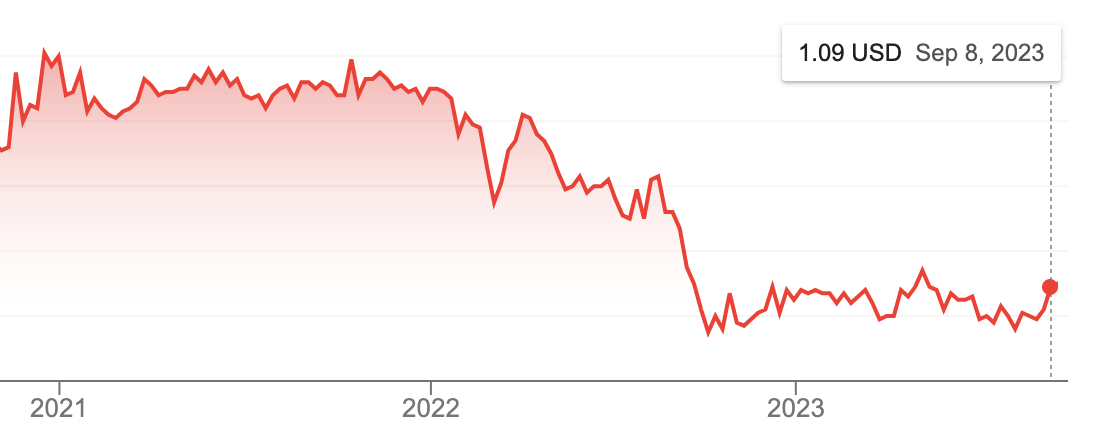

“The more recent four or five years at Indigo have been a disastrophe”

In the latest SHuSH newsletter, Ken Whyte outlines the rise and fall of Canada’s biggest bookstore chain that stopped trying to be a bookstore chain and now appears to be looking for a new identity to assume in the wake of several board resignations and the announced resignation of Heather Reisman, the founder and public face of the chain:

“Indigo Books and Music” by Open Grid Scheduler / Grid Engine is licensed under CC0 1.0![]()

![]()

Indigo opened its first bookstore in Burlington in 1997 and quickly expanded across the country in competition with the Chapters chain, which it bought in 2001. Heather’s husband, Gerry Schwartz, provided much of the financing in these years. Gerry is the controlling shareholder of Onex, a private equity firm that now has about $50 billion in assets under management.

Influential in Ottawa, the Schwartz-Reismans managed to convince the federal government to approve Indigo’s purchase of Chapters and also keep the US book chain Borders from moving north into Canada — a double play that cleared the field of meaningful competition and wouldn’t have happened in a country with serious antitrust enforcement.

Heather, as Indigo CEO, cast herself as the queen of Canadian literature, making personal selections of books to her customers, hosting book launches, interviewing celebrity authors, etc.

From a financial perspective, Indigo took about five years to get rolling after the Chapters acquisition. It looked steady through the late aughts and into the teens when Amazon showed up in force. Indigo’s share price caved. Unable to convince Ottawa to push Amazon back across the border, Heather adopted a new strategy, backing out of books and recasting Indigo as a general merchandiser selling cheeseboards, candles, blankets, and a lot of other crap to thirtyish women. “We built a wonderful connection with our customers in the book business,” she famously said. “Then, organically, certain products became less relevant and others were opportunities.” This charmed investors, if not the book community, and Indigo’s share price hit a high of $20 a share in 2018. By then, books, as a share of revenue, had fallen from 80 percent of revenue to below 60 percent (they are now 46 percent).

The more recent four or five years at Indigo have been a disastrophe. With its eighty-eight superstores and eighty-five small-format stores, the company lost $37 million in 2019, $185 million in 2020, and $57 million in 2021. Things looked somewhat better in 2022 with a $3 million profit, but its first three quarters of 2023 (Indigo has a March 28 year-end) resulted in an $8 million loss and its fourth quarter featured one of the most spectacular cyberhacks in Canadian commercial history. The company’s website was breached and its employment records held for ransom, resulting in a ten-day blackout for all of the company’s payment systems and a month-long outage in online sales. The share price is now $2.00 or one tenth the 2018 high.

ANALYSIS AND IRRESPONSIBLE SPECULATION

Given everything Indigo has been through over the last several years, and especially the last several months, it’s not surprising that Heather wants to pack it in. She’s seventy-four and super wealthy. There’s nothing but a desperately hard slog ahead for her money-losing company. Why stay?

Still, this has the feel of something that blew up at a board meeting, or in advance of a board meeting. It’s highly irregular for a company to lose almost half its directors in a single day. If these changes had been approached in conventional fashion, there would have been more in the way of messaging and positioning, especially regarding Heather. For all intents and purposes, she is Indigo. It wouldn’t exist without her. They ought to be throwing her a retirement parade and presenting her with a golden cheeseboard. Instead, all she’s getting, for now, are a few cliches in a terse press release.

It’s also weird that this all happened days before we get the company’s year-end results (they were out by this time last year). My guess is that the board got a preview, that the picture is ugly, that there are big changes afoot, and that the directors were nudged out as the start of a major retrenchment or given the option of sticking around for a bloodbath and chose instead to exit.

June 9, 2023

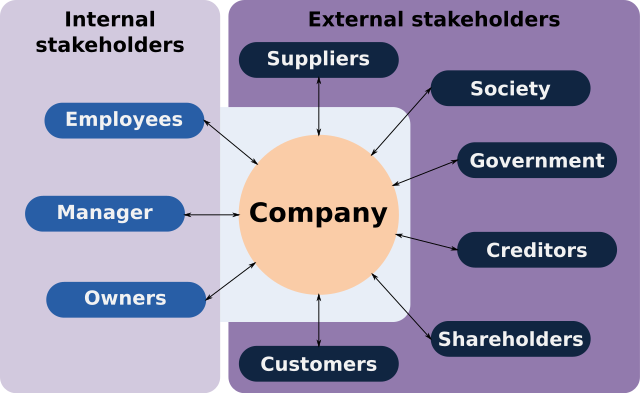

Putting an end to “stakeholder” capitalism

The Streetwise Professor explains what “stakeholder capitalism” is and why it needs to be staked through the heart to save western economies:

A graphic from Wikipedia showing typical internal and external stakeholders.

At its root, stakeholder capitalism represents a rejection – and usually an explicit one – of shareholder wealth maximization as the sole objective and duty of a corporation’s management. Instead, managers are empowered and encouraged to pursue a variety of agendas that do not promote and are usually inimical to maximizing value to shareholders. These agendas are usually broadly social in nature intended to benefit various non-shareholder groups, some of which may be very narrow (transsexuals) or others which may be all encompassing (all inhabitants of planet earth, human and non-human).

This system, such as it is, founders on two very fundamental problems: the Knowledge Problem and Agency problems.

The Knowledge Problem is that no single agent possesses the information required to achieve any goal – even if universally accepted. For example, even if reducing the risk of global temperature increases was broadly agreed upon as a goal, the information required to determine how to do so efficiently is vast as to be unknowable. What are the benefits of a reduction in global temperature by X degrees? The whole panic about global warming stems from its alleged impact on every aspect of life on earth – who can possibly understand anything so complex? And there are trade-offs: reducing temperature involves cost. The cost varies by the mix of measures adopted – the number of components of the mix is also vast, and evaluating costs is again beyond the capabilities of any human, no matter how smart, how informed, and how lavishly equipped with computational power. (Daron Acemoğlu, take heed).

[…]

Agency problems exist when due to information asymmetries or other considerations, agents may act in their own interests and to the detriment of the interests of their principals. In a simple example, the owner of a QuickieMart may not be able to monitor whether his late-shift employee is sufficiently diligent in preventing shoplifting, or exerts appropriate effort in cleaning the restrooms and so on. In the corporate world, the agency problem is one of incentives. The executives of a corporation with myriad shareholders may have considerable freedom to pursue their own interests using the shareholders’ money because any individual shareholder has little incentive to monitor and police the manager: other shareholders benefit from, and thus can free ride on, any individual’s efforts. So managers can, and often do, get away with extravagant waste of the resources owned by others placed in their control.

This agency problem is one of the costs of public corporations with diffuse ownership: this form of organization survives because the benefits of diversification (i.e., better allocation of risk) outweigh these costs. But agency costs exist, and increasing the scope of managerial discretion to, say, saving the world or achieving social justice inevitably increases these costs: with such increased scope, executives have more ways to waste shareholder wealth – and may even get rewarded for it through, say, glowing publicity and other non-pecuniary rewards (like ego gratification – “Look! I’m saving the world! Aren’t I wonderful?”)

H/T to Tim Worstall for the link.

March 18, 2023

Tales of the Metaverse

Ted Gioia wonders if Metaverse is doing badly enough to seriously harm Facebook itself:

![]()

When Facebook changed it’s name to Meta back in 2021, I made a gloomy prediction:

“Meta is for losers,” I announced. “Mark Zuckerberg is betting his company on a new idea — but this is a wager he will almost certainly regret.”

I revisited the situation in December, and pointed out all the ways Meta wasn’t just dying in the metaverse. It was also ruining its base business, the Facebook platform.

The company kept making the same mistake as so many other aging websites — instead of serving users they want to control them. The end result is a seeming paradox: the more money the company spends, the worse the user experience becomes.

In the article, I gave a dozen examples — and after it was published many readers shared their own horror stories.

Here’s just one anecdote, out of many:

Try to sign up for Facebook Dating and then try to leave. They won’t let you. A friend of mine recently used it, and now is unable to remove herself totally from the feature. She was allowed to remove all of her pictures, however, she was not permitted to remove her dating profile and picture, which really distressed her. She didn’t want any record of it.

What a great concept. You can meet somebody special, fall in love, get married, and raise a family — but years later you’re still on the Facebook dating app.

It seems ridiculous. But Meta really, really doesn’t like you to opt out of features. Their dream is to operate a virtual Hotel California, where — as the lyrics warn, “you can check out any time you want, but you can never leave”.

Hey, maybe that’s why Mark Zuckerberg won’t let you have legs in his metaverse.

Why isn’t this bold new strategy working? It certainly isn’t for lack of investment. Meta is reportedly spending one billion dollars per month on the project.

But sometimes you can fail even with the right concept — simply because the technology just isn’t ready for the mass market.

[…]

A year-and-a-half after his corporate makeover, the situation at Meta is more dire than ever. Back in October 2021, Facebook shares were trading above $340, but now they are below $200 — that’s a loss of around $300 billion in market value.

But here again, the real problem is the user experience.

“On my initial visits, the metaverse seems sort of desolate, like an abandoned mall,” writes Paul Murray in New York magazine.

[…]

Mark Zuckerberg seems hellbent on pursuing an even more embarrassing fate. His bet on the metaverse may turn into the biggest cash sinkhole in the history of capitalism. Already the Edsel and New Coke look like tiny peccadilloes by comparison.

Even if he keeps his job, he may want to go hide. Fortunately, he has a huge metaverse at his disposal where that has become surprising easy to do.

February 7, 2023

Disney – An Empire In Collapse

The Critical Drinker

Published 6 Feb 2023Disney isn’t looking too healthy these days, with massive financial losses, collapsing stock prices and internal power struggles threatening to tear the House of Mouse apart at the seams. How did this happen? Let’s find out.

(more…)

November 13, 2022

Corruption in US politics? Where’s the fainting couch?

Elizabeth Nickson looks at several recent books covering political corruption in US politics:

Whitney Webb’s One Nation under Blackmail published late last month, explains in exhaustive detail how the American government was taken over by well-dressed thieves. Webb writes from the left, but she is dispassionate. In 1,000 pages, she explains the history of the turning of democracy, starting post WW2 with the heinous Dulles brothers, moving through Reagan with country club thugs calling themselves The Enterprise, to Jeffrey Epstein’s seduction of Bill and Hillary Clinton. Promising riches beyond their imaginings, the seduction led the couple, by increments, to sell out the country to China and Wall Street.

Webb explains how Epstein set up the Clinton and Gates Foundations promising a new iteration in “charity”, one that made profits, and pushed forward the founders as Saviours. Clinton in her years as Sec State, flew around the world eating brownies and demanding tithes for herself, in return for every beneficence she gave courtesy of the American taxpayer. The ’08 crisis was brought to us by the same crooks, and the same methods, chipping away at regulation. The head Fannie and Freddie Mae bureaucrat, James A Johnson walked away with $100 million leaving the world in crisis. Tens of millions lost everything.

Add this to [Profiles in Corruption] Peter Schweizer’s extraordinary detailing of how Pelosi etc. made their hundreds of millions using taxpayer money, pinpointed deregulation and insider trading.

Schweizer describes how the mega-criminal dealing of the Bidens with China and the Ukraine has walked us into a potential nuclear conflict with both Russia and China. The Lords of Easy Money shows how Wall Street and all the pension funds, all the index funds, have been rolling over corporate debt and taking profits, then borrowing more, selling, borrowing more, selling, and repeat. Which means that every American enterprise that is traded and somehow functional, is laden with corporate debt it cannot possibly pay the interest on, as interest rates rise. Jay Powell made his $50 million that way.

Webb shows how Epstein coached Gates through invading and then purchasing public health both at home and through the UN. Add in the Covid mess, and another bunch of corporate and government thieves walked away with $3 Trillion, in the US alone.

Do you really think they’d allow the endless prosecutions they deserve? Do you really think they want to give back the money they stole?

August 16, 2022

“Penguin Random House is a vampire corporation”

Belatedly, as I was away for the weekend, here’s something from the latest SHuSH newsletter on the Random Penguin court case:

![]()

At the beginning of the millennium, Random House (pre-Penguin) had revenues of $2.3 billion (all US figures) and a profit margin of 9 per cent. At the end of the aughts, it had revenues of 2.3 billion and a profit margin of 9 per cent. It was the biggest publishing company on the planet but it had ceased to grow.

Growth matters, especially to Random House’s parent company, Bertelsmann SE, a public company. People buy shares in publicly listed companies because they believe the entity will grow and produce larger profits in the future, making the share price rise and the investor happy. That is the whole game for public companies.

When an asset at a public company does not contribute to growth it is dead weight. It needs to be fixed or jettisoned.

Bertelsmann decided to fix Random House. In 2012, it struck the richest deal in book publishing history, acquiring 53 per cent of Penguin Books, which it then merged with Random House to make the biggest publisher even bigger.

It was said at the time that the two publishers, with combined revenues of $3.9 billion, would be able to share costs, attract better talent, take more risks, offer new products, develop new markets, and otherwise innovate. Together they would have the scale to stand up to bookselling chains like Barnes & Noble and the massive digital players, Amazon and Apple.

It was a lot of hype, of course. Random House had its pick of talent, all the size it needed to negotiate with Barnes & Noble, and it would never be in the same league as Amazon. Markus Dohle, CEO of Penguin Random House, is lucky to get a mid-level account manager on the phone at Amazon.

But the deal went ahead and expectations for the new Penguin Random House were sky high. They had to be. Bertelsmann’s purchase price valued Penguin at $3.5 billion, or more than twenty times its annual profits of $171 million. Penguin Random House would have to be far more than the sum of its parts to justify that price.

Over the next several years, Bertelsmann doubled down on its bet, scooping up the remaining 47 per cent of Penguin in two separate transactions to eventually own it outright.

Did any of the anticipated magic happen?

The first full year of a combined Penguin Random House was 2014. Revenues were about $4 billion, and that’s where they’ve been ever since (leaving aside a nice bump in 2019, the year of Michelle Obama). Profits are up, which might be considered a good sign. But they didn’t grow as a result of the combined firm’s increased scale, new competitive muscle, better talent, new markets, new products, or innovations. As far as I can tell, the improved profitability was achieved the old-fashioned way: the payroll shrunk from a high of 12,800 to 10,800. Also, e-books and audiobooks improved the profitability of all publishers. And the Obamas each knocked one out of the park.

The point is that seven years down the road, Penguin Random House remained exactly the sum of its parts, minus 2000 workers. The acquisition was a big-time bust. Most of the $3.5 billion purchase price was wasted.

May 1, 2022

The Victorian-era “guarantee fund” model for risky enterprises

In the latest Age of Inventions newsletter, Anton Howes wonders why we don’t have a modern equivalent to the funding mechanism that helped create the Great Exhibition of 1851 and other events that provided benefits to the public without government backing:

The Crystal Palace from the northeast during the Great Exhibition of 1851.

Image from the 1852 book Dickinsons’ comprehensive pictures of the Great Exhibition of 1851 via Wikimedia Commons.

As I’ve mentioned before, exhibitions of industry were not just celebrations of technological progress, but could become engines for progress as well. For the inventors, artists, and engineers who exhibited, the events were a direct inducement to improvement. And for the public who visited, the events exposed them to what was possible, encouraging them to raise their demands as both consumers and citizens, ideally inspiring them to become future innovators too.

But how was it all paid for? Unlike its national-level precursors in France, the Great Exhibition was not a state-run event. Even more remarkably, its organisers also failed to raise anywhere near enough private subscriptions to cover their costs. Instead, they used something that called a “guarantee fund”.

Instead of asking for donations from supporters up-front, the organisers asked them to commit to covering the exhibitions potential losses up to certain amounts — to be paid only if the money was required. Based on the security provided by this crowdsourced guarantee fund, the organisers then raised an ordinary bank loan in order to get the cash they needed to actually hold the event. Crucially, the guarantors didn’t actually have to spend anything unless the event made a loss, and if the event broke even or even made a surplus thanks to ticket fees, then they would never spend a penny at all. (Luckily for them, that’s exactly what happened in 1851, and for many later exhibitions too.)

What’s interesting to me about the guarantee fund is that I can’t quite think of anything quite like it today. There are perhaps more individualised versions of it, like when a neighbour or friend acts as a guarantor for a mortgage. And governments sometimes provide guarantees for certain sectors or industries too. There have also been a few profit-making versions of it in certain industries, where the guarantors potentially get some share of the upside too (“Names” at the Lloyds of London insurance and reinsurance market sounds similar, though even these are disappearing). But I’ve not seen anything like what the Victorians did, essentially using a guarantee fund to leverage philanthropy.

This is surprising to me. It seems like it has a lot of major advantages, especially for those who might want to replicate the exhibitions of industry today, or indeed for any kind of capital-intensive philanthropic endeavour that could eventually be expected in some measure to pay for itself. (I can’t help but think it would be useful in efforts to speed up the de-carbonisation of the economy, for example — a potential application that I’ve been exploring in my conversations with the people at Carbon Upcycling.)

Consider that with a guarantee fund anyone able to afford the risk could considerably increase the philanthropic value of their assets. Say that you could afford to donate £100 right away, but could donate three times that amount at a pinch (e.g. by having to liquidate some funds in shares). You could thus guarantee £100 each to three different causes, potentially without ever actually having to donate it, and knowing that in the worst case scenario you would never have to spend more than the £300 you can afford.

After all, those signing up to the guarantee fund essentially chose what their maximum liability would be if the event were to make a loss. If they were confident in the event’s success, then they probably believed that they would not have to pay anything at all. And if not, they had at least named the maximum donation they might eventually be asked to give.

February 8, 2022

QotD: The East India Company’s rise to power

In many ways the EIC was a model of corporate efficiency: 100 years into its history, it had only 35 permanent employees in its head office. Nevertheless, that skeleton staff executed a corporate coup unparalleled in history: the military conquest, subjugation and plunder of vast tracts of southern Asia. It almost certainly remains the supreme act of corporate violence in world history. For all the power wielded today by the world’s largest corporations – whether ExxonMobil, Walmart or Google – they are tame beasts compared with the ravaging territorial appetites of the militarised East India Company. Yet if history shows anything, it is that in the intimate dance between the power of the state and that of the corporation, while the latter can be regulated, it will use all the resources in its power to resist.

When it suited, the EIC made much of its legal separation from the government. It argued forcefully, and successfully, that the document signed by Shah Alam – known as the Diwani – was the legal property of the company, not the Crown, even though the government had spent a massive sum on naval and military operations protecting the EIC’s Indian acquisitions. But the MPs who voted to uphold this legal distinction were not exactly neutral: nearly a quarter of them held company stock, which would have plummeted in value had the Crown taken over. For the same reason, the need to protect the company from foreign competition became a major aim of British foreign policy.

The transaction depicted in the painting [Wiki] was to have catastrophic consequences. As with all such corporations, then as now, the EIC was answerable only to its shareholders. With no stake in the just governance of the region, or its long-term wellbeing, the company’s rule quickly turned into the straightforward pillage of Bengal, and the rapid transfer westwards of its wealth.

Before long the province, already devastated by war, was struck down by the famine of 1769, then further ruined by high taxation. Company tax collectors were guilty of what today would be described as human rights violations. A senior official of the old Mughal regime in Bengal wrote in his diaries: “Indians were tortured to disclose their treasure; cities, towns and villages ransacked; jaghires and provinces purloined: these were the ‘delights’ and ‘religions’ of the directors and their servants.”

Bengal’s wealth rapidly drained into Britain, while its prosperous weavers and artisans were coerced “like so many slaves” by their new masters, and its markets flooded with British products. A proportion of the loot of Bengal went directly into Clive’s pocket. He returned to Britain with a personal fortune – then valued at £234,000 – that made him the richest self-made man in Europe. After the Battle of Plassey in 1757, a victory that owed more to treachery, forged contracts, bankers and bribes than military prowess, he transferred to the EIC treasury no less than £2.5m seized from the defeated rulers of Bengal – in today’s currency, around £23m for Clive and £250m for the company.

William Dalrymple, “The East India Company: The original corporate raiders”, Guardian, 2015-03-04.

January 15, 2022

The futility of “ethical” divestment agitation

In C2C Journal, William McNally explains why activists are demanding that university investments be moved away from fossil fuel companies in favour of “green” investment, and why it won’t work the way they expect:

A recent press release announced that 100 faculty and other staff at three Ontario postsecondary institutions have petitioned the University Pension Plan (UPP) to divest from the fossil fuel sector. The UPP manages the pension funds for over 30,000 employees at the University of Toronto, Queen’s and Guelph. The press release was issued by Shift Action, an organization that helps activist pension members agitate for divestment from what it calls “high-carbon, high-risk fossil fuel investments” such as oil producers and pipeline companies, and shift investments to a “decarbonized” portfolio focused on climate solutions.

I highlighted the UPP petition to draw attention to its activist source, but it is not unique, as it reflects a broader trend of politically driven or, as proponents prefer, “ethical” investing. The motivating claim for divestment in the Shift press release is that we are experiencing a “worsening climate crisis”. That too is a common sentiment nowadays. Because it is a crisis, we have a moral duty to mitigate the threat. The underlying reasoning is that divestment will starve fossil fuel companies of capital and less capital means less production which, in turn, means less CO2 emitted and ultimately slower climate change.

All campaigns of this sort trigger some immediate questions, such as, why choose a strategy as indirect as divestment? Why not reduce fossil fuel use in one’s own backyard, in this case the universities? Looking more broadly, Shift’s argument is more wishful thinking than sound economic analysis. Investors should feel free to hold any portfolio they want, but they should do so without illusions. In particular, they shouldn’t expect divestment to influence climate change by starving oil and natural gas companies of capital.

The first thing wrong is the underlying motivation: there is no climate crisis. As well-known author Bjorn Lomborg states in his most recent book, False Alarm: How Climate Change Panic Costs Us Trillions, Hurts the Poor, and Fails to Fix the Planet: “Climate change is real, but it’s not the apocalyptic threat that we’ve been told it is.” One of the clearest ways to see this is through climate economics. Scenarios set out by the Intergovernmental Panel on Climate Change (IPCC) forecast that over the next 80 years worldwide GDP per capita will likely increase to 450 percent of today’s level.

Lomborg estimates that climate damages will reduce this anticipated increase to 434 percent. Climate change is a problem. Accepting all of the assumptions that went into this modelling, climate change is likely to leave us somewhat less well off than we otherwise would be, by modestly slowing humanity’s overall progress. But judging by these figures, it is not a crisis.

H/T to Robert at SDA for the link.

August 23, 2021

QotD: Leaving money in the hands of individuals

People do things with that money. And even if all they do is buy stuff (thereby allowing someone else to accumulate wealth) or invest it, that money gets aggregated and finds things to do, as it were. Wealth goes to work on things that seem interesting, might be interesting, or are otherwise likely to make money for the individuals who hold the wealth.

Individuals have money to start new businesses that would never have existed if they’d paid that money in taxes. Or they “invest” in free time and a really nice garden, which in turn lifts the spirits of people who invent something because they feel better than they would otherwise.

The left insists that if they leave money in individual hands, it will just be “wasted”. (Because, you know, no money spent on a vast apparatus, most of it a jobs program for useless paper pushers or power-hungry martinets is ever wasted.)

How do they know? Have they tried leaving enough money in the hands of those who earn it to make a difference?

Not in the twentieth century. Though we can infer from the fact that the most sclerotic, dying countries are the highest taxed ones, that perhaps what government considers “best” and what we consider “best” are not the same.

Not just taxes, but regulations too weigh heavily on possibilities. Sure, the left sees “lands saved” (or created. oop) when say, regulations curtail oil drilling. But what I see is energy taking up an excessive amount of every family’s money, wealth that would otherwise be freed for other investments, for starting businesses, even “just” for fun.

The problem we have is that leftists lack utterly in imagination. They see the “pristine” plots of land, or the things government does with our money and they find it good.

But they’re mind’s-eye blind. They can’t see the wealth that has been consumed for almost 100 years now say on the war on poverty to create chronic poverty having instead been used by individuals to create, to invest, to build, so that, in that parallel world in which money stayed in individual hands, we now have interplanetary travel, colonies all over the solar system, and squid farms on Mars that feed all of humanity.

Their lack of vision, their killing of possibilities without the slightest thought to them: That is a tragedy.

Sara Hoyt, “The Tragedy of the Squid Farms on Mars”, Libertarian Enterprise, 2018-12-05.