Mansa Musa’s good intentions may be the first case in history of failed foreign aid. Known as the “Lord of the Wangara Mines”, Mansa Musa I ruled the Empire of Mali between 1312 and 1337. Trade in gold, salt, copper, and ivory made Mansa Musa the richest man in world history.

As a practicing Muslim, Mansa Musa decided to visit Mecca in 1324. It is estimated that his caravan was composed of 8,000 soldiers and courtiers — others estimate a total of 60,000 — 12,000 slaves with 48,000 pounds of gold and 100 camels with 300 pounds of gold each. For greater spectacle, another 500 servants preceded the caravan, and each carried a gold staff weighing between 6 and 10.5 pounds. When totaling the estimates, he carried from side to side of the African continent approximately 38 tons of the golden metal, the equivalent today of the gold reserves in Malaysia’s central bank — more than countries like Peru, Hungary or Qatar have in their vaults.

On his way, the Mansa of Mali stayed for three months in Cairo. Every day he gave gold bars to the poor, scholars, and local officials. Mansa’s emissaries toured the bazaars paying at a premium with gold. The Arab historian Al-Makrizi (1364-1442) relates that Mansa Musa’s gifts “astonished the eye by their beauty and splendor”. But the joy was short-lived. So much was the flow of golden metal that flooded the streets of Cairo that the value of the local gold dinar fell by 20 percent and it took the city about 12 years to recover from the inflationary pressure that such a devaluation caused.

Orestes R Betancourt Ponce de León, “5 Historic Examples of Foreign Aid Efforts Gone Wrong”, FEE Stories, 2021-06-06.

March 6, 2024

QotD: Mansa Musa’s disastrous foreign aid to Cairo

March 4, 2024

Japan’s Meiji Restoration, 1868-1912

Lawrence W. Reed outlines the end of Japan’s Shogunate Period and the start of the reign of Emperor Mutsuhito, known as the Meiji Period:

The Imperial Household Agency chose Uchida Kuichi, one of the most renowned photographers in Japan at the time, as the only artist permitted to photograph the Meiji Emperor in 1872 and again in 1873. Up to this point, no emperor had ever been photographed. Uchida established his reputation making portraits of samurai loyal to the ruling Tokugawa shogunate.

Wikimedia Commons.

In the 15 years that followed [American Commodore Matthew] Perry’s venture, the grip of the military dictatorship in Tokyo declined. Civil war erupted. When the smoke cleared in the first few days of January 1868, the shogunate was gone and a coup d’etat ushered in a new era of dramatic change. We call it the Reform Period, or the era of the Meiji Restoration.

That seminal event brought 14-year-old Mutsuhito to the throne, known as Emperor Meiji (a term meaning “enlightened rule”). He reigned for the next 44 years. His tenure proved to be perhaps the most consequential of Japan’s 122 emperors to that time. The country transformed itself from feudal isolation to a freer economy: engaged with the world and more tolerant at home.

In 1867, Japan was a closed country with both feet firmly planted in the past. A half-century later, it was a major world power. This remarkable transition begins with the Meiji Restoration. Let’s look at its reforms that remade the nation.

For centuries, Japan’s emperor possessed little power. His was a largely ceremonial post, with real authority resting in the hands of a shogun or, before that, multiple warlords. The immediate effect of the Meiji Restoration was to put the emperor back on the throne as the nation’s supreme governor.

In April 1868, the new regime issued the “Charter Oath,” outlining the ways Japan’s political and economic life would be reformed. It called for representative assemblies, an end to “evil” practices of the past such as class discrimination and restrictions on choice of employment, and an openness to foreign cultures and technologies.

After mopping up the rebellious remnants of the old shogunate, Emperor Meiji settled into his role as supreme spiritual leader of the Japanese, leaving his ministers to govern the country in his name. One of them, Mori Arinori, played a key role in liberalizing Japan. I regard Arinori as “the Tocqueville of Japan” for his extensive travels and keen observations about America.

The Meiji administration inherited the immediate challenge of a raging price inflation brought on by the previous government’s debasement of coinage. The oval-shaped koban, once almost pure gold, was so debauched that merchants preferred to use old counterfeits of it instead of the newer, debased issues. In 1871, the New Currency Act was passed which introduced the yen as the country’s medium of exchange and tied it firmly to gold. Silver served as subsidiary coinage.

A sounder currency brought stability to the monetary system and helped build the foundation for remarkable economic progress. Other important reforms also boosted growth and confidence in a new Japan. Bureaucratic barriers to commerce were streamlined, and an independent judiciary established. Citizens were granted freedom of movement within the country.

The new openness to the world resulted in Japanese studying abroad and foreigners investing in Japan. British capital, for instance, helped the Japanese build important railway lines between Tokyo and Kyoto and from those cities to major ports in the 1870s. The new environment encouraged the Japanese people themselves to save and invest as well.

For centuries, the warrior class (the samurai) were renowned for their skill, discipline, and courage in battle. They could also be brutal and loyal to powerful, local landowners. Numbering nearly two million by the late 1860s, the samurai represented competing power centers to the Meiji government. To ensure that the country wouldn’t disintegrate into chaos or military rule, the emperor took the extraordinary step of abolishing the samurai by edict. Some were incorporated into the new national army, while others found employment in business and various professions. Carrying a samurai sword was officially banned in 1876.

In 1889, the Meiji Constitution took effect. It created a legislature called the Imperial Diet, consisting of a House of Representatives and a House of Peers (similar to Britain’s House of Lords). Political parties emerged, though the ultimate supremacy of the emperor, at least on paper, was not seriously questioned. This nonetheless was Japan’s first experience with popularly elected representatives. The Constitution lasted until 1947, when American occupation led to a new one devised under the supervision of General Douglas MacArthur.

February 27, 2024

Javier Milei gets ghosted by US media after posting rare budget surplus in Argentina

Jon Miltimore on Argentine President Javier Milei’s good economic news that the legacy US media are resolutely ignoring:

Argentine President Javier Milei speaking at the World Economic Forum gabfest in Davos, Switzerland, January 2024.

Photo by Flickr – World Economic Forum | CC BY-NC-SA 2.0

Argentines witnessed something amazing last week: the government’s first budget surplus in nearly a dozen years.

The Economy Ministry announced the figures Friday, and the government was $589 million in the black.

Argentina’s surplus comes on the heels of ambitious cuts in federal spending pushed by newly-elected President Javier Milei that included slashing bureaucracy, eliminating government publicity campaigns, reducing transportation subsidies, pausing all monetary transfers to local governments, and devaluing the peso.

Milei’s policies, which he has himself described as a kind of “shock therapy,” come as Argentina faces a historic economic crisis fueled by decades of government spending, money printing, and Peronism (a blend of national socialism and fascism).

These policies have pushed the inflation rate in Argentina, once one of the most prosperous countries in Latin America, above 200 percent. Today nearly 58 percent of the Argentine population lives in poverty, according to a recent study.

And Milei rightfully blames Argentina’s backward economic policies for its plight — policies that, he points out, are spreading across the world.

“The main leaders of the Western world have abandoned the model of freedom for different versions of what we call collectivism,” Milei said in a recent speech in Davos. “We’re here to tell you that collectivist experiments are never the solution to the problems that afflict the citizens of the world — rather they are the root cause.”

The revelation that Argentina has done something the US government hasn’t done in more than two decades — run a budget surplus — seems like a newsworthy event.

Yet to my surprise, I couldn’t find a word about it in major US media — not in the New York Times, the Associated Press, the Washington Post, or Reuters. (The New York Sun seems to be the only exception.)

I had to find the story in Australian media! (To be fair, the Agence France Presse also reported the story.)

One could argue that these outlets just aren’t very interested in Argentina’s politics and economics, but that’s not exactly true.

The Associated Press has covered Argentinian politics and Milei extensively, including a recent piece that reported how the new president’s policies were inducing “anxiety and resignation” in the populace. The same goes for Reuters and the other newspapers.

A cynic might suspect these media outlets simply don’t wish to report good news out of Argentina, now that Milei is president.

January 26, 2024

Javier Milei to the parasites in Davos – You are the problem

Jon Miltimore on Argentine President Javier Milei’s visit to the World Economic Forum in Davos earlier this month:

Argentine President Javier Milei speaking at the World Economic Forum gabfest in Davos, Switzerland, January 2024.

Photo by Flickr – World Economic Forum | CC BY-NC-SA 2.0

Javier Milei went to Davos to attend the 54th annual World Economic Forum (WEF) meeting last week.

Attendees of the meetings — often derided as global elites who bask in their pomp, privilege, and luxury as they try to address global problems with collectivist solutions — received a jarring message from Argentina’s newly-elected president: you are the problem.

“Today I’m here to tell you that the Western world is in danger,” Milei said in his prepared remarks. “And it is in danger because those who are supposed to have to defend the values of the West are co-opted by a vision of the world that inexorably leads to socialism, and thereby to poverty.”

[…]

This is just a sprinkling of the topics discussed in Davos, of course, but you’ll notice a common current that runs throughout them: the solution to virtually every problem requires more government and “collective action”, and less freedom.

This is precisely the kind of thinking Milei, a self-described libertarian, took aim at in his speech, which was a clarion call for leaders to reject collectivist thinking and embrace individual freedom.

“The main leaders of the Western world have abandoned the model of freedom for different versions of what we call collectivism,” Milei told the audience. “We’re here to tell you that collectivist experiments are never the solution to the problems that afflict the citizens of the world; rather they are the root cause.”

As Milei pointed out, few can better attest to the failures of collectivism than Argentines. The country surged to prosperity in the latter half of the nineteenth century, only to experience a massive drop in prosperity due to its embrace of Peronism, a blend of fascism and socialism named after the left-leaning revolutionary Juan Domingo Perón (1895–1974) who dominated Argentine politics for decades following his initial ascent to power in 1946.

While many of Milei’s predecessors, such as the jet-setting Cristina Fernández de Kirchner, a self-described Peronist and progressive, were delivering international speeches in Copenhagen about tackling climate change through “a new multilateralism”, Argentines watched their country slowly collapse into poverty.

By embracing protectionist trade policies and rampant government spending, Peronists set Argentina’s economy on fire. By 2023, 40 percent of the population was in poverty and inflation had reached more than 140 percent due to massive money printing. Because of the constantly eroding value of pesos, Argentine merchants are compelled to update prices on chalkboards throughout the day.

The human disaster in Argentina was not caused by climate change or AI or “misinformation”.

It was caused by Argentine politicians and bureaucrats abandoning free-market capitalism, an economic system that brought about unprecedented human prosperity across the globe, and a stark contrast to its various collectivist counterparts — fascism, Peronism, communism, anti-capitalism, etc.

This is why Mr. Milei called capitalism the only “morally desirable” economic system, and the only one that can alleviate global poverty.

December 28, 2023

The Liberals may be bad at “deliverology”, but they’re world-beaters at pouring money into black holes

Tristin Hopper explains the apparent paradox that the federal government is spending money faster than it can be printed, yet the things the government is responsible for are perennially underfunded:

From back when The Onion was allowed to be funny – https://youtu.be/JnX-D4kkPOQ

This may surprise the average Canadian given that so much of the government is noticeably threadbare and underfunded. Canadians are dying in hospital waiting rooms due to unprecedented shortages in health care. The navy’s so strapped for cash that it can only deploy one offshore patrol vessel at a time. The RCMP’s federal policing is so under-resourced that Parliamentarians are now calling it a threat to national security. And even $600 billion in cumulative debt hasn’t been enough for the Liberals to honour their 2015 campaign promise to ensure universal clean water on First Nations reserves.

It’s popular to blame all this on some easy-to-identify example of government profligacy, such as Ukraine aid, free hotel rooms for refugee claimants or Prime Minister Justin Trudeau’s noted penchant to rack up outsized travel bills. But Canada’s fiscal problems are well beyond anything like that. At the current rate of spending, the cumulative $2.4 billion in military aid that Canada has sent to Ukraine represents less than a month’s worth of new debt.

So where’s all the money going? Below, a cursory guide to how Canada is able to spend so much while seemingly obtaining so little.

Debt servicing just got way more expensive

First, an easy one: The Trudeau government borrowed an obscene amount during the COVID-19 pandemic, and with rising interest rates the treasury is getting hammered with debt-servicing costs.

As recently as 2021, interest charges on federal debt cost $20.3 billion per year. In the current fiscal year, it’s probably going to blow past $46.5 billion. Ottawa now spends about as much on debt management as it does on health care transfers to the provinces.

The phenomenon of pricier debt is not limited to Canada: Virtually every government in the world ran up record-breaking debts during COVID and are now facing the consequences. But if Canada is different, it’s that our rate of pandemic debt accumulation was at least $200 billion higher than it needed to be. And in justifying all this extra spending at the time, Trudeau argued that it was a good time to take out extra debt since “interest rates are at historic lows”.

The corporate welfare is just unbelievable

Canada has a long history of government signing over grants and bailouts to politically connected corporations. As far back as 1972, then NDP Leader David Lewis famously championed the cause of stopping Canada’s “corporate welfare bums”.

But the Trudeau government has taken corporate welfare to new heights. It was only a few years ago that Bombardier was the undisputed champion in collecting federal grants, bailouts and interest-free loans. Over 50 years, according to an analysis by the Montreal Economic Institute, Bombardier received a cumulative “$4 billion in public funds”.

In just the last calendar year, the Trudeau government has signed two subsidy agreements that would dwarf that $4-billion figure several times over. In the spring, both Stellantis and Volkswagen agreed to build EV plants in Ontario in exchange for federal subsidy packages that could cost as much as $18.8 billion (plus another $9 billion from the Ontario government).

And that new $18.8 billion liability on the books doesn’t even account for the massive ramp-up in the corporate welfare everywhere else. To name just a couple: In 2021, Air Canada got a $5.4 billion loan package. And the Trudeau-founded Strategic Innovation Fund gets about $1.5 billion per year in handouts to green energy companies.

December 2, 2023

Joe Biden solves the inflation problem, fat!

Like any lying dog-faced pony soldier would know, it’s as easy as saying “Trunalimunumaprzure“:

Inflation is kicking just about everyone in the junk here lately, regardless of whether that junk is an innie or an outie. It’s been rough on a lot of us, but I know just how hard it’s been on me and mine.

Prices are up significantly over the last few years and my income isn’t up nearly as much. This creates issues with our finances. The upside is that it’s forced me to be better with money.

But prices are still higher than Willie Nelson on a SpaceX flight.

Luckily, President Joe Biden has figured out the solution to all our problems. He’s going to just tell companies to drop prices.

This week, the White House announced the launch of a Council on Supply Chain Resilience, created with the hope to “strengthen America’s supply chains” and “lower costs for families.”

…

President Joe Biden delivered remarks from the White House on Monday to announce the new council’s creation. He touted the lower inflation rate and falling grocery prices but admonished American companies for, in his view, not going far enough.

“Let me be clear: To any corporation that has not brought their prices back down — even as inflation has come down, even as supply chains have been rebuilt — it’s time to stop the price gouging,” Biden warned, imploring them to “giv[e] the American consumer a break.”

Here’s the issue, at least as I see it.

At Thanksgiving, it was noted here that prices are nearly 20 percent higher than in 2019. This while inflation has supposedly decreased. Prices are still high because it’s not so much that inflation has fallen but that the rate of inflation’s increase has fallen. It doesn’t mean prices should drop, only that they should increase at a slower rate.

November 30, 2023

The challenge facing Javier Milei

Craig Pirrong outlines just how much work Argentinian President-Elect Javier Milei will have to accomplish to begin to bring Argentina’s government in line with his electoral mandate:

When I wrote Milei is not a leftist, let’s say that rather understates the matter. Milei loathes leftists and leftism, and repeatedly refers to them on television and in public appearances in scatalogical terms, calling them “leftards”. He despises collectivism, and asserts bluntly that leftists are out to destroy you. His mission is to destroy them first.

As someone so vehemently hostile to the left and well outside conventional political categories, Milei’s victory has triggered a mass moral panic, especially in the media. The New York Times coverage was (unintentionally) hilarious: “Some voters were turned off by his past outbursts and extreme comments over years of work as a television pundit and personality.” Well, obviously a lot more weren’t, but I guess one has to take solace where one can, eh, NYT?

Milei’s agenda is indeed a radical one, especially for a statist basket case like Argentina. To combat the country’s massive (140 per cent annualised) inflation, Milei says he will dollarise the economy and eliminate (“burn down”) the central bank. He also wants to reduce radically the role of the state in Argentina’s economy. He says he wants to “chainsaw” the government – and emphasises the point by campaigning with an actual chainsaw.

His election on this programme sparked a rally in Argentine financial markets, with government debt rising modestly and stock prices rallying smartly.

Will Milei be able to deliver? Some early commentary has doubted his ability to govern based on the fact that his party’s representation in the legislature is well below a majority. That may be an issue, but not the major obstacle to Milei’s ability to transform Argentina into what it was at the dawn of the 21st century: an advanced, rapidly growing economy and a relatively free society.

The real obstacle is one that is faced by anti-statists everywhere – the bureaucracy. (I do not say “civil service” because that phrase is at best aspirational and more realistically a patent falsehood. Akin to the Holy Roman Empire that was neither holy nor Roman, the “civil service” is neither civil nor a service.)

Argentina’s bloated state is its own clientele with its own interests, mainly self-preservation and an expansion of its powers. Moreover, it has created a whole host of patronage clients in business and labour. Milei’s agenda is anathema to this nexus of public and private interests. They will make war to the knife to subvert it.

Even a president with an electoral mandate faces formidable obstacles to implementing his agenda. The most important obstacle is what economists call an “agency problem”. The bureaucrats are agents of the chief executive, but it can be nigh unto impossible to get these agents to implement the executive’s directives if they don’t want to. Their incentives are not aligned with the executive, and are often antithetical. As a result, they resist and often act at cross purposes with the executive.

The modern chief executive’s power to force his bureaucratic agents to toe the line is severely circumscribed. At best, the executive can make appointments at the upper levels of the bureaucracy (such as the heads of ministries or departments), but the career bureaucrats who can make or break the executive’s policy are beyond his reach, and not subject to any punishment if they subvert the executive’s agenda.

October 21, 2023

Paul Krugman lives in a fantasy world where “The war on inflation is over. We won, at very little cost”

Inflation continues to roar, despite calming words from government officials and legacy media pundits, as anyone who buys groceries could tell you. We long ago gave up going out for dinner, and now we’re very much living week-to-week and hoping the money lasts the whole month. Until my wife’s pension comes in late in the month, we’re utterly skint and trying to avoid spending any money at all. At Ace of Spades H.Q., Buck Throckmorton refutes the pro-government propaganda of, among others, Paul Krugman:

Monty used to use this image at Ace of Spades H.Q., and I certainly think it’s appropriate to include it here.

My household’s monthly grocery bill continues to steadily increase, despite the grocery list containing a pretty consistent basket of goods. We are spending more but not bringing home any more groceries. I am blessed that inflation has not forced us to cut back what we buy, but that hardly seems like an “expectation smashing” spending spree.

This article points out that several categories of retailers are not seeing any revenue growth at all, including clothing stores, electronics and appliance retailers, and sporting goods stores. In other words, these dry goods retailers are seeing declining unit sales as consumers are forced to redirect their decreasing purchasing power toward food, housing, and utilities.

Sales excluding auto and gas increased 0.6%, above estimates for a 0.1% increase compiled by Bloomberg.

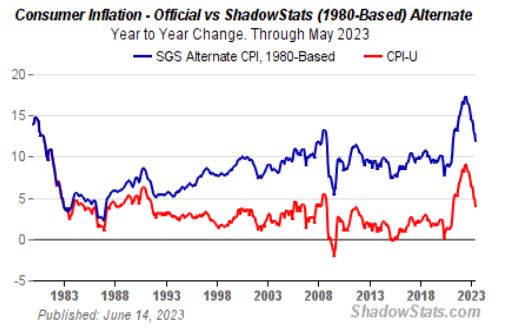

That 0.6% monthly increase in spending annualizes to a 7.2% increase in spending over one year. As we’ve discussed often, the government’s published inflation figures are completely fraudulent, with the Bureau of Labor Statistics reporting that as of September the annual inflation rate is just 3.7%, down from 4.0% in May 2023.

John Williams’ website (shadowstats.com) tracks inflation using the same measurements used in the Carter era. The chart below is updated through May 2023, showing the official 4% inflation as reported by the US government (red line) versus inflation if calculated the same way it was calculated in 1980 (blue line.) Actual inflation is more than 12%, which is 3 times the official bogus government figure.

Therefore, the “expectation smashing” consumer spending that the media is reporting is not even keeping up with actual inflation, which means that consumers are bringing home less in the way of retail goods, despite the increased dollar amount they are spending.

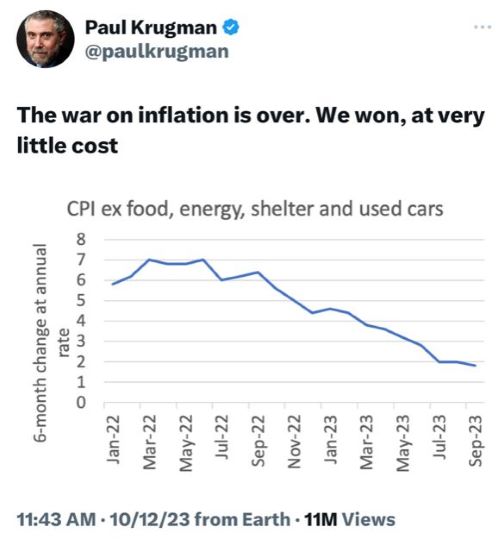

This tweet below is not a parody. Nobel Prize winning

propagandisteconomist Paul Krugman actually stated that excluding food, energy and shelter, “The war on inflation is over. We won, at very little cost.”

Thanks, Mr. Krugman, that’s very helpful. While inflation may be out of control on food, energy, and shelter, those are unnecessary discretionary expenditures. If people will just forego extravagances such as feeding their families and putting a roof over their children’s heads, they’ll do just fine in Biden’s economy.

August 2, 2023

QotD: The Coolidge years

So-called “progressives” tell us that Calvin Coolidge was a bad president because the Great Depression started just months after he left office.

This is precisely the same, lame argument expressed in two different contexts.

In five years (August 2023), we will mark the 100th anniversary of the day that Silent Cal became America’s 30th President. I intend to celebrate it along with others who believe in small government, but you can bet there’ll be plenty of progressives trying to rain on our parade. So let’s get those umbrellas ready.

Let’s remember that the eight years of Woodrow Wilson (1913-1921) were economically disastrous. Taxes soared, the dollar plummeted, and the economy soured. A sharp, corrective recession in 1921 ended quickly because the new Harding-Coolidge administration responded to it by reducing the burden of government. When Harding died suddenly in 1923, Coolidge became President and for the next six years, America enjoyed the unprecedented growth of “the Roaring ’20s.” Historian Burton Folsom elaborates:

One measure of prosperity is the misery index, which combines unemployment and inflation. During Coolidge’s six years as president, his misery index was 4.3 percent — the lowest of any president during the twentieth century. Unemployment, which had stood at 11.7 percent in 1921, was slashed to 3.3 percent from 1923 to 1929. What’s more, [Coolidge’s Treasury Secretary] Andrew Mellon was correct on the effects of the tax-rate cuts — revenue from income taxes steadily increased from $719 million in 1921 to over $1 billion by 1929. Finally, the United States had budget surpluses every year of Coolidge’s presidency, which cut about one-fourth of the national debt.

That’s a record “progressives” can only dream about but never deliver. Yet when they rank U.S. presidents, Coolidge gets the shaft. If you can get your hands on a copy of the out-of-print 1983 book, Coolidge and the Historians by Thomas Silver, buy it! You’ll be delighted at what Coolidge actually said, and simultaneously incensed at the shameless distortions of his words at the hands of progressives like Arthur Schlesinger.

Lawrence W. Reed, “Cal and the Big Cal-Amity”, Foundation for Economic Education, 2018-07-25.

July 17, 2023

The WEF considers whether to use the carrot or the stick next time

Elizabeth Nickson on the World Economic Forum’s latest gathering in China:

Last week the WEFers held their summer camp in China. More to come, they warned us. More pandemics, more catastrophic global warming, more inflation, hell on wheels, they promise us, Armageddon is coming. Be very afraid.

The following was a particularly lovely event:

“How to Stay Within Planetary Boundaries — Carrot or Stick?” which focused on whether to incentivize or force compliance with “climate goals”. It was hosted by some joker who edits a magazine called Nature Energy, no doubt funded by the WEF and read by exactly nobody. And some very po-faced morons of various colors, paid in the six figures, cited a bunch of falsified statistics ending with these pretty little paragraphs:

We are — broadly speaking — agreed that we need to get on track towards a net-zero, climate-safe and nature-positive future, but we know this will not be easy. And we’re going to need to change behaviours of both individuals but also the way that our industries and corporations and also our governments work and practices.

We’re going to need to do this through a mixture of carrots and hopefully perhaps not so many sticks, in some kind of mix. And there is a very active and live debate as to how we go about this. But we’re likely to see an increasing move towards more stick-like interventions …

These guys, they make me laugh. Seriously? How stupid do they think we are? How hated are they? All over the world, they are loathed and laughed at. Every time one of them is taken out, we laugh and laugh and laugh. Larry Fink from BlackRock? Hiding, Scared. Mocked, publicly humiliated. We need a lot more of that.

[…]

They have to destroy western culture, because we middle-class-unnecessary-eaters are too damned uppity. They have stolen so much that when the tipping point arrives, and it will, they will be hung from the highest tree. “Better to ruin those likely to catch and imprison us, and feed on peasants and serfs, the desperate in the rest of the world.”

Proof?

OK, let’s review the Biden/Trudeau/Macron/Sunak economy shall we? Since the out-in-the-open globalist theft of elections during the past three years — Sunak was installed, Trudeau is the most hated man in Canada, Biden is gaga and Macron is just crazy — this is what the bottom 50% are experiencing. Short form, ground into the dirt.

Ninety percent of the jobs “created” were those gained back after the pandemic. Most jobs are going to the foreign born – they work cheap.

Of the roughly 900 days Joe Biden has been in the White House, real wages have fallen for almost 700 days — about 75% of Biden’s time in office. All total, the collective drop in real wages has been 3% rather than the robust real wage gains workers deserve and expect.

Every single American has lost $36,000 to Biden’s inflation. It has crippled us, especially those working in the real (not digital) economy — Uber drivers, truckers, farmers, manufacturers, ranchers, the bottom 50% — gas prices have gone up 50%. Home heating up 23%, milk 16%, beef 25%, eggs 83%. Home prices 32%, rents 15%, electricity 21%.

Let’s not even talk about interest rates. Ten raises in the last 30 months. Last week the Bank of Canada gave its people $26 million in bonuses. Meanwhile, people are losing their houses.

How much more punishment are we expected to take? This is directly caused by their mad hatter spending during the pandemic — which was fake but for a few months in early 2020 — and their subsequent restriction of the energy supply. Restriction of energy causes prices to skyrocket because producing anything requires energy.

June 15, 2023

Thursday tab-clearing

A few items that I didn’t feel required a full post of their own, but might be of interest:

- Justin Trudeau’s government is clearly interested in moving to a Central Bank Digital Currency (CBDC), but “Canadians are not at peace with the idea of cash vanishing into thin air, with a consistent 80 per cent of respondents having no plans to go cashless“

- There’s an ongoing shortage of Adderall in the United States … and the Drug Enforcement Agency (DEA) is behind it.

- Alasdair Beckett-King explains what’s wrong with every time travel movie – https://youtu.be/zI0aBzA2K9s

- The man who visited Lenin’s Soviet Union and said “I have been over into the future, and it works.”

- Kim du Toit isn’t a believer in the official inflation statistics: “When the history of this era comes to be written, one of the most egregious falsehoods to be exposed will be the ‘official’ inflation rate.”

- Random meme of the day:

March 30, 2023

“Food insecurity” – one of the neat new benefits of our over-regulated economy

Elizabeth Nickson on how western governments (in her case, the provincial government of British Columbia) are working hand-in-glove with environmental non-governmental organizations to create “food insecurity”:

Original image from www.marpat.co.uk

In Canada, the British Columbia government in order to increase “food security” is handing out $200,000,000 to farmers in the province. Food insecurity, which means crazy high food prices, comes to us courtesy of the sequestration of the vast amounts of oil and gas in the province and the ever increasing carbon tax, which (like a VAT in Europe), as you probably know, is levied at every single step in food production. Add the hand-over-fist borrowing in which the government has indulged for the last 20 years, and you have created your own mini-disaster.

Ever since multinational environmental non-governmental organizations (ENGOs) took over public opinion in the province, our economy has been wrenched from resource extraction to tourism. Tourism is, supposedly, low-impact. The fact that it pays $15 an hour instead of $50 an hour and contributes very much less to the public purse than forestry, mining, farming, ranching, oil and gas, means we have had borrow to pay for health care and schooling. This madness spiked during Covid, and, as in every “post-industrial” state, has contributed to making food very, very much more expensive, despite the fact that British Columbia where I live, is anything but a food desert. We could feed all of Canada and throw in Washington State.

Inflation comes from a real place, it has a source, it is not mysterious and arcane. Regionally, it comes from “green” government decisions. I pay almost 70 percent more for food now than I did five years ago. Of course one cannot know with any confidence how much the real increase is. The Canadian government was caught last week hiding food price statistics and well they might. The Liberal government leads with its “compassion”, blandishing the weak and foolish, hiding the fact that in this vast freezing country they are trying to make it even colder by starving and freezing the lower 50 percent of the population.

Even the Wasp hegemony that ran this country pre-Pierre Elliot Trudeau knew not to try that. But not this crew! It doesn’t touch them. They don’t see and wouldn’t care if they did, about the single mother working in a truck stop on the Trans-Canada Highway, who steals food for her kids because all her money is going towards keeping them warm.

[…]

The region in which I live used to grow all the fruit for the province, now, well good luck with that buddy. Last year under the U.N. 2050 Plan, local government tried to ban farming and even horticulture. That was defeated so hard that the planner who introduced it was fired and the plan scrubbed from the website. Inevitably it will come again in the hopes that citizens or subjects, as we in Canada properly are, have gone back to sleep. U.N. 2050, an advance on 2030, locks down every living organism, and all the other elements that make up life, assigns those elements to multinationals, advised by ENGOs, which can “best decide” how to use them.

If the only tool you have is a hammer, it’s tempting to treat everything as if it were a nail. It is only the most arcane and numerate think tanks who bang on and on about over-regulation and how destructive it is. Regulation is so complex that most people would rather do anything than think about it, much less deconstruct it.

November 9, 2022

Liberal political fortunes ride “especially women in the suburbs of the Greater Toronto Area” … and those women are angry right now

In The Line, Ashley Csanady has some advice for Justin Trudeau in the lead-up to the next federal election that he really needs to pay attention to:

Poll after poll has told us the Liberals lost white male voters a long time ago, and their electoral fortunes, especially in Quebec and suburban Ontario, rely on women, especially women in the suburbs of the Greater Toronto Area. This isn’t to say dads and other caregivers aren’t angry. Families take many shapes and anyone with small people at home has faced the same indignities over the past nearly three years. However, politically and demographically, it’s the Ontario moms who are going to make or break the next election. And when folks are angry, it doesn’t matter who the incumbent is, they are wont to vote them out.

Nor is it not just about the children’s pain meds.

It’s about the fact we can’t find antibiotic eye drops over-the-counter either (a shortage one pharmacist told me is even worse than the one for pain and fever meds for the wee ones). Another shortage that means we must then turn to an already over-burdened health-care system to get a prescription for a medicine that may or may not be in stock.

Oh, and if that respiratory virus going around turns nasty, we aren’t even certain there will be a hospital bed for our babies when they need it most.

Then there is the infuriatingly slow roll-out of affordable childcare in this province. Parents once again caught between the feds and the province in a battle that may drag out the process so long that many expecting relief will see their kids off to junior kindergarten before it arrives.

Grocery bills are skyrocketing, and while I admit I’m privileged enough to absorb the eye-popping increases, so many families simply cannot. Imagine telling a picky toddler they can’t have their favourite snack because you can’t afford the crackers.

Now, Ontario moms had to deal with yet another disruption to their kids’ schooling, which threw their work lives into chaos once again. More disruptions are possible should bargaining fail again. This just after many women who left the workforce or took a step back from their careers during the pandemic were just getting back into the swing of things.

I made this point — that Ontario moms are angry and much of that anger is directed at political leaders, but I don’t expect it to fall on Ontario Doug Ford — on Twitter a couple weeks back. For this, I was “reminded” — more like chided — that many of these challenges are Mr. Ford’s fault. Or global challenges no logical person could blame the prime minister for. The partisans in my mentions were right on both counts. But here’s what they got wrong:

It doesn’t matter if I’m being “unfair” to Mr. Trudeau, because politics is unfair.

And as for Mr. Ford’s share of the blame, voters punish who’s up next at the ballot box, especially in a crisis. They had a chance to take out their rage on the PCs in June. They didn’t. So who does that leave up next?

October 26, 2022

You apparently only need to worry about inflation if you’re one of the “little people”

Tom Knighton was angered by a recent comment from a well-to-do type who is frustrated at all the “needless” worry about inflation when there are “bigger concerns” in play:

I really don’t like talking about my personal life too much, but I kind of feel like I have to. It started a couple of days when Never Trumper Tom Nichols tweeted this:

Frankly, I’m still pissed about it three days later.

You see, it must be nice for Nichols to view this as a problem of perspective, that people just aren’t seeing the forest for the trees because gas is a tad high.

I can’t be one of those people.

For the record, I think of myself as a working-class writer. I don’t make those six-figure salaries and socialize with the elite at cocktail parties. I make enough to support my family of four in what many could generously term a modest lifestyle.

And I’m OK with that. While I want more, I love the fact that my work life is what it is and I have tons more freedom to do what I want throughout the day.

These days, though, things are different.

You see, while Nichols pretends it’s just people a little grumpy about gas prices, I see the harsh reality that people like him never will.

I’m the guy looking at the time before the next paycheck and realizing that we might not have food in the house for a day or two. I’m the one trying to decide how to stretch the last $40 in our bank account to cover those couple of days and praying it will. I’m also the one who knows that two years ago, this wasn’t a problem.

Hell, a year ago, it wasn’t an issue.

And I don’t make awful money, all things considered. I can only imagine what it’s like for those whose families don’t bring in what I normally make.

For Nichols to get worked up because people don’t see any existential crisis but do see the harsh reality slapping them in the face day in, day out sounds an awful lot like “Let them eat cake” to me.

Unfortunately, that’s what folks like Nichols think.

Nichols, who seems to believe in expertise based on his previous work, is talking about stuff he knows nothing about, things he lacks the expertise to comprehend.

The current inflation isn’t just some mild inconvenience. It’s not one of those things where we all can just shrug and push through until better times. It’s real and it’s here and it’s hurting people like me.

That gives me a certain amount of expertise because this is my life and my livelihood. This is how my family suffers.

I’m very much with him on this, as rising inflation is already a pretty big concern for us and it doesn’t look like it’ll get better any time soon.

September 20, 2022

Pierre Poilievre and the role of the Governor of the Bank of Canada

In The Line, Jen Gerson looks at new Conservative leader Pierre Poilievre’s threat to fire the head of the Bank of Canada if and when he becomes Prime Minister:

Conservative leader Pierre Poilievre at a Manning Centre event, 1 March 2014.

Manning Centre photo via Wikimedia Commons.

In May, Poilievre claimed that Macklem was “surrendering his independence” to the government of the day by using quantitative easing — printing money — to ease the COVID economic crisis. During the party’s English-language debate in Edmonton, Poilievre also said he would fire the governor if he ascended to prime minister.

This, very rightly, ticked off a lot of people. The governor of the Bank of Canada ought to be independent of daily partisan machinations for very good reason; we don’t want the person setting inflation targets to be subject to political pressure, otherwise we would risk a lot more money printing to pay for social programs in the short term, and devaluation of our currency in the long term. So threatening to fire the governor because he or she failed to hew to an incoming government’s wishes is a bad idea. We want that person to stay above the partisan fray.

A Conservative ought to understand this better than most.

Further, much of our inflationary woes is the result of international supply chain issues, which is something beyond the governor’s control. The bank’s defenders have been quick to make this point. Looking at overall increase in the monetary supply, including the significant amounts of money that was pumped into the economy for pandemic relief measures, in addition to the thwack of cash sitting on the banks’ books in the form of potential debt, I suspect that this argument is still highly debatable.

Regardless, the response to Poilievre’s comments from the bank itself was interesting. Although he didn’t call for the firing of his boss, Paul Beaudry, the deputy governor of the Bank conceded that Poilievre had at least a smidgen of a point.

“The aspect that we should be held accountable is exactly right,” Beaudry told a news conference in June. “Right now we completely understand that lots of Canadians can be frustrated at the situation,” he said. “It’s difficult for a lot of people. And we haven’t managed to keep inflation at our target, so it’s appropriate [that] people are asking us questions.”

Macklem himself acknowledged that he had misjudged the possibility for a serious inflationary period back in April. He deserves praise for admitting this! It’s difficult for people in senior roles to admit they were wrong and seek to course correct. One might even argue that his humility on this point demonstrates a personality that is particularly well-suited for his role.

So I want to reiterate that I think threatening to fire Tiff Macklem is a bad idea. It directly undermines the independence of his office, and it places blame on the bank for inflation, when the causes of that inflation are, at best, not his fault, and at worst, still not perfectly understood.

That said — again, messing with the independence of the bank is bad, m’kay — there is a historical precedent for this kind of institution-meddling chicanery. The last politician to threaten an unpopular Bank of Canada governor for political gain was that notable far-right populist … Jean Chrétien. That was back in 1993, in a situation that almost perfectly mirrors the economic and political dynamics of today.

In the ’90s, the incumbent Conservatives had appointed Bank of Canada governor John Crow, who had set interest rates to about seven per cent in order to keep inflation in check. If that figure, which is closer to historical norms than we like to remember, makes you eye your mortgage renewals a little warily, so it should. The Liberals, who were gunning to take over the government from the Conservatives, had argued that Crow’s obsession on maintaining low inflation had worsened a recession; they wanted Crow to prioritize reducing Canada’s unemployment rate instead.

Of course, if that sounds like a potential prime minister taking swipes at an ostensibly independent agent of the Bank of Canada, well, that’s because that’s exactly what it was. And media at the time recognized this at the time.

I think this is another case of a politician indulging in a bit of “bad policy but good politics” rhetoric. Unless he actually means it…