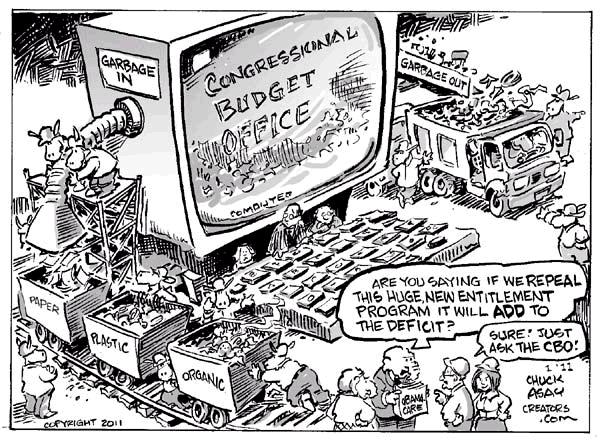

Dan Mitchell explains why there’s a need to change the way the Congressional Budget Office (CBO) and Joint Committee on Taxation (JCT) “keep score” on how proposed legislative changes will impact the US economy:

The CBO, for instance, puts together economic analysis and baseline forecasts of revenue and spending, while also estimating what will happen if there are changes to spending programs. Seems like a straightforward task, but what if the bureaucrats assume that government spending “stimulates” the economy and they fail to measure the harmful impact of diverting resources from the productive sector of the economy to Washington?

The JCT, by contrast, prepares estimates of what will happen to revenue if politicians make various changes in tax policy. Sounds like a simple task, but what if the bureaucrats make the ridiculous assumption that tax policy has no measurable impact on jobs, growth, or competitiveness, which leads to the preposterous conclusion that you maximize revenue with 100 percent tax rates?

Writing for Investor’s Business Daily, former Treasury Department officials Ernie Christian and Gary Robbins explain why the controversy over these topics – sometimes referred to as “static scoring” vs “dynamic scoring” – is so important.

It is Economics 101 that many federal taxes, regulations and spending programs create powerful incentives for people not to work, save, invest or otherwise efficiently perform the functions essential to their own well-being. These government-induced changes in behavior set off a chain reaction of macroeconomic effects that impair GDP growth, kill jobs, lower incomes and restrict upward mobility, especially among lower- and middle-income families. …Such measurements are de rigueur among credible academic and private-sector researchers who seek to determine the true size of the tax and regulatory burden on the economy and the true value of government spending, taking into account the economic damage it often causes.

But not all supposed experts look at these second-order or indirect effects of government policy.

And what’s amazing is that the official scorekeepers in Washington are the ones who refuse to recognize the real-world impact of changes in government policy.

These indirect costs of government, in particular or in total, have not been calculated and disclosed in the Budget of the United States or in analyses by the Congressional Budget Office. The result of this deliberate omission by Washington has been to understate many costs of government, often by more than 100%, and grossly overstate its benefits. …It is on this foundation of disinformation that the highly disrespected, overly expensive and too often destructive federal government in Washington has been built.