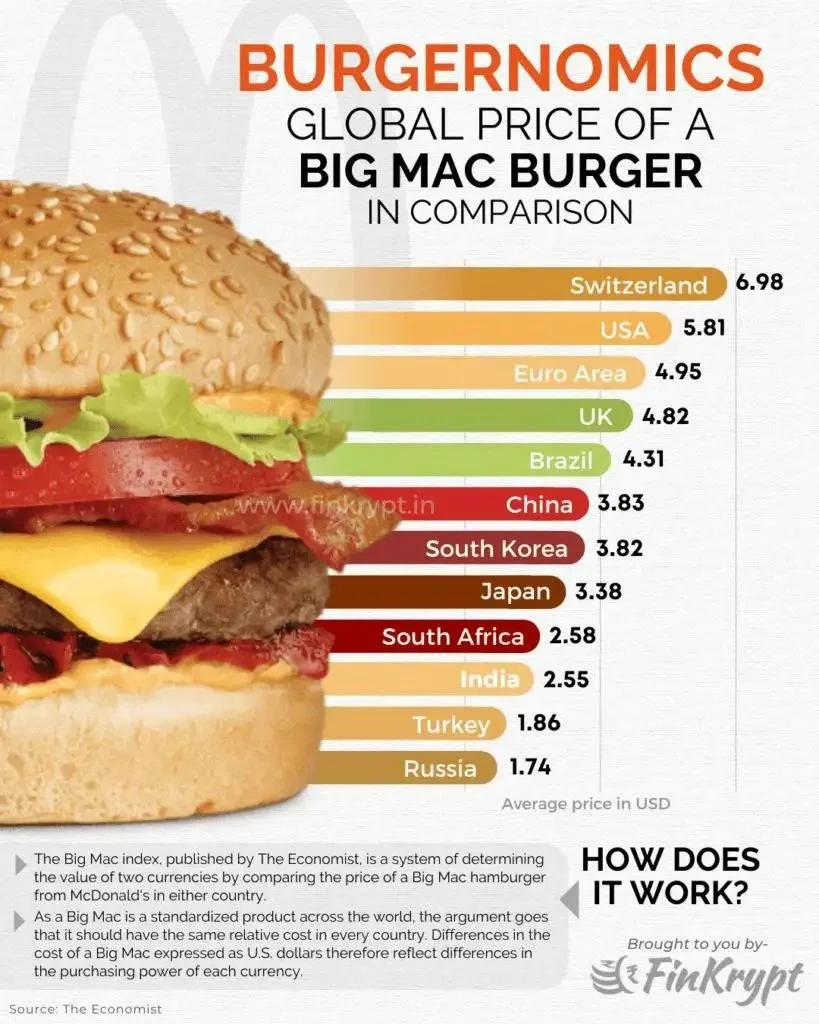

I started reading The Economist when I was in college in the early 1980s. I subscribed after I left college, no longer having access to the school library’s copies, and I continued my subscription for about 20 years. Eventually, I gave up on The Economist as their editorial stance shifted further and further leftward. One of the things they ran regularly was their “Big Mac Index” which compared prices of McDonalds’ Big Mac hamburgers across a range of countries to show the Purchasing Power Parity of the respective countries’ currency against the US dollar. I thought it was a neat way to use readily available data in a form that most consumers would be familiar with to illustrate a wider economic fact. But, as Tim Worstall points out here, the index isn’t actually measuring what it claims to be measuring at all:

Purchasing Power Parity (PPP) constitutes a foundational concept within mainstream international economics, asserting that, over the long term, real exchange rates will naturally adjust to equalize the purchasing power of currencies across nations. This suggests that the cost of an identical basket of goods should, in principle, be uniform globally once currency exchange rates are applied. This notion is frequently popularized through informal measures such as the Big Mac Index. PPP is conceptualized as a specific application of the Law of One Price (LOOP), which posits that, when abstracting from transactional frictions like transportation costs, tariffs, and taxes, any particular commodity traded or purchased should sell for a similar price regardless of its geographical location.

Aaaand, no. The Law of One Price says that a *traded* commodity should be at the same price everywhere, absent transport costs, tariffs and all the rest. Anything that’s not traded this will not be true of. For example, to use an example provided to us:

For instance, if a Starbucks coffee is considerably more affordable in Tokyo than in Manhattan, Purchasing Power Parity (PPP) would indicate an undervalued Yen.

No, Starbucks coffee is not a tradeable item. Coffee beans are globally traded, yes, and coffee beans are the same price the world over — given transport costs, tariffs and so on. But the coffee bean is pennies on the dollar of a Starbucks coffee.

The use of the Big Mac in The Economist‘s popular version of PPP actually runs entirely the other way around. The note is that a Big Mac is made the same way around the world. But it’s always made of *local* ingredients, not internationally traded ones. Therefore we are not measuring whether tradeable goods are the same price in different places at all — we’re measuring what local goods cost in different places.

Comparative advantage, whereby nations specialize in their most efficient productions for reciprocal benefit, is a myth. Absolute advantage reigns supreme.

Then there’s that as well. Which is to misunderstand comparative advantage as well. The insight is not about whether Britain makes cloth better than Portugal and then the same again with wine in reverse. Which is indeed absolute advantage. It’s about whether Britain makes cloth better than Britain makes wine, whether Portugal makes wine better than it does cloth. Each should do what they are *least bad at* and then share the increased production making both richer.

It’s also, once we move away from Ricardo, nothing to do with countries either. It’s something that applies to each and every individual. We should all do what we’re least bad at then swap the production. This does produce an interesting result for given how good, *ahem*, my economic writing is take a guess at how skilled I am at other ways of making a living? Quite.

So, you know, not getting PPP, LOOP nor comparative advantage — but still ending up calling for world government and that proper democratic control of the economy. Ah well, at least it’s fashionable even if incorrect.