I’m far from alone in taking the Canadian government’s absurd over-reaction to the Freedom Convoy 2022 political protest in February as a reason to be concerned about the Canadian banking system. Until then I’d paid very little attention to alternative currency options like Bitcoin and the like, but I now understand that they may be a key element in future financial planning. At Quillette, Jonathan Kay explains that he realized at the same time he needed to know much more about crypto:

“Bitcoin – from WSJ” by MarkGregory007 is licensed under CC BY-NC-SA 2.0![]()

![]()

![]()

![]()

On February 15th, following weeks of anti-vaccine-mandate protests in downtown Ottawa, Justin Trudeau lurched from complete inaction to absurd overreaction by declaring a national emergency. One effect of this was that banks were suddenly authorized to freeze the personal assets of citizens linked with the protests, civil liberties be damned. Around the same time, moreover, hackers acquired and published identifying information associated with thousands of people who’d donated money to the protest movement. Rather than denounce this apparent criminal data breach, many public figures — including Gerald Butts, who’d been Trudeau’s right-hand man before resigning amid scandal in 2019 — actually celebrated this doxxing. Some media outlets even tried to mine the dox information for clickbait before being stung by a public backlash. While I hadn’t donated to the Freedom Convoy movement, I was sufficiently appalled by these developments that I started educating myself about how one might donate to a similar cause without government officials and social-media hyenas exploiting these transactions as a pretext to attack my assets and reputation.

The easiest way to get into the crypto market, I learned, is simply to open an account at an exchange platform such as Coinbase or Wealthsimple. But while they’re easy to use, exchange platforms also generally require clients to supply government-issued ID when they secure their accounts, and transactions are traceable by authorities. To assure myself of real anonymity and theft-protection, my tutor instructed me, a better (if more complex) option is “cold storage”. This is a real physical device — in my case, something called a Ledger — that acts as a personal crypto wallet.

My Ledger (which looks like a large USB key drive) contains the data required to generate the “private keys” (which look like long passwords, though that isn’t quite what they are) that allow me to send my crypto to other people. And that spending can be done only in those moments when the device is connected to the Internet, after which it can be relegated to a drawer or safe (thus the metaphorical concept of “cold storage”). On the other hand, I can receive money even if the Ledger is offline, so long as the sender has my public key, which (unlike a private key) is generally safe to give to others (such as, say, a prospective donor to any charitable cause that I might establish).

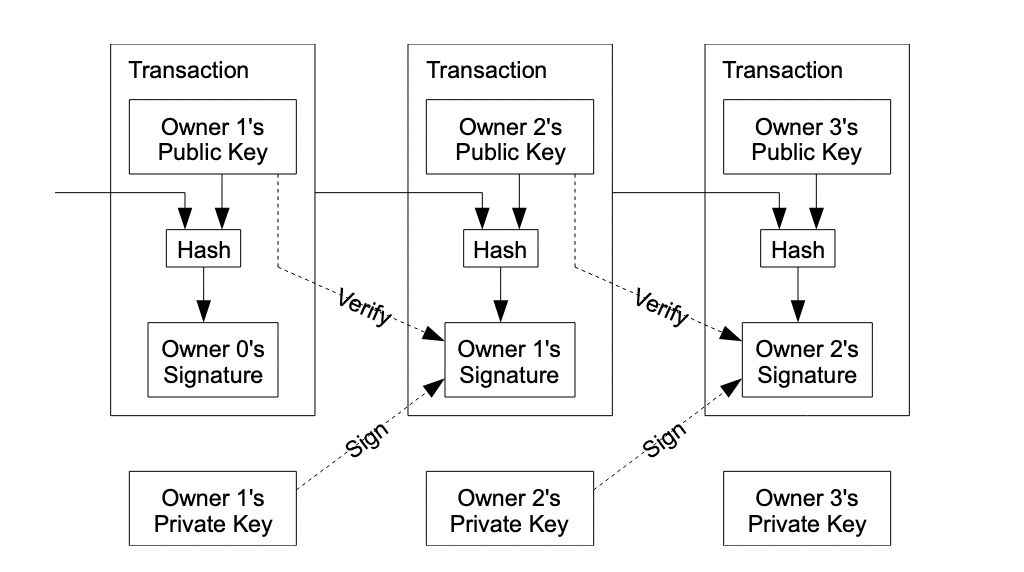

Bitcoin’s basic mechanics were set out in 2009 by the much-mythologized pseudonymous author (or collective) known as “Satoshi Nakamoto”. In a legendary white paper titled Bitcoin: A Peer-to-Peer Electronic Cash System, Satoshi describes the newly conceived electronic coin as consisting of a chain of digital signatures (a blockchain) that build one upon the next through a mathematical mechanism known as a cryptographic hash function — a one-way function whose output doesn’t expose the original private key to reverse-engineering. So once a bitcoin transaction is recorded and added in verified form to the blockchain by everyone — this being the “public distributed ledger” that bitcoin users are part of — the transaction can’t be erased or reversed (with one important theoretical exception, described later on).

Image contained in Bitcoin: A Peer-to-Peer Electronic Cash System, demonstrating the use of public and private keys to verify and sign bitcoin transactions.

Of course, you don’t need to understand how this cryptography works to use cryptocurrency. But it is worth getting your head around an important concept that fundamentally separates crypto from conventional assets such as, say, money that sits in a bank account. Your bank account number doesn’t have any value in and of itself: It’s just an institutional convenience that tells you and your bank where your actual money’s been filed (which is why that account number sits in plain sight on every physical check you sign, assuming you still use checks). But in the case of bitcoin, a private key basically is money — in the sense that anyone with access to such a key can spend the associated funds. And so if you lose your private-key information, or it gets stolen by a thief, there’s no 1-800 helpdesk number. It’s gone forever.