I used to love Elon like everyone else. I still think that having four or five billionaires in a space race against each other is finally the world I thought I was going to get growing up reading Heinlein. The Tesla Model S was probably one of the most revolutionary cars of the last 50 years. But he lost me when he committed outright fraud in the Solar City – Tesla deal and since then have only become more skeptical about he and Tesla.

Elon Musk at the 2015 Tesla Motors annual meeting.

Photo by Steve Jurvetson via Wikimedia Commons.I sort of laugh when folks tell me that really smart successful rich people believe in Tesla. You mean like James Murdoch, on the board of Tesla and who also was lost his entire investment in Theranos? Or like Larry Ellison, an adviser and fan of Elizabeth Holmes who invested $1 billion in Tesla just 6 months ago and has already lost 40% of it? The window on this is probably closing, but over the last 10 years if you wanted to get Silicon Valley investors to throw a lot of money at you, find a traditional bricks and mortar business and devise a story in which you take that industry and convert its economics to that of the networked software world (see: Uber, WeWork, Tesla, and even Theranos in some of its strategic pivots).

Or how about true millennials and Elon Musk? Name a wealthy millennial supporter of Elon Musk and Tesla and I can bet you any amount of money they have not looked at Tesla’s balance sheet or cash flow or the details of its global demand trends. They have not thought about its dealership strategy or manufacturing strategy and the cash flow implications of these. They just like what Elon says. It sounds big and visionary. They buy into Elon’s formulation that he is saving the environment and everyone opposed to him is in a cabal with big oil (ignoring the fact that Elon routinely uses his Gulfstream VI to commute distances less than 60 miles). So saying that rich millenials adore Elon is effectively saying that they want to be associated with the same things Elon says he is for — the environment and space travel et al.

Elon Musk is Ferdinand DeLesseps. He is PT Barnum. He is Elizabeth Holmes. He is the pied piper. He is fabulous at spinning visions and making them sound science-y. But he is not Tony Stark. There is a phenomenon with Elon Musk that everyone thinks he is brilliant until they hear him speak about something about which they have domain knowledge, and then they realize he is full of sh*t. For example, no one who knows anything about transportation or physics or basic engineering has thought his Boring Company and Hyperloop make any sense at all. His ideas would have been great cover stories for Popular Mechanics in the 1970’s, wowing 13-year-old boys like me with pictures of mile-long cargo blimps and flying RV’s. He is like a Marvel movie that spouts science that is just believable-enough sounding that it moves the plot along but does not stand up to any scrutiny.

All of this would be harmless if he was not running a public company. I don’t really care about the rich folks who were duped by Elizabeth Holmes, but hundreds of thousands of small millenial investors who have totally bought into the Elon hype are literally putting their last dollar into Tesla, and sometimes borrowing more. Tesla shorts often laugh at these folks on Twitter, calling them “bagholders,” but it is a tragedy. Unless Tesla finds a sugar daddy sucker, and the odds of that are getting longer, I think it is going to end badly for many of these investors.

As a disclosure, I have been short Tesla via puts for a while now. It you really want to understand Elon, the best book I can recommend is The Path Between The Seas about the building of the Panama Canal. First, it is a great book you should read no matter what. And second, Ferdinand DeLesseps is the best analog I can find for Musk.

Warren Meyer, “People Who Express Opinions Outside of their Domain Seldom Have Really Looked into it Much”, Coyote Blog, 2019-05-28.

July 3, 2019

QotD: Elon Musk as a modern-day Ferdinand DeLesseps

June 21, 2019

Making America Great Again | Between 2 Wars | 1927 Part 1 of 2

TimeGhost History

Published on 20 Jun 2019In 1927 the US is finally back to its pre-WWI economic greatness, at least measured by the stock market. But all is not well with the finances in the land of the free and home of the brave.

Join us on Patreon: https://www.patreon.com/TimeGhostHistory

Hosted by: Indy Neidell

Written by: Francis van Berkel and Spartacus Olsson

Research by: Francis van Berkel

Directed and Produced by: Spartacus Olsson and Astrid Deinhard

Executive Producers: Bodo Rittenauer, Astrid Deinhard, Indy Neidell, Spartacus Olsson

Creative Producer: Joram Appel

Post Production Director: Wieke Kapteijns

Edited by: Wieke KapteijnsArchive by Reuters/Screenocean http://www.screenocean.com

A TimeGhost chronological documentary produced by OnLion Entertainment GmbH

From the comments:

TimeGhost History

1 day ago (edited)

So… before you all go and get your panties in a bunch about the title. 1. This video is literally abut the effort to make America great again in the 1920s. 2. Although Donald Trump appropriated that expression in 2016, it has been used by two Presidents before him; Ronald Reagan and Bill Clinton. 3. It has even been used in other political contexts both liberal and conservative as early as in the 1940s. So, as a historical reference to US history, not a political value comment, it is highly relevant to this episode. On that note, our heartfelt thanks to our TimeGhost Army that keeps the wheels attached to the TimeGhost vehicle and keeps us rolling forward into the past. If you’re not already a member, you can join here: https://www.patreon.com/TimeGhostHistory or here: https://timeghost.tv

April 9, 2019

Blue’s Dumb History Tales

Overly Sarcastic Productions

Published on 8 Mar 2019Please check out That Works for the best blacksmithing on YouTube: https://goo.gl/vXsuFt

What do you get when you cross a month that has 5 Fridays with a historian who can’t do math? This nonsense, apparently.

PATREON: https://www.patreon.com/OSP

March 22, 2019

Understanding the Great Depression

Marginal Revolution University

Published on 23 May 2017In this video, we examine the causes behind the Great Depression with the help of the aggregate demand-aggregate supply model.

In 1929, the stock market crashed and an air of pessimism swept across America — making bank depositors nervous. What would you do if you thought your money might not be safe with the bank? You’d probably want it back in your own hands. What happened next? A run on the banks.

Along with the Stock Market Crash of 1929, it’s one of the iconic moments of the early days of Great Depression. However, the Great Depression was an incredibly complex downturn in which the economy experienced a series of aggregate demand shocks. By the end of this video, you’ll walk away with a better understanding of the many factors behind the Great Depression and how to apply the AD-AS model to a real-world scenario.

January 27, 2019

Some reasons to be bearish on Tesla’s future

At Coyote Blog, Warren Meyer climbs back onto one of his favourite hobby horses:

Yes, I am like an addict on Tesla but I find the company absolutely fascinating. Books and HBS case studies will be written on this saga some day (a couple are being written right now but seem to be headed for Musk hagiography rather than a real accounting ala business classics like Barbarians at the Gate or Bad Blood).

I still stand by my past thoughts here, where I predicted in advance of results that 3Q2018 was probably going to be Tesla’s high water mark, and explained the reasons why. I won’t go into them all. There are more than one. But I do want to give an update on one of them, which is the growth and investment story.

First, I want to explain that I have nothing against electric vehicles. I actually have solar panels on my roof and a deposit down on an EV, though it is months away from being available. What Tesla bulls don’t really understand about the short position on Tesla is that most of us don’t hate on the concept — I respect them for really bootstrapping the mass EV market into existence. If they were valued in the market at five or even ten billion dollars, you would not hear a peep out of me. But they are valued (depending on the day, it is a volatile stock) between $55 to $65 billion.

The difference in valuation is entirely due to the charisma and relentless promotion by the 21st century’s PT Barnum — Elon Musk. I used to get super excited by Musk as well, until two things happened. One, he committed what I consider outright fraud in bailing out friends and family by getting Tesla to buy out SolarCity when SolarCity was days or weeks from falling apart. And two, he started talking about things I know about and I realized he was totally full of sh*t. That is a common reaction from people I read about Musk — “I found him totally spellbinding until he was discussing something I am an expert in, and I then realized he was a fraud.”

Elon Musk spins great technology visions. Like Popular Mechanics magazine covers from the sixties and seventies (e.g. a flying RV! a mile long blimp will change logging!) he spins exciting visions that geeky males in particular resonate with. Long time readers will know I identify as one of this tribe — my most lamented two lost products in the marketplace are Omni Magazine and the Firefly TV series. So I see his appeal, but I have also seen his BS — something I think a lot more people have caught on to after his embarrassing Boring Company tunnel reveal.

December 2, 2018

QotD: There’s investment and then there’s “public investment”

In 2003, the Organisation for Economic Cooperation and Development published a paper on the ‘sources of economic growth in OECD countries’ between 1971 and 1998 and found, to its surprise, that whereas privately funded research and development stimulated economic growth, publicly funded research had no economic impact whatsoever. None. This earthshaking result has never been challenged or debunked. It is so inconvenient to the argument that science needs public funding that it is ignored.

November 30, 2018

England: South Sea Bubble – Lies – Extra History

Extra Credits

Published on 9 May 2015Support us on Patreon! http://bit.ly/EHPatreon

____________No historian is perfect, so it’s important we acknowledge our mistakes where we find them (with the help of our viewers, no less)! After we clear up some discrepancies that emerged during the South Sea Bubble series, we turn to answering some common questions that came up during this series on economic history. In a period where financial masterminds like John Blunt engaged in trickery meant to confuse other people and hide his real activities, it’s no wonder that many viewers had questions about what insider trading is and how Blunt could endlessly inflate stock prices for his unprofitable company. This is a history show, but we do our best to explain! As a bonus, James also reads Robert Knight’s letter to Parliament on the eve of his illegal flight and tells some cool stories about Robert “It was Me” Walpole.

September 27, 2018

Revising the accredited investor rules

Alex Tabarrok summarizes a suggestion from Matt Levine on how to improve the rules for accredited investors:

Matt Levine has an excellent piece on accredited investor rules and his alternative:

- Anyone can also invest in any other dumb investment; you just have to go to the local office of the SEC and get a Certificate of Dumb Investment. (Anyone who sells dumb non-approved investments without requiring this certificate from buyers goes to prison.)

- To get that certificate, you sign a form. The form is one page with a lot of white space. It says in very large letters: “I want to buy a dumb investment. I understand that the person selling it will almost certainly steal all my money and that I would almost certainly be better off just buying index funds, but I want to do this dumb thing, anyway. I agree that I will never, under any circumstances, complain to anyone when this investment inevitably goes wrong. I understand that violating this agreement is a felony.”

- Then you take the form to an SEC employee, who slaps you hard across the face and says “Really???” And if you reply “Yes, really,” then she gives you the certificate.

- Then you bring the certificate to the seller and you can buy whatever dumb thing he is selling.

September 26, 2018

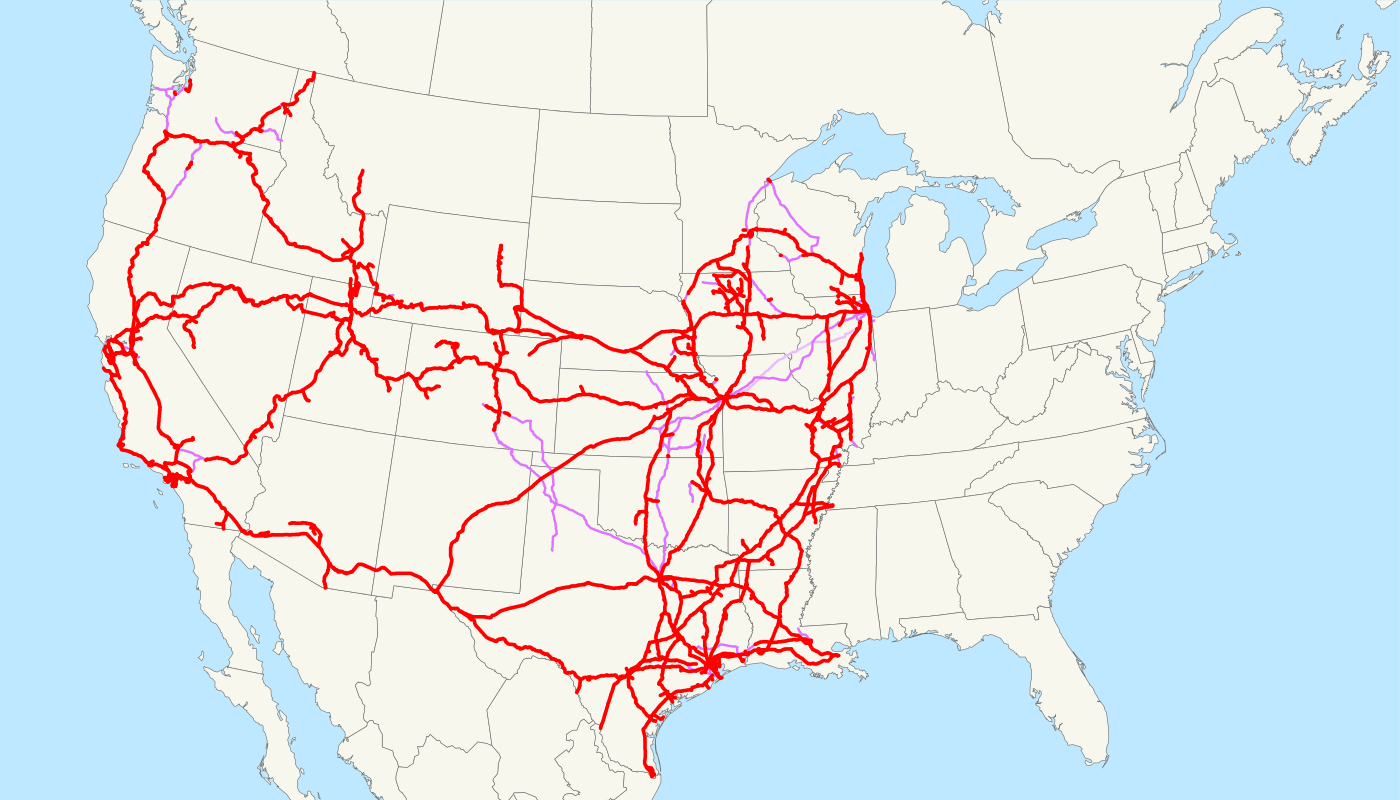

Reforming Union Pacific

Fred Frailey explains why the vast Union Pacific system is due for some serious economic streamlining:

Union Pacific locomotive 5587, a General Electric AC4400CW-CTE (AC44CWCTE)

Photo by Terry Cantrell via Wikimedia Commons.

Union Pacific is the ideal lab rat for Precision Scheduled Railroading, practiced by the late Hunter Harrison on four Class I railroads, with great rewards for shareholders and mixed results for customers. UP, which will begin recasting itself October 1, is ideal for the role because it has too many employees, too many unproductive route miles, and too many expensive toys. Plus, it is less interested in increasing market share than in maximizing freight rates, which makes right-sizing the railroad easier. Let’s start by running the numbers.

Employees. At the peak of the last railroad cycle in 2006, Union Pacific had already been lapped by its western competitor, BNSF Railway, in both cars originated and revenue ton miles. Since then, through 2017, UP’s originations and revenue ton miles both fell 17 percent, while BNSF RTMs actually set a record in 2017. Yet at 44,146 employees last year, UP’s employee count was still 7 percent higher than that of BNSF. To put this another way, for UP’s productivity per employee (revenue ton miles per worker) to equal its competitor’s, it would need to slice the headcount by 16,000. A place to start might be headquarters in Omaha. UP counted 3,678 executives, officials and staff assistants in 2017 versus BNSF’s 1,511.

Barren route miles. Salina, Kan., to Provo, Utah, is becoming a traffic wasteland. That didn’t stop UP from laying welded rail and concrete ties and from covering the almost 1,000 miles with centralized traffic control. Meanwhile, one train a day (plus Amtrak) operates In Missouri between St. Louis and Poplar Bluff, Ark. And the railroad has effectively ceased freight service between Watsonville Junction and San Luis Obispo, Calif., and is close to doing so over the rest of the Coast Line to Los Angeles. All of these routes and perhaps many others you can identify contribute little revenue but buckets of costs, inflating the operating ratio (which is the percentage of revenues eaten up by operating costs). They would constitute Hunter Harrison’s first target.

Map of the Union Pacific Railroad as of 2008, with trackage rights in purple (the special Chicago-Kansas City intermodal trackage rights are lighter).

Image via Wikimedia Commons.[…]

Moreover, there are aspects to PSR as practiced by Hunter Harrison that customers won’t like. At the core of Precision Scheduled Railroading is intense use of assets: Run as many trains every day one direction as you do the other, fill them to maximum designed length and operate them at similar speeds. This isn’t how the commercial world works, and the Hunter Harrison way to make customers ship seven days a week was to discount rates on slow days and slap on surcharges on busy days. This keeps your crews and equipment fleet in motion at all times, and those cars and locomotives not continually used can be retired. Goodbye to growth and increased market share, which is a messy process requiring you to accede to the needs of customers rather than the other way around. But it is efficient.

However, if Union Pacific is serious about serving its customers better and delivering individual cars rather than trains to their destinations on schedule, I have an idea that I guarantee will achieve that result: Base salaried bonuses and stock grants on UP’s success in getting cars to customers on the right day and time and on the right train. UP has scheduled individual cars for decades, but there have never been monetary consequences for achieving those plans. People do follow the money. And when Union Pacific does for customers what it says it will do, calling the process Precision Scheduled Railroading or whatever you wish, I will be leading the applause.

September 21, 2018

QotD: “Let us abandon Capitalism, and go back to Adam Smith”

An old friend of mine, among my bosses in late ’seventies Bangkok — Antoine van Agtmael, genuinely admired and loved — was the genius who invented the expression “emerging markets,” to replace that downer, “developing countries.” (Which in turn had been the euphemism for “backward countries.”) It was by such creative hocus-pocus that attitudes towards “Third World” investment were dramatically changed, in the era of Thatcher and Reagan. A man of indomitably good intentions; charitable, selfless, and a brilliant merchant banker; a little leftish in his social and cultural outlook — I give Antoine’s phrase as an example of the sort of poetry that changes the world. I took pride, once, in editing a book of his astute investment “case studies.”

Thirty-six years have passed, since in my youth and naiveté I was draughting a book of my own on what is still called “development economics.” (I was a business journalist in Asia then, who did a little teaching on the side.) It seemed to me that “free enterprise” should be encouraged; that “government intervention” should be discouraged; but that the aesthetic, moral, and spiritual order in one ancient “developing country” after another was being undermined by the success, as also by the frequent failures, not only of foreign but of domestic investors. This bugged me because, like my father before me (who had worked and taught westernizing subjects in this same Third World), my well-intended efforts on behalf of “progress” were ruining everything they touched; everything I loved.

My attempt to explain this, if only to myself, ended in abject failure to answer my central question: “Why does capitalist success make the world ugly and its people sad?”

Only now do I begin to glimpse an answer; and that part of it could be expressed in the imperative, “Let us abandon Capitalism, and go back to Adam Smith.”

David Warren, “In defence of economic backwardness”, Essays in Idleness, 2016-12-01.

July 12, 2018

Infrastructure has costs as well as benefits

Tim Worstall makes a sensible point that applies (to a greater or lesser extent) to most of these “we’re dropping down the league tables in telecommunications” stories:

The Daily Mail is reacting with horror to the thought that the UK has slipped down the broadband tables. We’re only 35th in the world for average speed now! The correct answer to which is that yes, of course the UK’s broad band speeds are slow, we’re a developed and rich country. Which doesn’t mean that yes we’ll have the latest in shiny infrastructure. Rather, it means that we put in infrastructure some time ago and thus have the infrastructure from some time ago. You know, having infrastructure being one of the things which makes you a rich and developed nation?

Britain has slipped four places in the world broadband speed league, leaving its network lagging well behind the likes of Latvia, Lithuania, Hungary and Romania.

The UK is the sixth largest economy in the world but has dropped to 35th in the rankings after being overtaken by France and even Madagascar, according to the latest analysis.

As other countries rush to install fibre-optic cable networks which are capable of providing superfast download speeds, much of Britain continues to rely on old copper telephone wires to connect homes to the web.

Well, yes, the point being that we had a copper based network which went to pretty much everywhere. Thus we’ve not rushed to put in the fibreoptic because we’ve actually not needed it. Hey, sure, maybe it would be nice. Maybe it’s something we will install everywhere in the future. But we’ve not done it as yet because there’s not been a pressing case for that investment.

You see, our forebears already invested in the copper for us.

As a general rule of thumb, the earlier you invested in your telecommunications network, the slower it will be compared to current technology. At some point, it becomes economical to replace the installed network, but as long as the existing infrastructure is providing a profit, there isn’t the sense of urgency that most of these “the sky is falling” articles imply.

June 29, 2018

QotD: What is a discount rate?

It is not the 20 percent savings you got by buying a new washing machine on Black Friday last year. A discount rate is a way of accounting for the fact that dollars in the future are not quite the same as dollars you have right now.

You know this, don’t you? Imagine I offered to give you a dollar right now, or a dollar a year from now. You don’t have to think hard about that decision, because you know instinctively that the dollar that’s right there, able to be instantly transferred into your sweaty little hand, is much more valuable. It can, in fact, be easily transformed into a dollar a year from now, by the simple expedient of sticking it in a drawer and waiting. It can also, however, be spent before then. It has all the good stuff offered by a dollar later, plus some option value.

Even if you’re sure you don’t want to spend it in the next year, however, a dollar later is not as good as a dollar now, because it’s riskier. That dollar I’m holding now can be taken now, and then you will definitely have it. If you’re counting on getting a dollar from me a year from now, well, maybe I’ll die, or forget, or go bankrupt.

The point is that if you’re valuing assets, and some of your assets are dollars you actually have, and others are dollars that someone has promised to give to you at some point in the future, you should value the dollars you have in your possession more highly than dollars you’re supposed to get later.

The rule for establishing an exchange rate between future dollars and current ones is known as the “discount rate.” Basically, it’s a steady annual percentage by which you lower the value of dollars you get in future years.

All you need to remember is two things: the longer you have to wait to get paid, the less that promise is worth to you today. And the higher the discount rate you apply, the lower you’re valuing that future dollar.

Megan McArdle, “Public Pensions Are Being Overly Optimistic”, Bloomberg View, 2016-09-21.

April 14, 2018

The Solow Model and the Steady State

Marginal Revolution University

Published on 12 Apr 2016Remember our simplified Solow model? One end of it is input, and on the other end, we get output.

What do we do with that output?

Either we can consume it, or we can save it. This saved output can then be re-invested as physical capital, which grows the total capital stock of the economy.

There’s a problem with that, though: physical capital rusts.

Think about it. Yes, new roads can be nice and smooth, but then they get rough, as more cars travel over them. Before you know it, there are potholes that make your car jiggle each time you pass. Another example: remember the farmer from our last video? Well, unless he’s got some amazing maintenance powers, in the end, his tractors will break down.

Like we said: capital rusts. More formally, it depreciates.

And if it depreciates, then you have two choices. You either repair existing capital (i.e. road re-paving), or you just replace old capital with new. For example, you may buy a new tractor.

You pay for these repairs and replacements with an even greater investment of capital.

We call the point where investment = depreciation the steady state level of capital.

At the steady state level, there is zero economic growth. There’s just enough new capital to offset depreciation, meaning we get no additions to the overall capital stock.

A further examination of the steady state can help explain the growth tracks of Germany and Japan at the close of World War II.

In the beginning, their first few units of capital were extremely productive, creating massive output, and therefore, equally high amounts available to be saved and re-invested. As time passed, the growing capital stock created less and less output, as per the logic of diminishing returns.

Now, if economic growth really were just a function of capital, then the losers of World War II ought to have stopped growing once their capital levels returned to steady state.

But no, although their growth did slow, it didn’t stop. Why is this the case?

Remember, capital isn’t the only variable that affects growth. Recall that there are still other variables to tinker with. And in the next video, we’ll show two of those variables: education (e) and labor (L).

Together, they make up our next topic: human capital.

April 4, 2018

DicKtionary – I is for Investment – Gregor MacGregor

TimeGhost

Published on 3 Apr 2018I for investment, for financial success,

Or for a failure, cause it’s hard to guess,

But if there’s one man who could make you a beggar,

It’s today’s star, Gregor MacGregor.Join us on Patreon: https://www.patreon.com/TimeGhostHistory

Written and Hosted by: Indy Neidell

Based on a concept by Astrid Deinhard and Indy Neidell

Produced by: Spartacus Olsson

Executive Producers: Bodo Rittenauer, Astrid Deinhard, Indy Neidell, Spartacus Olsson

Camera by: Ryan Tebo

Edited by: Bastian BeißwengerA TimeGhost format produced by OnLion Entertainment GmbH

February 15, 2018

DicKtionary – D is for Dollars – Hetty Green

TimeGhost

Published on 14 Feb 2018D is for dollars, 100 to the penny,

Some have but few, others have many,

Some hoard them too – the frugal and mean,

And none was more frugal than one Hetty Green.Hosted and Written by: Indy Neidell

Based on a concept by Astrid Deinhard and Indy Neidell

Produced by: Spartacus Olsson

Executive Producers: Bodo Rittenauer, Astrid Deinhard, Indy Neidell, Spartacus Olsson

Edited by: Bastian BeißwengerA TimeGhost format produced by OnLion Entertainment GmbH