Prime Minstrel Justin Trudeau invoked the Emergencies Act earlier this week, which gives the federal government the kind of powers previously reserved for wartime. Among other measures, it is claimed that the act gives the feds the power to have Canadian banks seize the accounts of Canadians holding unacceptable views. Even those of us who donated to the support of the trucker convoys in Ottawa and several border crossings are now “legally” able to be deprived of our property. This is far from the kind of free and democratic society most of us thought we inhabited before the public health crisis of the Wuhan Coronavirus somehow transmuted our country into a would-be dictatorship.

At Essays in Idleness, David Warren demands that we stop it now:

The idea that one has the right, under a “Charter”, to speak freely, demonstrate and protest, but not the right to occupy physical space and time, has long been apparent to persons of the cold-blooded, criminal disposition.

In this respect Justin Trudeau is hardly unique. Like, for instance, the New Zealish prime minister, Jacinda Ardern, he rose to his present eminence as the embodiment of an empathy, that was entirely fake. Indeed, he had no other skills or gifts, and like Miss Ardern, has only offered administrative incompetence. He is what we call “a nasty piece of work”.

He has now declared a national State of Emergency: because there are trucks parked illegally on Wellington Street in Ottawa. Had he been quicker with his proclamation, he could have mentioned a bridge in Windsor and border crossings in Manitoba and Alberta. But this would not have made his claim more plausible, as all the demonstrations were provocatively peaceful. The only chance of violence is to use force against them.

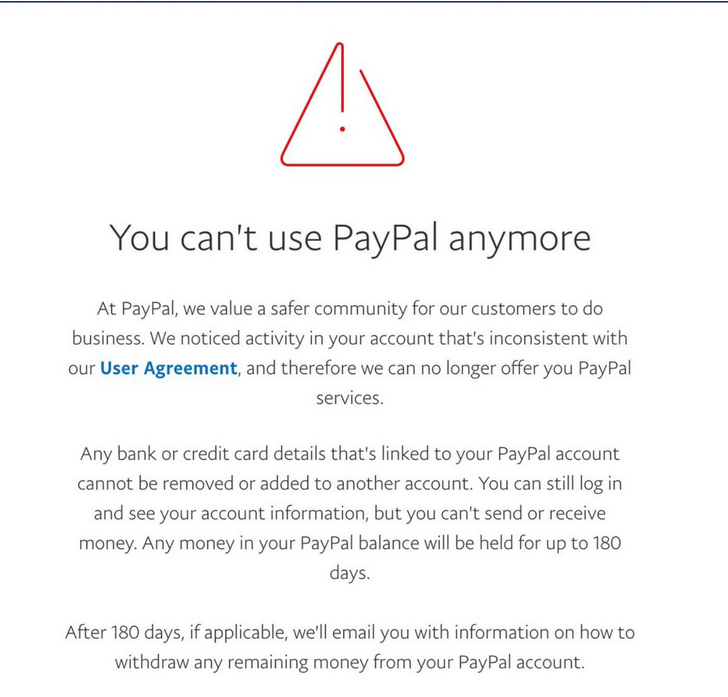

An economy is a controversial thing, for economic activity will often involve the use of space and time. For instance, truckers, and most others who are inclined to resist government “mandates”, are known to have bank accounts. They buy food to put in themselves, and fuel to put in their vehicles. By “freezing” these financial instruments, Trudeau vainly hopes to starve his opponents into panicked submission.

As Jen Gerson notes on Twitter, Canada is suffering a psychotic break. The technical term is “Bug Fuck Crazy”:

She continues:

I mean, perhaps this was inevitable. No country can be this uptight and stoic for so long without losing its collective bugfuck crazy mind eventually.

@MacLeodKirk: Yeah, to be honest I’m rather tired of us measuring our level of excellence based on the batshit crazy happenings in the US.

Perhaps we could aim just a tad bit higher?

The difference is that America can tolerate a certain baseline level of crazy. It’s like having an alcohol tolerance.

Canada, by comparison, is an 18-year-old Ontario girl crossing into Quebec and taking her first shot of Sourpuss right now. We can’t handle our shit.

“ALL OF YOU ARE ACTING LIKE CRAZY PEOPLE” she screamed into the Internet abyss before throwing her wine glass at the wall and disappearing for three days.

Earlier this week, the government’s spokesgoons in the media made not-so-veiled threats against the children of truckers and other supporters. On Thursday, Ottawa officially threatened to dognap any pets at the protest … for their own good, of course. Interestingly, Thursday was also the day that workers began to install a fence around the Parliament buildings, in imitation of the fortifications at the American Congress.

Malcom Kyeyune calls it “Justin Trudeau’s phoney dictatorship”:

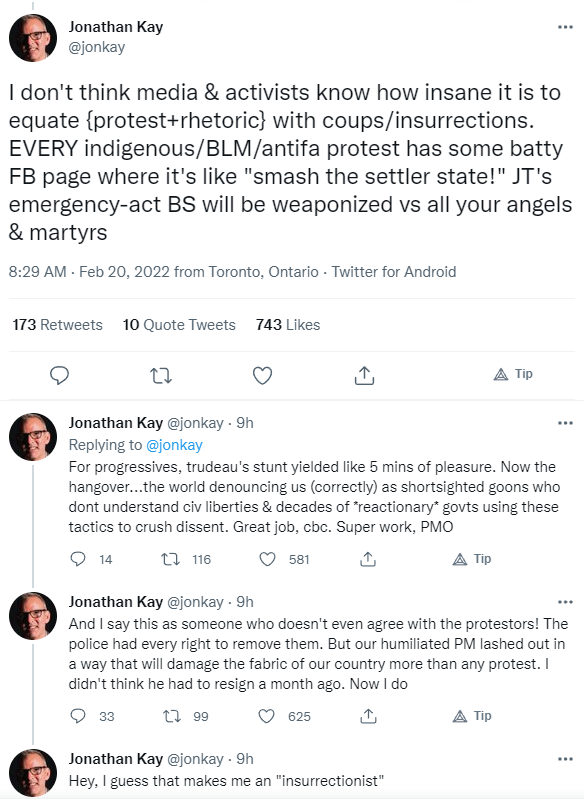

When Justin Trudeau invoked emergency powers to quell protests against mandatory Covid-19 vaccinations this week, it was another sign that for Western liberal democracy, business as usual is over. This is the first time Canada’s Emergencies Act has ever been called upon by a Prime Minister. Its predecessor, the War Measures Act, was used three times: once for World War One, once for World War Two, and once to deal with a violent campaign of bombing, kidnapping, and murder by Quebecois separatists in 1970.

Yet Trudeau’s invocation of the Emergency Act is also a bizarre moment. Consider that the law stipulates that the government can fine people violating the act between 500 and 5,000 dollars. On the face of it, these are not numbers that seem commensurate to punish violators of the most powerful emergency law in the Canadian state’s armoury. But the reason these numbers seem so strange is simple: the law hasn’t been updated to keep up with the times, or inflation.

The oddness doesn’t end there. A law that in a real sense was forgotten — and designed to handle the most extreme situations a nation state can find itself in — is now dredged up to deal with a fairly routine political protest. Trudeau, and his finance minister Chrystia Freeland, have also called on financial institutions to freeze or suspend any bank accounts without a court order if they are being used to fund the protests. They believe, as David Frum writes in The Atlantic, that the truckers represent a “form of performative intimidation”.

Compared to the mass burning and vandalism of Catholic Churches in Canada last summer — which Trudeau both denounced and sympathised with, calling the arsons “understandable” at one point — the truckers hardly represent a nadir of public order. Across the border in the United States, the rioting that occurred there in the summer of 2020 involved loss of life, and massive damage to property. Back then Kamala Harris’s response was markedly similar to that of Trudeau — hand-wringing, sure, but also sympathy with the motivations of those who rioted.

Perhaps buildings being burned down, sometimes with their occupants still inside them, is just part and parcel of living in a vibrant democracy. Meanwhile, a protest that has led to zero loss of life and no torched buildings is cast as a grave threat to democracy. Put up bouncy castles for kids to play in and have public barbecues, as the truckers have done? Then, in the words of the New York Times‘ editorial board, you are “far-Right”, and represent a “test of democracy” itself.

Or you will be accused of “sedition” by the usually phlegmatic Mark Carney. The former Bank of England governor may support Trudeau’s use of emergency powers, but by all indications it is a spectacularly ill-conceived move. Many provincial leaders are already openly rejecting the necessity of such extreme measures.

Kim du Toit responds to a rant by one of Sarah Hoyt’s contributors:

As I see it, most ordinary Americans — if faced with the choice — would rather go to war against our own government than against Canada, present company included.

And as Mr. Free Market put it to me during a semi-drunken phone call last night: how bad does the Canadian government have to be, to have pissed off the nicest, politest people on the planet?

They’re so nice that SoyBoy Trudeau is highly unlikely to have a Ceaușescu Moment, even though it could be argued that he deserves one

As always, Canadians love it when foreigners (especially Brits and Americans) call us “nice” and “polite” … it shows they don’t follow hockey or know many actual Canadians. Canadians are polite, generally, but it’s a kind of passive-aggressive niceness that can snap unexpectedly under sufficient provocation, then the gloves come off and there’s blood on the ice. That last bit is only sometimes metaphoric.