Janice Fiamengo debunks a common “just so” story about women only gaining the right to hold a credit card in the 1970s:

A few years ago, I started hearing that women, before feminism, couldn’t have their own credit cards. Or they couldn’t get one without a man’s signature. Or married women couldn’t have one in their own name. Divorced women, apparently, couldn’t get credit at all. Men conspired to keep women powerless and dependent.

THANK THE GODDESS FOR FEMINISM!

Just last June, on the podcast Diary of a CEO (in an episode viewed by nearly two million people), three feminists debating feminism agreed that, in the words of one of the panelists, “None of us could get a credit card a few decades ago … We couldn’t have anything …” (see 1:50:37).

Before correcting herself, in fact, the panelist had started to say, “None of us could get a credit card a couple of decades ago …”

The statement struck me with the full force of the ludicrous. I started school in 1970. My teachers were nearly all women, at least half of them unmarried. They certainly seemed to live full, normal lives in obeisance to no man. They were paid a salary; they had bank accounts; they owned cars; they bought things and went on vacations.

My mother had worked in an insurance office for years both before and after she married my father in 1956. She had purchased appliances and paid her own rent, helped my father buy his first commercial fishing boat, and handled all the household expenses when my dad was away fishing for months every summer.

My friends’ mothers were similarly active and self-determining. Were all these women actually hobbled by the patriarchy, cut off from the economy?

Received knowledge would have us believe so. Last year, The Globe and Mail published a paid advertisement for Women’s History Month titled “50 Years Ago: Women Got the Right to Have Credit Cards”. Written by a financial services company seeking to drum up business, the article repeated the popular story that women in North America could not get their own credit cards until 1974.

Credit cards were one of the growth areas for banks and other financial service companies in the 1960s and 70s … from something only relatively wealthy travellers and business executives used, they expanded to become widely used by ordinary consumers for all kinds of purchases. Consumers benefitted from access to useful financial tools, while banks enjoyed the profits from the widespread use of credit cards. So where did the idea that they were male-only come from?

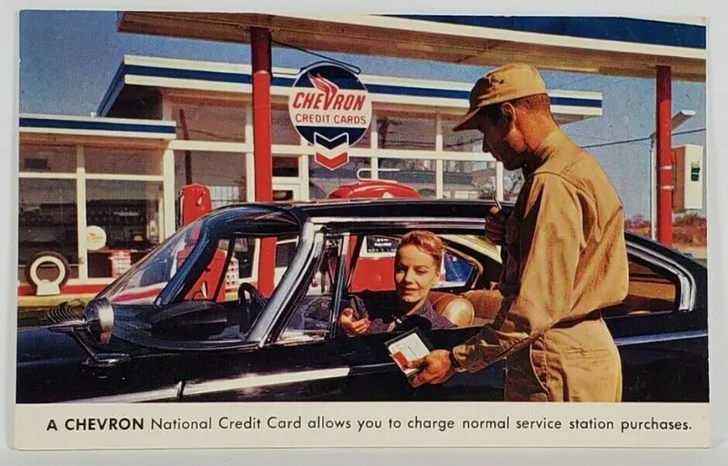

The reality is that from the 1950s on, credit cards were a new invention being aggressively marketed to both men and women. Advertising from the era shows how keen credit card companies were to target female customers, how eager to tap into women’s spending power.

Originally introduced as a convenience for travelers on business, credit cards began to expand their purview in the late 1950s. Bank Americard (later Visa) became the first consumer credit card in 1958. A network of banks formed the Interbank Card Association, originally named Master Charge (later Mastercard), in 1966.

Yet we are somehow to believe that half the population was deliberately excluded from this new consumer venture for no other reason than that they were female?

“It wasn’t until 1974 that women were allowed to open a credit card under their own name,” the Globe article states emphatically. “Before 1974, if women wanted to open a credit card, they would be asked a bunch of intrusive questions, like if they were married or whether they planned to have children. If a woman was married, she could (hopefully) get a credit card with her husband. But single, divorced, or widowed women weren’t allowed to get a credit card of their own — they had to have a man cosign for the credit application.”

The explanation is dramatic and incoherent, undoing its own logic from the beginning. It backtracks to allege that women were in fact “allowed” to have a credit card so long as they answered “a bunch of intrusive questions” or found a co-signer. Even this lesser claim is false, but it is rather different from the prior assertion about women “not having the right” to a card.

At a time when many married women either did not work outside the home or worked only part-time and on a temporary basis, there would have been nothing unreasonable about a woman’s husband co-signing her credit card application. Many married women were happy to purchase what they wanted on the assurance that their husbands would pay the bill when it came in, and credit card issuers saw joint accounts as a way of ensuring payment.

Update, 4 October: Welcome, Instapundit readers! Please have a look around at some of my other posts you may find of interest. I send out a daily summary of posts here through my Substack – https://substack.com/@nicholasrusson that you can subscribe to if you’d like to be informed of new posts in the future.

[…] SO TIRED OF THESE: Women and credit card access … another “just so” story. […]

Pingback by Instapundit » Blog Archive » SO TIRED OF THESE: Women and credit card access … another “just so” story. — October 4, 2025 @ 04:00

Makes sense. You don’t want to have the half of the population that LOVES SHOPPING to run up a credit card and have to pay you lots of interest. Because banks are much more concerned with keeping the womenfolk in their place than with making profits.

Comment by Michael Hutchison — October 4, 2025 @ 04:29

the writer of this article was obviously not alive in the 1970s or not old enough to have experienced this. I was. It was true. I was in grad school. had some income, job. I was told I could not have a credit card at a dept store (Scarboroughs, Austin Tx.) without the signature of a husband or father. This article is garbage.

Comment by susan harms — October 4, 2025 @ 05:43

Oddly, women in countless small towns (presumably the most backward of the backward places) were able to write a counter check for their purchases without even showing ID!

Comment by Not That Donald — October 4, 2025 @ 07:42

Um. Read the article you’re quoting. It says, in so many words, that married women generally had to have a husband co-sign a card application prior to ECOA. This exactly matches my wife’s and my own experience of credit in the late 60s and early 70s. The fact that my wife earned as much as I did, and had a job of the same (poor) stability, was irrelevant. She could not get a card in her name only. We tried. No bank would accept the application without a co-signer, me, her husband. I could (and did) get a card without her signature in my name only.

Banks were indeed suspicious that single women would marry and lose their job (that was my employer’s stated policy in the 50s). Women were in general considered a poorer credit risk for cards in their name only because of such policies.

As the piece says, women “often” could not get a card independently before the ECOA. “Usually” would be more correct. The ECOA told the card issuers that they had to have ONE set of standards for credit approval, for both sexes.

The Smithsonian article accurately reflects the reality of the time. It does not claim that cards were ‘male-only’ – that’s your interpretation. It DOES say that getting credit (of any kind) was difficult for single women. Not impossible, just very hard. And that was absolutely the situation.

Comment by doc — October 4, 2025 @ 08:01

My parents had a small business where my father did the shop work and my mother handled the business/book keeping side. One of the things that I recall about the day to day aspects of their work was that extending credit or not extending credit was often discussed. My father tended to be somewhat too lenient so my mother had to keep him on a short leash. The biggest fly in their business ointment seemed to be single women. The problem was that they would often build up a mountain of debt, marry (there-by changing their name), and then disappear. Tracking them down was often impossible, leading to my parents having to eat the loss. Their often choosing to not sell to single women had nothing to do with anything other than basic economics.

Comment by Oran Woody — October 4, 2025 @ 09:14

In 1974, 4% of men had a bank credit card.

Comment by Tmitsss — October 4, 2025 @ 09:43

My guess is that that law passed in ’74 simply codified into law the idea that women could not be treated differently than men when applying for a credit card. It was likely a result of the growing popularity of credit cards (and maybe was a political sop to the recently-minted Feminist Movement as a consolation prize for the failure of the ERA).

A woman who could prove she was creditworthy in her own right was, I suspect, rarely turned down for a card.

Comment by jbspry — October 4, 2025 @ 10:26

Yes yes, I know feminism has been around since the mid-19th century.

“Resurgent” or “recently-militantized” would be better than “recently-minted”.

Now go make me a sandwich.

Comment by jbspry — October 4, 2025 @ 10:30

Credit cards used to demand that you actually had, you know, credit before you could get a card. As a college student in the early 1980s, I could not get a card. And none of my fellow students had a card, male or female. Students couldn’t get one, not even with a co-signer. When I graduated and got my first full-time job, I finally was able to get a card. It had a rate of 27% and a credit limit of $300. I needed to build up credit before I could get anything else. Credit card issuers did not give the things out like candy, the way they do now.

Comment by Alabama Slamma — October 4, 2025 @ 11:01

I got my first credit card sent to me unsolicited in mid 1960s. I was female, in college, and it was a Sunoco gas card. IIRC cards were sent unsolicited in those days. In the early 1970s, by then married, my husband and I had a bit of a fuss getting a credit card as we had been out of the country for several years and did our finances on a cash basis so I guess our credit score didn’t have much to go on. Shamed them into issuing us one so we could rent the Uhaul to move with 😉

Two spinster great aunts bought a house together in their hometown in MA waaay (1940s?) before feminism made it an issue. So there were other stories out there. And yes my husband had to cosign for our college aged kid when he bought a used truck, because there are rules in how lenders guard their investments.

Comment by JAL — October 4, 2025 @ 11:13

Oh, for the Love of Life Orchestra. I just read the recently-published novel “The Art of Vanishing” by Morgan Pager (shouldn’t have bothered; it was a waste of time), which among other historical absurdities presents a woman in France in the interwar period posing for Modigliani … in exchange for paints and canvas. Because apparently men were so determined to keep women from making art that they couldn’t obtain paints and canvas except through barter with male artists. These Handmaid’s Tale fantasies are getting out of hand.

Comment by werewife — October 4, 2025 @ 20:25

In 1967, a year out of the army, a year into a marriage, a year into a job paying an above average salary, a year of payments (at 12% interest) on a 3 year old used car, I was turned down (after getting a mailed invitation to apply) for an Esso credit card. I am male.

Nobody passed out credit to unknowns, except at usurious rstes.

Comment by bud — October 5, 2025 @ 20:05