Janice Fiamengo debunks a common “just so” story about women only gaining the right to hold a credit card in the 1970s:

A few years ago, I started hearing that women, before feminism, couldn’t have their own credit cards. Or they couldn’t get one without a man’s signature. Or married women couldn’t have one in their own name. Divorced women, apparently, couldn’t get credit at all. Men conspired to keep women powerless and dependent.

THANK THE GODDESS FOR FEMINISM!

Just last June, on the podcast Diary of a CEO (in an episode viewed by nearly two million people), three feminists debating feminism agreed that, in the words of one of the panelists, “None of us could get a credit card a few decades ago … We couldn’t have anything …” (see 1:50:37).

Before correcting herself, in fact, the panelist had started to say, “None of us could get a credit card a couple of decades ago …”

The statement struck me with the full force of the ludicrous. I started school in 1970. My teachers were nearly all women, at least half of them unmarried. They certainly seemed to live full, normal lives in obeisance to no man. They were paid a salary; they had bank accounts; they owned cars; they bought things and went on vacations.

My mother had worked in an insurance office for years both before and after she married my father in 1956. She had purchased appliances and paid her own rent, helped my father buy his first commercial fishing boat, and handled all the household expenses when my dad was away fishing for months every summer.

My friends’ mothers were similarly active and self-determining. Were all these women actually hobbled by the patriarchy, cut off from the economy?

Received knowledge would have us believe so. Last year, The Globe and Mail published a paid advertisement for Women’s History Month titled “50 Years Ago: Women Got the Right to Have Credit Cards”. Written by a financial services company seeking to drum up business, the article repeated the popular story that women in North America could not get their own credit cards until 1974.

Credit cards were one of the growth areas for banks and other financial service companies in the 1960s and 70s … from something only relatively wealthy travellers and business executives used, they expanded to become widely used by ordinary consumers for all kinds of purchases. Consumers benefitted from access to useful financial tools, while banks enjoyed the profits from the widespread use of credit cards. So where did the idea that they were male-only come from?

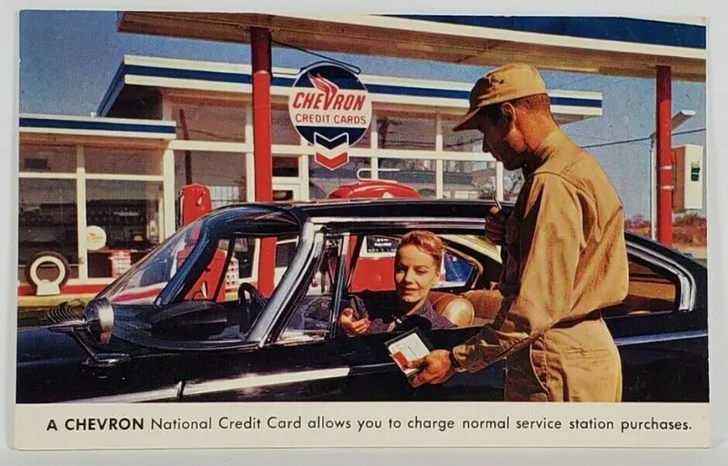

The reality is that from the 1950s on, credit cards were a new invention being aggressively marketed to both men and women. Advertising from the era shows how keen credit card companies were to target female customers, how eager to tap into women’s spending power.

Originally introduced as a convenience for travelers on business, credit cards began to expand their purview in the late 1950s. Bank Americard (later Visa) became the first consumer credit card in 1958. A network of banks formed the Interbank Card Association, originally named Master Charge (later Mastercard), in 1966.

Yet we are somehow to believe that half the population was deliberately excluded from this new consumer venture for no other reason than that they were female?

“It wasn’t until 1974 that women were allowed to open a credit card under their own name,” the Globe article states emphatically. “Before 1974, if women wanted to open a credit card, they would be asked a bunch of intrusive questions, like if they were married or whether they planned to have children. If a woman was married, she could (hopefully) get a credit card with her husband. But single, divorced, or widowed women weren’t allowed to get a credit card of their own — they had to have a man cosign for the credit application.”

The explanation is dramatic and incoherent, undoing its own logic from the beginning. It backtracks to allege that women were in fact “allowed” to have a credit card so long as they answered “a bunch of intrusive questions” or found a co-signer. Even this lesser claim is false, but it is rather different from the prior assertion about women “not having the right” to a card.

At a time when many married women either did not work outside the home or worked only part-time and on a temporary basis, there would have been nothing unreasonable about a woman’s husband co-signing her credit card application. Many married women were happy to purchase what they wanted on the assurance that their husbands would pay the bill when it came in, and credit card issuers saw joint accounts as a way of ensuring payment.

Update, 4 October: Welcome, Instapundit readers! Please have a look around at some of my other posts you may find of interest. I send out a daily summary of posts here through my Substack – https://substack.com/@nicholasrusson that you can subscribe to if you’d like to be informed of new posts in the future.