At the start of the twentieth century, Argentina was one of the wealthiest countries in the world. The capital, Buenos Aires, was known as “the Paris of South America”.

A lot can happen in a hundred years.

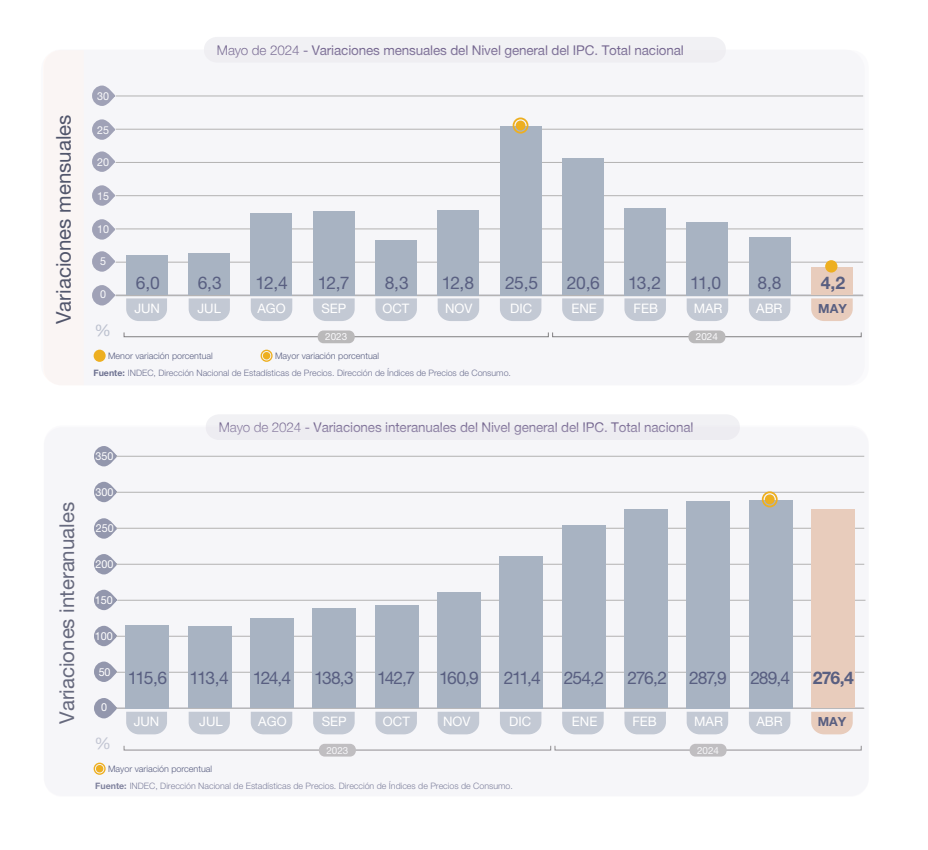

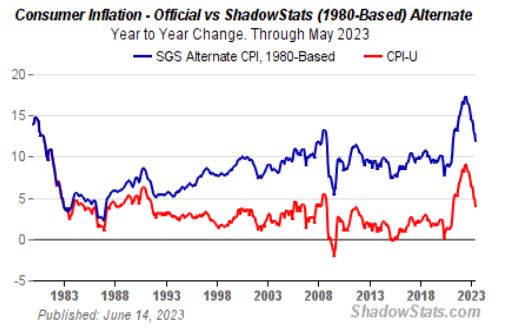

Argentina today is in grave crisis. It has defaulted on its sovereign debt three times since 2001, and a few months ago, it faced an annualized inflation rate of over 200 percent — one of the highest in the world.

Why? What happened?

Argentina’s new president says it’s simple: socialism.

When Javier Milei took office in December 2023, he became the world’s first libertarian head of state. During his campaign, he made his views clear: “Let it all blow up, let the economy blow up, and take this entire garbage political caste down with it”. In case the chainsaw he wielded on the campaign trail left any question about his intentions, during his victory speech last year, he reiterated his vision: “Argentina’s situation is critical. The changes our country needs are drastic. There is no room for gradualism, no room for lukewarm measures.”

There is nothing gradual about what Milei is now doing.

He’s eliminating government ministries and services, cutting regulations, privatizing state-run companies, and purposely creating a recession to curb the out-of-control inflation.

This is why people voted for him: change. They saw someone who could shake things up in a way that could turn out to be lifesaving for the country — even if it meant short-term economic pain.

But will it work? Not all Argentines think so. And not everyone is willing or able to wait for things to improve. In April, with food prices rising and poverty up 10 percent, tens of thousands of Argentines took to the streets to protest Milei’s aggressive austerity measures.

Milei is a strange and idiosyncratic creature. There are the obvious things: He says he doesn’t comb his hair (and he doesn’t appear to). He has four cloned mastiffs that he refers to as his “four-legged children“, and which he’s named for his favorite free-market economists. He was raised Catholic, but studies the Torah. (He even quoted a Midrash during our conversation.) He used to play in a Rolling Stones cover band. And he has been known since grade school in the ’80s as El Loco, on account of his animated outbursts, which would later bring him stardom as a TV, radio, and social media celebrity.

But that’s all the superficial stuff. What really makes Milei unusual is that he is the ultimate skunk at the garden party. In a world of liberals and conservatives, he doesn’t represent either side. He is ultra-liberal on economics, but right-wing and populist on rhetoric. He is anti-abortion, but favors the legalization of prostitution. He wants to deregulate the gun market and legalize the organ trade.

He calls himself an anarcho-capitalist, which basically means he believes the state, as he told me, is “a violent organization that lives from a coercive source which is taxes”. Essentially, he’s a head of state who really doesn’t believe in states. Or at least, not theoretically.

In January, Milei showed up at Davos, the Alpine mountain resort that hosts the annual World Economic Forum. This is traditionally a place where people who all think the same way go to drink champagne and tell each other how smart they are. Milei arrived, flying commercial, and blew up that comfortable consensus: “Today, I’m here to tell you that the Western world is in danger. And it is in danger because those who are supposed to have defended the values of the West are co-opted by a vision of the world that inexorably leads to socialism and thereby to poverty.”

All of this is why I was eager to talk to Milei and put some of these questions to him: How long will it take for things to improve in Argentina? Why does he believe the Western world is in danger? What’s the difference between social justice and socialism? Can the free market really solve all of our civic problems? And how does he feel about being the skunk at the garden party? (Spoiler: He loves it.)

And despite having called journalists “extortionists”, “liars”, “imbeciles”, “freeloaders”, and “donkeys”, for some reason, he agreed to sit down with me.